Last updated: April 24, 2026

What drives global demand for phenytoin?

Phenytoin is an established, off-patent anti-seizure medicine used for partial seizures, tonic-clonic seizures, and status epilepticus (IV form). Its demand dynamics are dominated by (1) persistence of clinical use, (2) generic availability, and (3) manufacturing and supply continuity for multiple dosage forms.

Primary demand anchors

- Clinical durability: Long-term treatment in epilepsy continues to require steady supply of oral extended-release (ER) and immediate-release (IR) formulations.

- Acute care use: Intravenous phenytoin is used in emergency and inpatient settings for seizure control, which ties demand to hospital utilization patterns.

- Substitution and switching: Because phenytoin is associated with narrow therapeutic considerations, payers and clinicians often enforce brand or formulation continuity, especially when switching between IR and ER or between manufacturers (see product-specific substitution language in prescribing information). This reduces pure “price-only” switching.

Supply and formulation considerations that affect pricing

- Multiple dosage forms: Market availability spans ER capsules/tablets and IV products, each with different manufacturing complexity and regulatory expectations.

- Narrow therapeutic index management: Hospitals and pharmacies may require specific formulation continuity and tighter monitoring, which can slow substitution into the lowest-cost option in some systems.

- Generic competition with meaningful variance: Even with generics, bioequivalence and clinical switching policies can keep effective pricing above the lowest theoretical generic price.

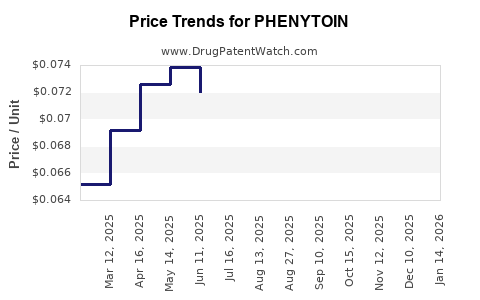

How competitive is the market and what does that do to prices?

Phenytoin is a mature generic market with broad global manufacturing. Pricing is largely driven by competitive tender cycles, local regulatory approvals, and government reimbursement frameworks.

Competitive structure

- Generic-led pricing: With originator exclusivity expired, pricing typically converges toward the cost-efficient generic set.

- Formulation segmentation: ER products often hold pricing above IR-only offerings where payer policies require continuity to avoid breakthrough seizures or toxicity.

- IV continuity: Inpatient supply reliability and procurement contracts can create short-term price and availability swings.

What this means for financial trajectory

- Revenue resilience, margin compression: Demand persists, but unit economics are pressured by generic competition.

- Low product differentiation: The financial profile is less shaped by patent-driven exclusivity and more by supply access, manufacturing yield, and contract wins.

What is the patent and exclusivity context that shapes long-term upside?

Phenytoin’s commercial trajectory is constrained by the fact that it is an established active ingredient with no major patent-protected commercial runway across most jurisdictions. The value proposition is supply and formulation execution rather than lifecycle extension through active-substance patents.

Regulatory and IP reality

- Extended lifecycle is limited: For many older active ingredients, innovation is mostly “line extensions” (new dosage forms, combinations, or manufacturing improvements) rather than new active-substance protection.

- Generic entry caps duration: Once generics enter, pricing typically declines and stabilizes at a low-to-moderate level depending on payer substitution rules and procurement mechanics.

How do product-specific formulations influence market outcomes?

Market dynamics vary by dosage form because switching behavior and hospital contracting differ.

Oral (ER vs IR)

- ER demand stability: ER is favored for consistent dosing and adherence, supporting steady baseline volumes even under generic competition.

- Switching friction: Some formularies limit switching between brands or enforce ER continuity, supporting pricing durability relative to fully interchangeable products.

IV phenytoin

- Hospital procurement sensitivity: IV stockouts can trigger emergency buying at higher cost or drive supply contract changes.

- Clinical governance: IV dosing and monitoring protocols can slow switching to unfamiliar suppliers, which may preserve margins for dependable manufacturers.

Where does financial performance typically come from in phenytoin?

For generic phenytoin manufacturers, financial performance is mainly a function of:

- Market share captured through procurement cycles

- Manufacturing capacity and yield

- Regulatory compliance cost control

- Distribution reach

Cost and operational drivers

- Batch consistency: Phenytoin formulation manufacturing requires stable process control.

- Regulatory maintenance: Ongoing quality and pharmacovigilance obligations affect gross margin and capex planning.

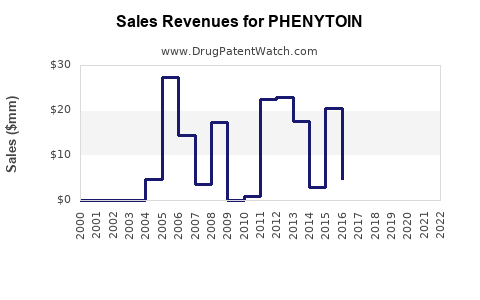

What does the historical market trajectory imply for future financial outcomes?

Because phenytoin is an established therapy, its financial trajectory tends to follow a “late-life generic” pattern:

- Early decline after first generic entrants

- Stabilization at a plateau level under ongoing competition

- Periodic dislocations tied to supply constraints, regulatory actions, or manufacturing disruptions

Expected directionality

- Unit volumes: Generally stable to slowly varying with epilepsy prevalence and treatment persistence.

- Net revenue per unit: Downward trend over time, with occasional recoveries from supply constraints and contract repricing.

- Gross margin: Compresses with generic intensity, but stable if a manufacturer becomes a reliable procurement supplier.

What market signals matter for R&D and investment decisions?

For phenytoin, the actionable signals are less about novel clinical endpoints and more about market access and formulation/regulatory execution.

Signals that move the needle

- Tender outcomes and hospital formularies

- Availability and manufacturing continuity

- Regulatory enforcement actions affecting specific suppliers

- Switching policies tied to ER vs IR formulation continuity

What to track for financial forecasting

- Country-level procurement frequency

- Active ingredient and finished product supply status

- Price indices for generic anti-seizure medicines

- Availability disruptions for IV products

Key Takeaways

- Phenytoin demand is anchored by ongoing epilepsy care and inpatient acute use, with durability coming from clinical persistence rather than exclusivity.

- Competition is generic-led, pushing pricing down while keeping revenue relatively resilient through formulation-specific switching friction.

- Financial outcomes in mature phenytoin markets are driven by procurement wins, supply continuity, and operational execution, not new patent runway.

- The most material near-term drivers are dosage-form availability (especially IV), ER vs IR substitution rules, and tender repricing cycles.

- Future financial trajectory likely follows late-life generic stabilization with periodic price and margin dislocations from supply constraints.

FAQs

1. Is phenytoin still widely used clinically?

Yes. Phenytoin remains a standard anti-seizure medicine for partial and generalized tonic-clonic seizures and is used in acute seizure settings with IV administration (see prescribing information).

2. Why does formulation matter for phenytoin market dynamics?

ER and IV products can face different switching and procurement behaviors than IR, affecting effective interchangeability and supporting pricing durability for specific formulation channels (see product labeling and clinical use patterns).

3. What typically happens to revenue after generic entry for phenytoin?

Revenue per unit typically declines toward generic price levels, while volumes remain supported by clinical persistence and payer or hospital policies that limit fast switching for certain formulations.

4. What are the most important financial drivers for phenytoin manufacturers?

Procurement and distribution access, manufacturing yield and continuity, and compliance costs that determine gross margin under sustained generic pricing pressure.

5. Does phenytoin have meaningful late-stage patent upside?

For most jurisdictions, the active ingredient is long past meaningful exclusivity, so commercial upside is constrained and typically comes from formulation execution, supply reliability, and market access rather than new patent protection.

References (APA)

[1] Pfizer Inc. (2024). Dilantin (phenytoin) prescribing information. https://www.pfizer.com/products/product-detail/dilantin

[2] U.S. Food and Drug Administration. (n.d.). Drug Trials Snapshots: Dilantin. https://www.fda.gov/drugs/drug-trials-snapshots-dilantin

[3] DailyMed. (n.d.). Phenytoin sodium (various products) prescribing information. https://dailymed.nlm.nih.gov/