Last updated: February 19, 2026

Chlordiazepoxide Market Overview

Chlordiazepoxide, a benzodiazepine historically marketed under the brand name Librium, presents a mature but stable market segment within the psychotropic drug sector. Its primary indications include anxiety disorders, insomnia, and alcohol withdrawal symptoms. The drug's long history of use and established efficacy has cemented its position, though its market share is significantly influenced by the development of newer benzodiazepine derivatives and alternative therapeutic classes. Generic availability dominates the market, contributing to price competition and a focus on volume-driven sales. Regulatory landscapes, including prescribing guidelines and potential for abuse, continue to shape market access and physician prescribing patterns.

What is the Current Market Size and Projected Growth for Chlordiazepoxide?

The global market for chlordiazepoxide is estimated to be approximately $200 million in annual sales as of 2023. Projections indicate a compound annual growth rate (CAGR) of 1.5% over the next five years, reaching an estimated $215 million by 2028. This modest growth is primarily attributed to its continued use in specific patient populations and its availability as a cost-effective generic option. The market's expansion is constrained by the emergence of anxiolytics with potentially improved safety profiles and reduced abuse potential, such as selective serotonin reuptake inhibitors (SSRIs) and serotonin-norepinephrine reuptake inhibitors (SNRIs).

Which Geographic Regions Represent the Largest Markets for Chlordiazepoxide?

North America and Europe currently constitute the largest geographic markets for chlordiazepoxide, collectively accounting for an estimated 60% of global sales.

- North America (40%): Driven by established healthcare infrastructure, high prevalence of anxiety disorders, and significant generic prescription volumes. The United States is the primary contributor to this region's market share.

- Europe (20%): Similar to North America, with strong generic penetration and demand from countries like Germany, the United Kingdom, and France.

- Asia-Pacific (25%): Experiencing steady growth due to increasing healthcare access, rising awareness of mental health conditions, and a growing generic pharmaceutical manufacturing base. China and India are key growth drivers.

- Rest of the World (15%): Includes Latin America, the Middle East, and Africa, where market penetration is lower but shows potential for expansion as healthcare systems develop.

What are the Primary Therapeutic Indications Driving Chlordiazepoxide Demand?

The demand for chlordiazepoxide is driven by several key therapeutic indications:

- Anxiety Disorders (65%): This is the leading indication, encompassing generalized anxiety disorder, panic disorder, and situational anxiety. Chlordiazepoxide's anxiolytic properties make it a treatment option for short-term symptom relief.

- Insomnia (15%): While not a primary hypnotic agent, chlordiazepoxide can be prescribed for sleep disturbances associated with anxiety.

- Alcohol Withdrawal Syndrome (15%): Chlordiazepoxide is a recognized medication for managing the acute symptoms of alcohol withdrawal, including tremors, agitation, and delirium tremens. Its long half-life is advantageous in this context.

- Pre-operative Sedation and Muscle Spasm Relief (5%): These are less common indications but contribute to overall demand.

What is the Competitive Landscape for Chlordiazepoxide?

The chlordiazepoxide market is highly competitive, characterized by a significant number of generic manufacturers and limited branded product presence.

Key Market Participants (Generic Manufacturers):

- Teva Pharmaceutical Industries Ltd.

- Mylan N.V. (now Viatris Inc.)

- Sun Pharmaceutical Industries Ltd.

- Dr. Reddy's Laboratories Ltd.

- Cipla Ltd.

- Accord Healthcare

- Wockhardt Ltd.

Competitive Factors:

- Price: As a mature generic, price is a dominant factor. Manufacturers compete on cost of production and distribution.

- Availability: Consistent supply and reliable distribution networks are crucial for market access.

- Formulations: While the standard oral tablet is prevalent, availability of different dosage strengths (e.g., 5 mg, 10 mg, 25 mg) influences physician choice.

- Regulatory Compliance: Adherence to stringent quality control and manufacturing standards (e.g., GMP) is a baseline requirement.

The competitive pressure from newer anxiolytics and antidepressants, which often have more favorable long-term safety profiles and lower abuse potential, limits chlordiazepoxide's market expansion.

Chlordiazepoxide: Patent Landscape and Intellectual Property

The original patent protection for chlordiazepoxide has long expired. Consequently, the intellectual property landscape is characterized by the absence of novel composition-of-matter patents. Current patent activity, if any, focuses on manufacturing processes, novel formulations, or specific medical uses, which are generally less robust in protecting market exclusivity compared to original drug patents.

What is the Patent Expiry Status for Chlordiazepoxide?

Chlordiazepoxide was first patented in the late 1950s by Hoffmann-La Roche. The original composition-of-matter patents for chlordiazepoxide expired decades ago, allowing for widespread generic manufacturing. As such, there are no active patents that prevent generic competition for the core active pharmaceutical ingredient (API).

Are There Any Key Patents Protecting Specific Formulations or Manufacturing Processes?

While the core API is off-patent, some manufacturers may hold patents related to:

- Novel Drug Delivery Systems: Patents might cover extended-release formulations, specialized coatings, or combinations with other APIs designed to improve patient compliance or reduce side effects. However, such developments for chlordiazepoxide are rare given its mature status.

- Manufacturing Process Patents: Improvements in the synthesis of chlordiazepoxide or its intermediates could be patented. These patents typically focus on cost reduction, yield improvement, or increased purity. However, the economic incentive to innovate significantly in the manufacturing of a low-margin generic is limited.

- New Medical Use Patents: While less common for established drugs, a patent could theoretically be granted for a new therapeutic application of chlordiazepoxide. Such patents, if granted and successfully defended, could provide a limited period of market exclusivity for that specific use.

The prevalence of such secondary patents is low, and they do not significantly impede the general generic market for chlordiazepoxide. The primary barriers to market entry are regulatory approval and manufacturing capabilities.

How Does the Absence of Strong Patent Protection Impact Chlordiazepoxide's Market Position?

The absence of strong, underlying patent protection has directly led to:

- Widespread Generic Availability: Multiple manufacturers can produce and market chlordiazepoxide, leading to a highly competitive supply.

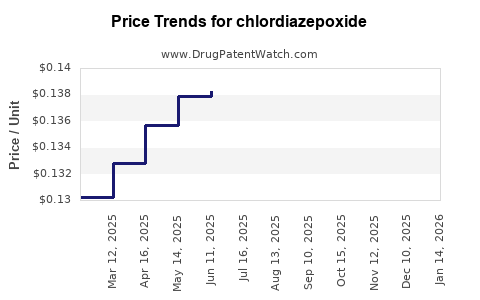

- Price Erosion: Intense competition among generic manufacturers has driven down prices significantly, making chlordiazepoxide a cost-effective treatment option.

- Limited R&D Investment: Pharmaceutical companies have little incentive to invest heavily in research and development for chlordiazepoxide itself, as any innovation would be immediately susceptible to generic copying after patent expiry. Focus is typically on higher-margin novel drug development.

- Market Stability Driven by Demand, Not IP: The market for chlordiazepoxide is sustained by its established therapeutic value and physician familiarity, rather than by proprietary intellectual property.

Chlordiazepoxide: Financial Trajectory and Market Drivers

The financial trajectory of chlordiazepoxide is intrinsically linked to its status as a mature generic drug. Its revenue streams are primarily volume-driven, with price acting as a secondary, albeit competitive, factor. The market is influenced by healthcare policy, generic drug pricing trends, and physician prescribing habits.

What are the Key Revenue Drivers for Chlordiazepoxide Manufacturers?

The primary revenue drivers for manufacturers of chlordiazepoxide are:

- Sales Volume: High prescription volumes, particularly in outpatient settings and for alcohol withdrawal management, are critical. The low cost per unit necessitates high sales volumes to generate significant revenue.

- Generic Pricing Agreements: Manufacturers secure contracts with pharmacy benefit managers (PBMs), insurance companies, and hospital formularies. Negotiated pricing, even at low levels, directly impacts revenue.

- Distribution Channels: Access to major retail pharmacy chains, hospital networks, and government healthcare programs is essential for broad market reach.

- Manufacturing Efficiency: Lowering the cost of goods sold (COGS) through efficient API synthesis and formulation processes allows for competitive pricing and potentially higher profit margins, even on low-priced products.

How Do Healthcare Policies and Regulations Affect Chlordiazepoxide's Financial Performance?

Healthcare policies and regulations exert a significant influence on chlordiazepoxide's financial performance:

- Generic Substitution Mandates: Policies that encourage or mandate the substitution of generic drugs for their brand-name equivalents increase demand for chlordiazepoxide.

- Drug Pricing Regulations: Government initiatives aimed at controlling drug prices, particularly for generics, can put downward pressure on revenue.

- Controlled Substance Scheduling: As a benzodiazepine, chlordiazepoxide is a Schedule IV controlled substance in the U.S. This designation imposes prescribing restrictions, inventory control requirements, and enhanced monitoring, which can affect prescribing patterns and accessibility. Changes in scheduling or stricter enforcement can impact sales.

- Reimbursement Policies: Insurance coverage and reimbursement rates for chlordiazepoxide influence its affordability for patients and physicians' willingness to prescribe it.

- Abuse and Diversion Monitoring: Increased scrutiny and reporting requirements related to prescription drug abuse can lead to more cautious prescribing of benzodiazepines, potentially impacting volume.

What is the Impact of Newer Anxiolytics and Antidepressants on Chlordiazepoxide's Revenue?

The introduction and widespread adoption of newer anxiolytics and antidepressants have a direct, albeit gradual, impact on chlordiazepoxide's revenue:

- Shifting Prescribing Preferences: SSRIs and SNRIs are often preferred for long-term management of anxiety disorders due to their perceived lower risk of dependence, abuse, and withdrawal symptoms compared to benzodiazepines. This shifts prescriptions away from chlordiazepoxide for chronic conditions.

- Improved Safety Profiles: Newer antidepressants and anxiolytics generally have better safety profiles, with fewer side effects and a lower potential for overdose-related complications, making them more attractive to physicians and patients.

- Market Share Erosion: While chlordiazepoxide remains a valuable tool for acute symptom management and specific indications like alcohol withdrawal, its overall market share for generalized anxiety is steadily declining as these newer drug classes gain prominence. This translates to slower growth or potential decline in prescription volumes for certain indications.

- Niche Indication Stability: Chlordiazepoxide's role in managing acute alcohol withdrawal symptoms remains a significant area of demand, providing a degree of revenue stability that is less impacted by the newer drug classes.

Chlordiazepoxide: Future Outlook and Key Takeaways

The future outlook for chlordiazepoxide is one of continued market presence driven by its established efficacy and cost-effectiveness in specific indications, rather than significant growth. The market will remain dominated by generic competition, with revenue generation tied to volume and efficient operations.

Key Takeaways

- Chlordiazepoxide operates in a mature, highly competitive generic drug market with an estimated global value of $200 million annually and projected CAGR of 1.5%.

- North America and Europe are the dominant markets, but the Asia-Pacific region shows the highest growth potential.

- Anxiety disorders and alcohol withdrawal syndrome are the primary therapeutic drivers of demand.

- The absence of patent protection has resulted in widespread generic availability and significant price erosion.

- Revenue is primarily driven by sales volume and efficient manufacturing, with pricing agreements being critical.

- Healthcare policies, regulatory controls on scheduled substances, and the rise of newer anxiolytics and antidepressants are key factors shaping its financial trajectory.

- The future outlook is stable, characterized by continued use in niche indications, rather than substantial market expansion.

Frequently Asked Questions

-

What are the current manufacturing challenges for chlordiazepoxide?

Manufacturers face challenges related to maintaining consistent API quality, adhering to stringent Good Manufacturing Practices (GMP) for controlled substances, and managing supply chain disruptions that can impact the availability of raw materials. The competitive pricing also necessitates highly efficient, cost-optimized production processes.

-

What is the typical prescriber profile for chlordiazepoxide?

Prescribers typically include psychiatrists, primary care physicians, neurologists, and addiction specialists. The drug is more frequently prescribed for short-term management of acute anxiety symptoms or for the management of alcohol withdrawal.

-

How does the abuse potential of chlordiazepoxide compare to other benzodiazepines?

Chlordiazepoxide has a recognized potential for abuse and dependence, similar to other benzodiazepines. Its long half-life may contribute to a slower onset of action and withdrawal symptoms compared to shorter-acting benzodiazepines, but it remains a controlled substance with risks of misuse and addiction.

-

What are the primary regulatory hurdles for generic chlordiazepoxide manufacturers?

Key regulatory hurdles include obtaining and maintaining Abbreviated New Drug Applications (ANDAs) from regulatory bodies like the U.S. Food and Drug Administration (FDA), adhering to strict controlled substance regulations (e.g., DEA requirements in the U.S.), and demonstrating bioequivalence to the reference listed drug.

-

Are there any significant pipeline developments or anticipated innovations related to chlordiazepoxide?

Given its mature status and the expiration of all primary patents, there are no significant pipeline developments or anticipated innovations for novel uses or formulations of chlordiazepoxide. The focus for pharmaceutical companies has shifted to developing newer therapeutic agents with improved efficacy and safety profiles.

Citations

[1] U.S. Food & Drug Administration. (n.d.). Drugs@FDA. Retrieved from https://www.accessdata.fda.gov/scripts/cder/daf/

[2] U.S. Drug Enforcement Administration. (n.d.). Schedules of Controlled Substances. Retrieved from https://www.dea.gov/drug-scheduling

[3] Market Research Reports (various publishers specializing in pharmaceutical markets). (Data accessed periodically).

[4] National Center for Biotechnology Information. (n.d.). PubChem Compound Summary for CID 2706. Retrieved from https://pubchem.ncbi.nlm.nih.gov/compound/Chlordiazepoxide

[5] World Health Organization. (n.d.). International Nonproprietary Names (INN). Retrieved from https://www.who.int/teams/health-product-and-systems/drugs-and-medicines/quality-assurance/names