Aspirin - Generic Drug Details

✉ Email this page to a colleague

What are the generic sources for aspirin and what is the scope of patent protection?

Aspirin

is the generic ingredient in fifty-three branded drugs marketed by Hesp, Plx Pharma, Bayer, Savage Labs, Lgm Pharma, Mpp Pharma, Watson Labs, Allergan, Sandoz, Actavis Elizabeth, Fosun Pharma, Halsey, Hikma Intl Pharms, Ivax Pharms, Puracap Pharm, Quantum Pharmics, Strides Pharma, Lannett, Dr Reddys Labs Sa, Novitium Pharma, Stevens J, Sun Pharm Industries, Chartwell Rx, Bausch, Galt Pharms, Alra, Xanodyne Pharm, Ivax Sub Teva Pharms, Teva, Genus, Novast Labs, Oxford Pharms, Meda Pharms, Ingenus Pharms Nj, Boehringer Ingelheim, Amneal Pharms, Ani Pharms, Barr, Chartwell Molecular, Dr Reddys, Glenmark Speclt, Micro Labs, Ph Health, Sun Pharm, Zydus Pharms, Schwarz Pharma, Abbott, Par Pharm, Medpointe Pharm Hlc, Mcneil, Robins Ah, Genus Lifesciences, Actavis Labs Fl Inc, Epic Pharma Llc, Endo Operations, Roxane, Sanofi Aventis Us, Bristol Myers Squibb, and Aaipharma Llc, and is included in eighty-nine NDAs. There are six patents protecting this compound. Additional information is available in the individual branded drug profile pages.Aspirin has twenty patent family members in nine countries.

There are twenty-two drug master file entries for aspirin. There is one tentative approval for this compound.

Summary for aspirin

| International Patents: | 20 |

| US Patents: | 6 |

| Tradenames: | 53 |

| Applicants: | 59 |

| NDAs: | 89 |

| Drug Master File Entries: | 22 |

| Raw Ingredient (Bulk) Api Vendors: | 136 |

| Clinical Trials: | 1,742 |

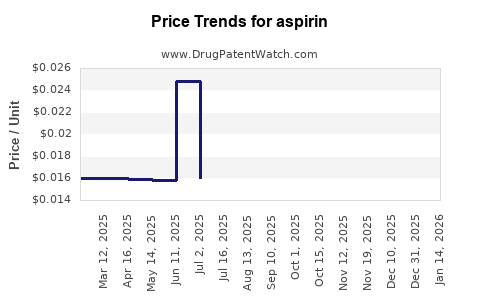

| Drug Prices: | Drug price trends for aspirin |

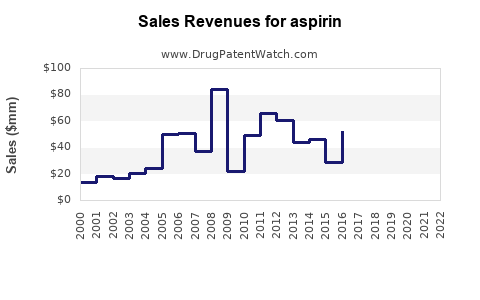

| Drug Sales Revenues: | Drug sales revenues for aspirin |

| Patent Litigation and PTAB cases: | See patent lawsuits and PTAB cases for aspirin |

| What excipients (inactive ingredients) are in aspirin? | aspirin excipients list |

| DailyMed Link: | aspirin at DailyMed |

DrugPatentWatch® Estimated Loss of Exclusivity (LOE) Date for aspirin

Generic Entry Date for aspirin*:

Constraining patent/regulatory exclusivity:

Dosage:

CAPSULE;ORAL |

*The generic entry opportunity date is the latter of the last compound-claiming patent and the last regulatory exclusivity protection. Many factors can influence early or later generic entry. This date is provided as a rough estimate of generic entry potential and should not be used as an independent source.

Recent Clinical Trials for aspirin

Identify potential brand extensions & 505(b)(2) entrants

| Sponsor | Phase |

|---|---|

| Stanford University | PHASE2 |

| Yale University | PHASE3 |

| Medical University of South Carolina | PHASE3 |

Generic filers with tentative approvals for ASPIRIN

| Applicant | Application No. | Strength | Dosage Form |

| ⤷ Start Trial | ⤷ Start Trial | 325MG;40MG | TABLET;ORAL |

| ⤷ Start Trial | ⤷ Start Trial | 81MG;40MG | TABLET;ORAL |

The 'tentative' approval signifies that the product meets all FDA standards for marketing, and, but for the patents / regulatory protections, it would approved.

Medical Subject Heading (MeSH) Categories for aspirin

US Patents and Regulatory Information for aspirin

Expired US Patents for aspirin

| Applicant | Tradename | Generic Name | Dosage | NDA | Approval Date | Patent No. | Patent Expiration |

|---|---|---|---|---|---|---|---|

| Plx Pharma | VAZALORE | aspirin | CAPSULE;ORAL | 203697-001 | Jan 14, 2013 | ⤷ Start Trial | ⤷ Start Trial |

| Plx Pharma | VAZALORE | aspirin | CAPSULE;ORAL | 203697-001 | Jan 14, 2013 | ⤷ Start Trial | ⤷ Start Trial |

| Plx Pharma | VAZALORE | aspirin | CAPSULE;ORAL | 203697-001 | Jan 14, 2013 | ⤷ Start Trial | ⤷ Start Trial |

| >Applicant | >Tradename | >Generic Name | >Dosage | >NDA | >Approval Date | >Patent No. | >Patent Expiration |

International Patents for aspirin

| Country | Patent Number | Title | Estimated Expiration |

|---|---|---|---|

| Australia | 2012315545 | ⤷ Start Trial | |

| Canada | 2850187 | VECTEURS DEPENDANT DU PH POUR LIBERATION CIBLEE DE PRODUITS PHARMACEUTIQUES DANS LE TUBE DIGESTIF, COMPOSITIONS PREPAREES A PARTIR DE CEUX-CI, ET LEUR FABRICATION ET LEUR UTILISATION (PH DEPENDENT CARRIERS FOR TARGETED RELEASE OF PHARMACEUTICALS ALONG THE GASTROINTESTINAL TRACT, COMPOSITIONS THEREFROM, AND MAKING AND USING SAME) | ⤷ Start Trial |

| China | 103957888 | 用于将药物沿胃肠道靶向释放的pH依赖性载体、其组合物及其制备和应用 (Ph dependent carriers for targeted release of pharmaceuticals along the gastrointestinal tract, compositions therefrom, and making and using same) | ⤷ Start Trial |

| European Patent Office | 2760433 | VECTEURS DÉPENDANT DU PH POUR LIBÉRATION CIBLÉE DE PRODUITS PHARMACEUTIQUES DANS LE TUBE DIGESTIF, COMPOSITIONS PRÉPARÉES À PARTIR DE CEUX-CI, ET LEUR FABRICATION ET LEUR UTILISATION (pH DEPENDENT CARRIERS FOR TARGETED RELEASE OF PHARMACEUTICALS ALONG THE GASTROINTESTINAL TRACT, COMPOSITIONS THEREFROM, AND MAKING AND USING SAME) | ⤷ Start Trial |

| Hong Kong | 1200098 | 用於將藥物沿胃腸道靶向釋放的 依賴性載體、其組合物及其製備和應用 (PH DEPENDENT CARRIERS FOR TARGETED RELEASE OF PHARMACEUTICALS ALONG THE GASTROINTESTINAL TRACT, COMPOSITIONS THEREFROM, AND MAKING AND USING SAME PH) | ⤷ Start Trial |

| >Country | >Patent Number | >Title | >Estimated Expiration |

Supplementary Protection Certificates for aspirin

| Patent Number | Supplementary Protection Certificate | SPC Country | SPC Expiration | SPC Description |

|---|---|---|---|---|

| 0984957 | 122012000017 | Germany | ⤷ Start Trial | PRODUCT NAME: ASPIRIN UND ESOMEPRAZOL - MAGNESIUM-TRIHYDRAT; NAT. REGISTRATION NO/DATE: 81047.00.00 20110930 FIRST REGISTRATION: PORTUGAL 5402359 5402367 5402375 20110812 |

| 0984957 | 2012/048 | Ireland | ⤷ Start Trial | PRODUCT NAME: A COMBINATION PRODUCT COMPRISING ASPIRIN AND ESOMEPRAZOLE MAGNESIUM TRIHYDRATE; NAT REGISTRATION NO/DATE: PA 970/063/001 20120831; FIRST REGISTRATION NO/DATE: 5402359; 5402367 5402375 20110812 |

| >Patent Number | >Supplementary Protection Certificate | >SPC Country | >SPC Expiration | >SPC Description |

ASPIRIN: Market Dynamics and Financial Trajectory

More… ↓