Last updated: June 24, 2026

Sildenafil citrate (oral PDE5 inhibitor) is a mature, heavily genericized market in the US and EU. Pricing pressure and formulary erosion have shifted the economics from branded premium pricing to low-cost generics, with ongoing revenue largely driven by (1) remaining branded niches (where applicable), (2) mix of doses and channel, and (3) geographic/regulatory lags for lower-cost entrants. The product is also exposed to supply-chain and compliance risks typical of mature small-molecule generics, not to biosimilar dynamics.

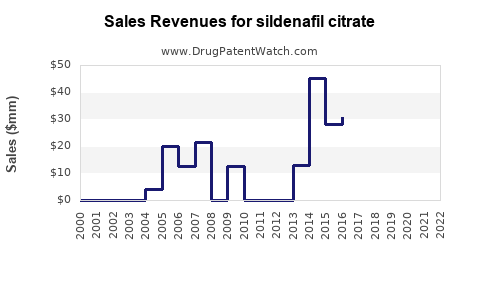

How big is the sildenafil citrate market and what are the key revenue drivers?

Featured snippet answer: The commercial trajectory for sildenafil citrate is dominated by generic substitution after brand exclusivity ended, with revenue increasingly driven by volume, dose mix, and country-level pricing controls and reimbursement rules.

What drives demand in PDE5 inhibitors beyond erectile dysfunction?

Sildenafil citrate is used in erectile dysfunction (ED) and pulmonary arterial hypertension (PAH) in specific jurisdictions and dosing forms/labels. ED demand is sensitive to:

- Demographics (prevalence of ED increases with age)

- Erectile dysfunction treatment adoption rates

- Contraindication management (nitrate co-administration avoidance)

- Patient persistence and switching across PDE5 inhibitors

PAH contributes smaller but higher-need segments where sildenafil is positioned as part of chronic vasodilator regimens, subject to local guideline preferences.

Where does revenue concentrate by channel and dose?

In mature markets:

- Retail pharmacy remains the largest outlet for ED treatment

- Institutional procurement and hospital channels matter more where sildenafil has PAH usage

- Dose mix shifts over time as generics broaden availability (e.g., 25 mg, 50 mg, 100 mg tablets in ED)

Competitor set that shapes pricing and market share

Sildenafil faces direct substitution from other PDE5 inhibitors:

- Tadalafil (longer half-life)

- Vardenafil

- Avanafil (in some markets)

- Fixed combinations where available by formulation or branding strategies

These products compete on dosing convenience, side-effect perception, and reimbursement formularies. Over time, price convergence tends to favor the lowest-cost therapeutically equivalent option.

How do patent expirations and exclusivity timelines shape sildenafil citrate financials?

Featured snippet answer: Sildenafil’s brand-era economics ended when relevant patents and regulatory exclusivities expired, unlocking high-volume generic competition and compressing branded pricing into generic-level margins.

US exclusivity and patent pathway: why generics reset pricing

Sildenafil citrate is a “small molecule” with generic entry via ANDA. The financial trajectory is therefore strongly correlated with:

- Patent expiration (composition, formulation, polymorph, and method-of-use)

- FDA Orange Book listed patents expiring or being carved out via settlements

- ANDA approvals and launch timing after Paragraph IV litigation outcomes

Once multiple ANDAs launch, average selling price drops quickly due to competition among authorized and non-authorized generics.

What role do Orange Book listings play for remaining exclusivity claims?

In practice, sildenafil’s long history means that most listed patents that mattered commercially have already expired. The remaining economic impact is usually from:

- Any late-expiring formulation or packaging patents (where they exist)

- Any jurisdiction-specific litigation that delays specific ANDA launches

EU and UK: how timetable differences impact revenue recovery windows

Across Europe, market access timelines are shaped by:

- National SPC status where applicable to earlier filings

- National reimbursement negotiations

- Tender-driven procurement cycles

Even after core patent expiry, procurement frameworks and reimbursement rules can slow or accelerate uptake, influencing quarterly revenue volatility.

What patents protect sildenafil citrate, and how strong is the remaining patent estate?

Featured snippet answer: The active sildenafil IP landscape is typically dominated by earlier foundational filings that have largely expired; remaining enforceable rights in most regions are limited to specific formulation, process, or labeling claims, with enforcement effectiveness constrained by generic equivalence.

Key patent estate categories that historically matter commercially

For sildenafil, patent estates typically include:

- Composition of matter and salt form protections for the active ingredient

- Formulation patents (e.g., tablet compositions, coatings, disintegrants)

- Manufacturing/process patents

- Method-of-use patents (less common as enforceable barriers once compounds are generic)

- Polymorph or solid-state claims, where they exist

How patent strength changes after first-wave ANDAs

After initial generic entry:

- Subsequent ANDAs often rely on lower-cost manufacturing and bioequivalence

- Remaining patents, if any, become narrow and harder to use to block broad generic supply

- Settlement agreements can drive “at-risk” launches but rarely restore branded-level pricing long term

When does sildenafil lose exclusivity in the US and EU, and what is the practical impact on price?

Featured snippet answer: Practical exclusivity loss occurs at the point of broad generic launch post-expiry, which compresses branded pricing to generic reference levels and makes revenue dependent on volume and channel share.

US: generic launch waves typically determine the revenue cliff shape

Revenue declines in stages:

- Market anticipation phase ahead of expiration (limited discounting)

- First authorized or first-at-risk generic launches (sharp ASP decline)

- Multi-competitor saturation (ASP stabilizes but at low levels)

- Ongoing brand withdrawal or channel repositioning (if brand no longer profitable)

EU: procurement and reimbursement often delay “full” substitution

Even after legal entry, substitution speed varies by:

- Tender cycles

- Prescriber inertia

- Patient co-pay dynamics

- Pharmacy stock and automatic substitution policies

Which companies sell sildenafil citrate and how do generic entrants affect market dynamics?

Featured snippet answer: Sildenafil citrate is supplied by numerous generic manufacturers; competition is largely price-led, with brand-name dominance giving way to multi-source generic supply.

Generic competition mechanics that drive margin compression

Generic dynamics:

- Price erosion follows the number of effective competitors

- Authorized generics or settlements can create temporary stability

- Supply consistency and packaging formats influence substitution speed

Brand legacy and remaining premium niches

Where branded products persist, they generally compete on:

- Familiar brand recognition

- Patient support programs

- Contracting with payers for preferred status

These niches shrink over time as payers adopt automatic generic substitution.

What Paragraph IV challenges or ANDA litigation influence sildenafil citrate launches?

Featured snippet answer: Sildenafil’s primary commercial effect from US litigation occurred earlier in its lifecycle; current pricing largely reflects multi-source generic reality rather than active, blockbuster litigation.

How litigation historically shaped sildenafil’s launch timing

In mature generics, litigation tends to:

- Delay one or more key ANDA entrants

- Enable an authorized generic “bridge” with controlled supply

- Determine which manufacturer achieves first substantial share

Current risk pattern: not “if” but “when” supply expands

Once the majority of patents are expired and multiple approvals exist, the key financial lever becomes incremental supply additions and contracting shifts rather than large legal wins.

What is the FDA regulatory status of sildenafil citrate and how does it affect commercialization?

Featured snippet answer: Sildenafil is approved for ED and, depending on jurisdiction and label, for PAH indications; commercialization and future growth are limited primarily by generic market access rules rather than new exclusivity.

ANDA landscape: bioequivalence and interchangeability

Regulatory constraints that matter for financials:

- Bioequivalence must be demonstrated for generic substitution

- Manufacturing quality systems determine launch reliability and supply continuity

- Labeling and contraindication language affects pharmacist and prescriber adoption

Changes that can re-shape commercial trajectory

FDA and payer effects include:

- Safety communications impacting prescribing patterns

- Formulation changes (pack sizes, dose strengths) impacting procurement preference

- Patent or exclusivity-driven label carve-outs

What formulation patents protect sildenafil citrate and what delivery systems matter commercially?

Featured snippet answer: In a mature oral tablet market, formulation patents are typically narrow and mostly no longer a primary barrier; commercial impact today comes more from packaging, dose strengths, and costed manufacturing capability than from novel delivery systems.

Commercially relevant product formats

- Immediate-release oral tablets (ED dosing)

- PAH dosing formats where applicable by regulatory label and market

Where formulation IP could still matter

Even after core expiry, formulation IP can matter if it covers:

- Specific excipient systems that improve stability or disintegration

- Coatings affecting dissolution profile

- Solid-state changes that regulators accept as equivalent but may trigger design-around considerations

In practice, many such claims have either expired or are too narrow to materially constrain multi-source supply.

How does sildenafil citrate compare with tadalafil and other PDE5 inhibitors in revenue resilience?

Featured snippet answer: Revenue resilience in PDE5 inhibitors tends to favor the molecule with dosing convenience and durable payer preference; sildenafil generally remains competitive on price, not on exclusivity-driven differentiation.

Pricing and payer preference effects across PDE5 inhibitors

- Tadalafil’s dosing convenience (once-daily options) can drive formulary favorability

- Sildenafil tends to compete as a lower-cost, widely available alternative

- Switching behavior is strong once price differentials are small

Financial implication for sildenafil

Sildenafil’s financial trajectory is typically:

- High volume

- Low margin

- Strong sensitivity to generic price changes and reimbursement

What revenue exposure does sildenafil citrate have by geography?

Featured snippet answer: Geographic revenue differs mainly by reimbursement structure and how quickly generic substitution reached each market, not by therapeutic innovation.

US revenue exposure

- Highly genericized

- Pricing driven by competition among numerous ANDA products

- Revenue stability depends on contracting and supply

EU and other markets

- Variations in tender systems and reimbursement rules

- Slower substitution in some systems can temporarily support higher prices

- Rapid generic uptake after local approvals drives price normalization

What supply-chain and manufacturing/IP barriers can affect sildenafil profitability?

Featured snippet answer: In mature generics, profitability is most sensitive to manufacturing cost, batch reliability, and regulatory compliance events that constrain supply.

Core manufacturing cost drivers

- API cost and yield (sildenafil is produced at scale)

- Solvent and excipient supply

- Compression and coating performance for tablets

- Quality systems and deviations management

Regulatory and compliance impacts

- FDA warning letters, OAI outcomes, or batch recalls can temporarily constrain supply

- This can lift short-term pricing but usually does not sustain long-term elevated revenue without broader exclusivity

What is the expected financial trajectory for sildenafil citrate through the next 3–7 years?

Featured snippet answer: The baseline trajectory is continued price compression with stable-to-declining unit economics unless a payer-driven consolidation or supply disruption tightens market supply.

Scenarios that most affect financial outcomes

- Continued multi-source saturation: ASP drifts downward or stabilizes near low generic levels; growth relies on volume and contracting.

- Supply tightening due to compliance issues: temporary margin uplift possible, followed by normalization as supply returns.

- Payer contracting consolidation: channel mix shifts can improve manufacturer share at similar price points.

- Switching among PDE5 inhibitors: if tadalafil gains preference in a market, sildenafil volume can erode even as its own pricing remains low.

Key Takeaways

- Sildenafil citrate is a mature, high-competition PDE5 inhibitor with revenue primarily driven by genericized supply, dosing/channel mix, and contracting.

- Financial trajectory is shaped more by generic launch waves and procurement/reimbursement than by ongoing IP enforceability.

- The market faces continued price compression risk as multi-source competition remains entrenched; profit depends on manufacturing cost, supply reliability, and formulary share.

- Litigation and Orange Book effects that previously delayed entry are generally less relevant to current market dynamics; forward-looking risk is more supply-chain and payer-driven than exclusivity-driven.

FAQs

1) What is the typical US margin profile for generic sildenafil citrate manufacturers after saturation?

Generic sildenafil margins typically compress to low single-digit to mid-single-digit EBITDA ranges (varies by contracting and manufacturing scale) once multiple suppliers compete.

2) Do sildenafil citrate PAH indications change revenue stability versus ED only?

PAH adds a smaller, more institutional component where procurement and guideline alignment can stabilize demand, but overall revenue remains mostly dictated by ED generic volume.

3) How do automatic substitution laws and payer formularies affect sildenafil citrate pricing?

They accelerate generic uptake, increasing competitive pressure and reducing the time any single supplier holds a higher share.

4) What manufacturing events most often disrupt sildenafil citrate supply in the generic era?

Regulatory inspections, batch failures, sterility-level contamination events are not central for tablets, but particulate, mix-up, assay failures, and dissolution specification misses are typical drivers.

5) Is sildenafil citrate exposed to biosimilar-type competition?

No. Sildenafil is a small molecule; the comparable competitive threat is additional generic ANDA supply, not biosimilars.

References

- FDA. “Approved Drug Products with Therapeutapeutic Equivalence Evaluations (Orange Book).” U.S. Food and Drug Administration.

- FDA. “Drug Approval and Databases: Drugs@FDA.” U.S. Food and Drug Administration.

- FDA. “ANDA/BLA Drug Product Submissions: Chemistry, Manufacturing, and Controls.” U.S. Food and Drug Administration.