Last updated: April 22, 2026

Quetiapine fumarate is a major branded and generic CNS product with long-cycle demand driven by schizophrenia and bipolar disorder indications. The market has shifted from branded dominance to sustained generic volume after patent expiries, with continuing revenue contributions from branded strategy adjustments (line extensions and formulations) and risk-managed tendering in major geographies.

What is driving demand for quetiapine fumarate?

Core indications anchor recurring prescriptions

Quetiapine (including the fumarate salt) is prescribed primarily for:

- Schizophrenia

- Bipolar disorder (manic and depressive episodes; maintenance in some regimens)

These therapeutic categories generate steady base demand because treatment is often longitudinal and discontinuation typically requires clinician-led transitions rather than abrupt switching.

Substitution dynamics: same molecule, different formulations

Quetiapine’s market response depends on formulation attributes rather than the API alone:

- Immediate-release (IR) supports flexible dosing schedules and generic availability.

- Extended-release (XR) tends to compete on tolerability and adherence outcomes, and it often carries differentiated pricing dynamics where brand history is strong.

Even when generics enter, formulation-specific competition can sustain price floors longer for the dominant delivery form in a region.

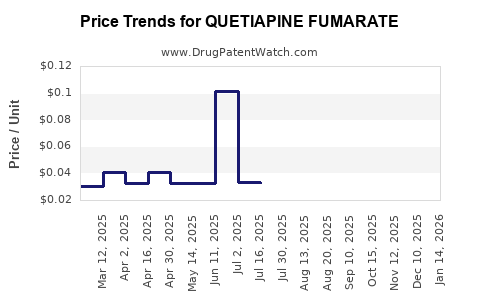

Payer behavior compresses prices post-entry

As generic share rises, reimbursement structures push the product toward:

- Price-linked tendering

- Reference pricing

- Negative formulary placement risk for high-copay segments

This pattern drives a typical post-loss-of-exclusivity trajectory: revenue retention through volume, followed by margin erosion as the number of competitors increases.

How has competition evolved since branded exclusivity?

Shift from brand-led pricing to multi-generic equilibrium

Quetiapine fumarate markets generally follow a predictable exclusivity-to-generic arc:

- Pre-entry: branded pricing power with limited substitution.

- Initial generic entry: steep discounting vs brand; revenue declines begin.

- Multi-generic saturation: lowest-cost providers gain volume; wholesale and retail margins compress.

- Ongoing consolidation: fewer SKUs and fewer profitable tender participants; pricing stabilizes at a lower level than pre-entry.

This lifecycle is reinforced by the drug’s widespread clinical adoption and the ease of therapeutic interchange within the same API class (where local regulations and prescriber practice permit).

Segment differentiation is increasingly formulation-specific

Competition is strongest where payer systems treat IR and XR as separable categories. If a region reimburses XR preferentially or maintains formulary preference, the XR segment can preserve price more than IR, even after generic entry.

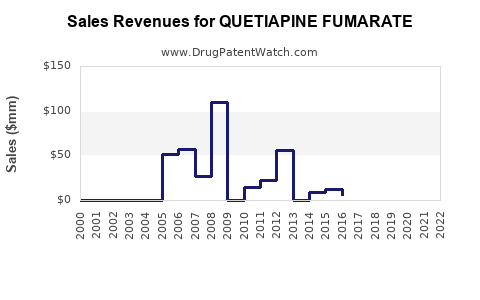

What does the financial trajectory typically look like for quetiapine fumarate?

Revenue trajectory: volume supports, pricing limits

The post-exclusivity financial shape for quetiapine fumarate is usually:

- Revenue decline after generic entry

- Partial stabilization from increased generic volume

- Further margin pressure as competitive pricing intensifies

In practice, the API becomes a “high-volume, low-margin” SKU once multiple generics gain tender traction.

Margin trajectory: wholesalers and pharmacies capture less spread

As discounts widen across generics:

- Wholesale margins compress with tender price competition.

- Pharmacy reimbursement structures tighten dispensing economics.

- Brand protection value shifts to brand loyalty programs, discounting discipline, and XR-related differentiation where formularies allow.

Expense and R&D spend changes with maturity

For the API’s market participants, R&D focus tends to move from the base compound toward:

- Line extensions

- Improved delivery systems

- Lifecycle studies and legal defense

The base fumarate molecule remains mature; financial outcomes rely more on commercial strategy and regulatory execution than on major product innovation.

What regulatory and market-structure factors shape near-term performance?

Patent and litigation risk translates into entry timing

Quetiapine fumarate has experienced multiple rounds of regulatory and legal events over its lifecycle. Market timing effects can be material because even short delays can preserve brand revenue in high-spend geographies.

Tender and reference pricing intensify after entry

In many markets, once generics reach a critical number:

- tender awards become more frequent,

- reference price resets lower,

- and payer procurement cycles accelerate.

This typically causes step-down pricing events rather than smooth declines.

Formulary and switching rules influence generic capture

Where formularies require prior authorization or where switching rules are stricter:

- brand share decays more slowly,

- generic revenue capture is delayed,

- and revenue can stabilize longer at mid-level prices.

Where switching is simpler:

- generic share grows faster,

- and price compression hits earlier.

How do global geography dynamics affect the money path?

High-income markets: earlier genericization, stronger tender discipline

- Generics generally enter earlier.

- Price competition is structured through reference pricing and contracting.

- Revenue becomes more dependent on scale and procurement execution.

Emerging markets: later generic entry, different reimbursement mechanics

- Exclusivity can persist longer by geography or enforcement outcomes.

- Generic uptake can be slower due to procurement fragmentation and variable formulary coverage.

- Price erosion may be less immediate but ultimately becomes severe once procurement consolidates around lowest-cost suppliers.

Outcome: a long tail with periodic step changes

Across both market types, performance is best modeled as:

- long-term base demand,

- periodic step-down events after entry or tender resets,

- and a lower steady-state revenue level after competitive saturation.

What could investors and business leaders infer from the commercial pattern?

The core commercial thesis

Quetiapine fumarate behaves like a mature CNS platform:

- demand is resilient due to clinical necessity,

- but profitability is structurally constrained by generic competition,

- and financial upside is concentrated in execution (tender wins, supply continuity, formulation mix).

The key decision levers

For R&D and investment evaluation, the biggest levers are:

- Formulation strategy (IR vs XR exposure)

- Geographic contracting approach (tender readiness and supply network)

- Lifecycle portfolio (line extensions where formularies support them)

- Cost competitiveness (API supply economics and finished-dose scale)

Key Takeaways

- Quetiapine fumarate demand is anchored by chronic CNS indications, supporting persistent volume even as exclusivity fades.

- Financial trajectory shifts from branded price power to generic volume growth, then to margin compression as multi-generic competition and tendering intensify.

- Near-term outcomes are driven less by clinical novelty and more by formulation mix, payer contracting mechanics, and legal-driven entry timing.

- The market is best treated as a mature, high-volume product with stepwise revenue declines and a long tail of lower-price, high-supply economics.

FAQs

1) Is the market driven more by IR or XR for quetiapine fumarate?

It depends on regional formularies and contracting; XR often carries differentiated reimbursement and switching friction where payers prefer adherence-focused dosing.

2) What typically happens to pricing after generic entry?

Pricing usually declines sharply after initial entry and then falls further as multiple competitors win tender share, stabilizing at a lower steady-state level.

3) Does quetiapine fumarate face demand volatility?

Clinical use reduces volatility; demand is generally steady because therapy changes require clinical oversight and patient-specific transitions.

4) What determines how fast generic share grows?

Tender structures, reference pricing rules, switching policies, and formulary restrictions shape capture speed more than clinical equivalence alone.

5) Where does financial upside come from in mature quetiapine markets?

Upside concentrates in formulation mix, tender execution, and lifecycle commercialization (such as line extensions), not in base-compound innovation.

References

[1] World Health Organization. (n.d.). ATC classification: N05 Psycholeptics. https://www.who.int/tools/atc-ddd-toolkit/atc-classification

[2] U.S. Food and Drug Administration. (n.d.). Drug Approval Reports and related databases. https://www.accessdata.fda.gov/scripts/cder/daf/

[3] European Medicines Agency. (n.d.). Medicine information and EPARs. https://www.ema.europa.eu/en/medicines