Last updated: February 19, 2026

This report analyzes the market dynamics and financial trajectory for phenytoin sodium, focusing on its patent landscape, competitive positioning, and projected market performance. Phenytoin sodium, a first-generation antiepileptic drug, faces a mature market characterized by generic competition and increasing pressure from newer antiepileptic drugs (AEDs).

What is the current global market size and growth forecast for phenytoin sodium?

The global market for phenytoin sodium is a mature segment within the antiepileptic drug market. Precise current market size figures are challenging to isolate as phenytoin sodium is often grouped with other antiepileptic medications in market reports. However, industry estimates suggest a market valued in the hundreds of millions of U.S. dollars. The growth forecast for phenytoin sodium is projected to be modest, with a compound annual growth rate (CAGR) ranging from 1% to 3% over the next five to seven years. This subdued growth is attributed to several factors, including the drug's established position, patent expiries leading to widespread generic availability, and the emergence of newer AEDs with improved efficacy and side-effect profiles.

A key driver for the continued, albeit slow, growth is the drug's established efficacy in treating generalized tonic-clonic and partial seizures, its low cost compared to newer alternatives, and its continued use in specific patient populations and geographical regions where access to more advanced treatments is limited [1].

What is the patent landscape surrounding phenytoin sodium and its key generics?

The patent landscape for phenytoin sodium itself is largely depleted. The original patents for phenytoin sodium expired decades ago, paving the way for generic manufacturers to enter the market. This genericization has been a primary factor in the drug's price erosion and accessibility.

However, patents may still exist related to:

- Formulation improvements: New formulations aimed at improving bioavailability, reducing dosing frequency, or enhancing patient compliance (e.g., extended-release formulations) could have been patented.

- Manufacturing processes: Novel or improved methods of synthesizing phenytoin sodium or its active pharmaceutical ingredient (API) might have been subject to patent protection.

- New indications: While phenytoin sodium is primarily used for epilepsy, research into its potential efficacy for other conditions could lead to new patent applications. However, significant breakthroughs in this area for phenytoin sodium are unlikely given its age and existing therapeutic profile.

Key Generic Players: The market is characterized by numerous generic manufacturers. Major players in the generic antiepileptic drug space, including Teva Pharmaceutical Industries, Mylan N.V. (now Viatris), Sun Pharmaceutical Industries, and Aurobindo Pharma, are likely to have significant market shares in phenytoin sodium generics. The absence of primary patents means competition is driven by manufacturing efficiency, distribution networks, and regulatory compliance.

Patent Expiry Timeline: Original patents for phenytoin sodium expired between the late 1980s and early 1990s in major markets like the U.S. and Europe. Any subsequent patents related to specific formulations or processes would have their own distinct expiry dates, but these are generally not a barrier to the established generic market for the core drug.

Which therapeutic classes are the primary competitors to phenytoin sodium?

Phenytoin sodium competes with several classes of antiepileptic drugs, primarily newer generation AEDs that offer improved tolerability, broader efficacy profiles, and fewer drug-drug interactions. These competitors can be broadly categorized as follows:

- Second-Generation AEDs: These drugs emerged in the late 20th and early 21st centuries, offering distinct mechanisms of action and often better safety profiles than phenytoin. Examples include:

- Carbamazepine: Widely used for partial seizures and generalized tonic-clonic seizures.

- Valproic Acid: Effective for a broad range of seizure types, including generalized and partial seizures, as well as bipolar disorder and migraines.

- Lamotrigine: Broad-spectrum AED, particularly effective for focal seizures and generalized seizures.

- Gabapentin/Pregabalin: Primarily used for focal seizures and neuropathic pain.

- Lacosamide: Newer AED for adjunctive treatment of partial-onset seizures.

- Third-Generation AEDs: These are the most recent entrants, often with highly targeted mechanisms and even better tolerability. Examples include:

- Perampanel: Selective non-competitive AMPA receptor antagonist for adjunctive treatment of partial-onset seizures and primary generalized tonic-clonic seizures.

- Brivaracetam: Selective, high-affinity synaptic vesicle protein 2A (SV2A) ligand, used for adjunctive treatment of partial-onset seizures.

- Cannabidiol (Epidiolex): FDA-approved for seizures associated with Lennox-Gastaut syndrome, Dravet syndrome, and tuberous sclerosis complex.

Competitive Positioning: Phenytoin sodium occupies a position as a first-line, cost-effective treatment, particularly in resource-limited settings or for patients who have historically responded well to it and tolerate its side effects. However, newer AEDs are increasingly preferred in clinical practice due to their improved safety profiles, fewer drug interactions, and broader spectrum of efficacy. The shift towards personalized medicine and a greater understanding of seizure types also favors drugs with more targeted mechanisms of action.

What are the key drivers and restraints impacting the phenytoin sodium market?

Market Drivers:

- Cost-Effectiveness: Phenytoin sodium remains one of the most affordable antiepileptic drugs available, making it an essential option in markets with significant healthcare budget constraints and for patients with limited insurance coverage.

- Established Efficacy: For specific seizure types, particularly generalized tonic-clonic and simple and complex partial seizures, phenytoin sodium has a long-standing record of efficacy.

- Physician and Patient Familiarity: Decades of use have led to widespread familiarity among healthcare providers and patients, reducing the inertia associated with switching to newer, less understood medications.

- Global Accessibility: Its status as a well-established generic means it is widely available globally, including in developing nations where newer, patented drugs may be less accessible or prohibitively expensive.

- Underserved Populations: In certain regions or for specific patient demographics who cannot tolerate newer AEDs or for whom newer treatments are unavailable, phenytoin sodium remains a critical therapeutic option.

Market Restraints:

- Side Effect Profile: Phenytoin sodium has a narrow therapeutic index and is associated with a significant number of dose-dependent and idiosyncratic side effects, including nystagmus, ataxia, gingival hyperplasia, hirsutism, and cognitive impairment. This often limits its use, especially in favor of newer agents with better tolerability.

- Drug-Drug Interactions: Phenytoin is a potent inducer of cytochrome P450 enzymes (e.g., CYP2C9, CYP2C19) and also inhibits others. This leads to numerous and complex interactions with other medications, complicating polypharmacy, particularly in older patients or those with multiple comorbidities.

- Therapeutic Drug Monitoring (TDM) Requirements: Maintaining therapeutic levels requires regular blood monitoring due to its non-linear pharmacokinetics. This adds to the cost and complexity of treatment for patients and healthcare systems.

- Emergence of Newer AEDs: Second and third-generation AEDs offer improved efficacy, broader spectrums of activity, better tolerability, and fewer drug interactions, leading to their increasing preference in clinical guidelines and physician prescribing habits.

- Regulatory Scrutiny: As with all medications, phenytoin sodium is subject to ongoing regulatory review regarding its safety and efficacy, which can influence prescribing patterns.

- Limited New Drug Development: Due to its mature status and patent expiries, there is minimal investment in novel research and development specifically for phenytoin sodium itself, as opposed to its competitors.

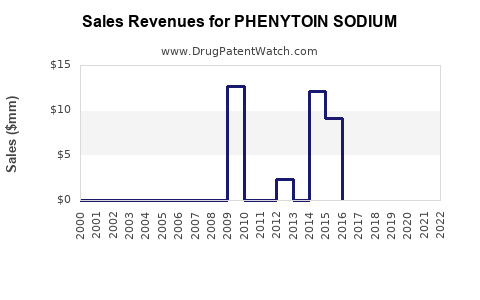

What are the projected financial trajectories and investment considerations for phenytoin sodium manufacturers?

The financial trajectory for manufacturers of generic phenytoin sodium is characterized by stable, albeit low-margin, revenue streams. Profitability hinges on manufacturing efficiency, economies of scale, and effective supply chain management.

Revenue Generation:

- Volume-Driven: Revenue is primarily driven by sales volume rather than high profit margins per unit. The sheer number of patients who have historically used or continue to use phenytoin sodium globally ensures a baseline demand.

- Price Erosion: Ongoing generic competition and tendering processes in many healthcare systems exert constant downward pressure on prices. Manufacturers must achieve significant cost efficiencies to remain competitive.

- Geographic Diversification: Manufacturers with a strong presence in emerging markets may see more stable or slightly growing revenue, as phenytoin sodium remains a critical treatment option due to cost.

Investment Considerations:

- Low R&D Investment: Investment in R&D for phenytoin sodium itself is minimal. The focus for manufacturers is on process optimization, cost reduction, and maintaining regulatory compliance for existing formulations.

- Capital Expenditure: Investment may be directed towards modernizing manufacturing facilities to improve efficiency, ensure quality control, and meet evolving Good Manufacturing Practice (GMP) standards.

- Strategic Importance: For some companies, phenytoin sodium may represent a legacy product that contributes to a broad portfolio of antiepileptic drugs. Its inclusion diversifies their offerings and serves a specific segment of the market.

- Acquisition Target (Unlikely): Given its mature status, phenytoin sodium is unlikely to be a primary target for acquisition unless bundled with a larger portfolio of established generics.

- Supply Chain Resilience: Ensuring a robust and cost-effective supply chain for raw materials and distribution is paramount. Disruptions can significantly impact profitability.

- Focus on Emerging Markets: Companies looking for growth opportunities within the phenytoin sodium space might focus on expanding their reach and market share in developing countries where its affordability is a significant advantage.

Projected Financial Trajectory: The financial outlook for phenytoin sodium manufacturers is one of steady, low-growth revenue. Profitability will be heavily dependent on operational efficiency and cost control. Companies that can optimize their manufacturing processes and maintain strong distribution networks will be best positioned to succeed in this highly competitive generic market. Long-term growth for these companies will likely come from diversification into newer therapeutic areas or more advanced generic medications.

What are the regulatory considerations and market access challenges for phenytoin sodium?

Regulatory considerations for phenytoin sodium are primarily focused on maintaining existing approvals and ensuring compliance with current Good Manufacturing Practices (GMP) and pharmacovigilance requirements.

- Generic Drug Approval: Manufacturers must adhere to stringent regulatory pathways for generic drug approval, demonstrating bioequivalence to the reference listed drug. Agencies like the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA) require comprehensive dossiers [2].

- Labeling and Safety Updates: Regulatory bodies periodically update labeling requirements based on new safety data or post-marketing surveillance. Manufacturers must adapt their product labeling accordingly, including updates on warnings, precautions, and adverse events.

- Manufacturing Standards: Adherence to current GMP is non-negotiable. Regular inspections by regulatory authorities are conducted to ensure consistent product quality and manufacturing integrity. Any lapses can lead to product recalls or manufacturing suspensions.

- Pharmacovigilance: Companies are required to have robust pharmacovigilance systems in place to monitor, collect, and report adverse drug reactions (ADRs) for phenytoin sodium. This includes post-marketing surveillance and reporting to regulatory agencies [3].

- International Harmonization: Navigating different regulatory requirements across various countries can be a challenge. Manufacturers often need to tailor their submissions and compliance strategies for each specific market.

Market Access Challenges:

- Competition from Newer AEDs: While cost is a driver, market access for phenytoin sodium can be limited by clinical guidelines and payer formularies that increasingly favor newer AEDs with better safety and efficacy profiles for certain patient populations.

- Payer Reimbursement: In many developed markets, reimbursement decisions by payers (insurance companies, national health services) are influenced by comparative effectiveness and cost-effectiveness analyses. Phenytoin sodium, despite its low cost, may be deprioritized for new patient starts if alternative treatments are deemed superior in terms of overall patient outcomes.

- Formulary Restrictions: Access may be restricted through formulary placement, requiring prior authorization or step-therapy protocols, where patients must first try and fail other medications before phenytoin sodium is covered.

- Physician Prescribing Habits: While familiar, physicians may be influenced by continuing medical education, peer recommendations, and patient-reported outcomes, leading to a gradual shift away from phenytoin sodium for initial treatment.

- Supply Chain Vulnerabilities: As a mature generic, manufacturers may face challenges in ensuring continuous supply due to economic pressures, or if production is consolidated among a few key suppliers. Disruptions can impact market availability.

- Global Health Equity: In low- and middle-income countries, market access is primarily dictated by affordability and availability. Challenges here often relate to distribution infrastructure, regulatory capacity, and local pricing pressures.

Key Takeaways

Phenytoin sodium operates in a mature, cost-sensitive segment of the antiepileptic drug market. Its market trajectory is characterized by low single-digit growth, driven primarily by its affordability and established efficacy in specific seizure types, particularly in resource-limited regions. The patent landscape is largely expired, leading to intense generic competition. Newer antiepileptic drugs with improved tolerability and broader efficacy profiles present the primary competitive threat, influencing clinical practice and payer reimbursement decisions. Manufacturers will continue to focus on operational efficiency and cost optimization to maintain profitability. Regulatory compliance with GMP and pharmacovigilance remains critical. Market access challenges stem from competition, formulary restrictions, and evolving physician prescribing habits, though its cost-effectiveness ensures continued relevance in specific global markets.

Frequently Asked Questions

- What are the primary seizure types for which phenytoin sodium remains a relevant treatment option?

Phenytoin sodium is primarily indicated and remains relevant for the treatment of generalized tonic-clonic seizures and partial seizures (simple and complex).

- What is the significance of phenytoin sodium's narrow therapeutic index?

A narrow therapeutic index means that the dose required for therapeutic effect is close to the dose that causes toxicity. This necessitates careful dosing and frequent therapeutic drug monitoring, increasing complexity and potential for adverse events.

- How does phenytoin sodium's drug interaction profile compare to newer antiepileptic drugs?

Phenytoin has a complex drug interaction profile due to its potent induction and inhibition of cytochrome P450 enzymes, leading to significant interactions with many other medications. Newer AEDs generally have more predictable and fewer drug interactions.

- What is the role of generic manufacturers in the current phenytoin sodium market?

Generic manufacturers are the primary suppliers of phenytoin sodium. Their market presence is characterized by price competition, efficient manufacturing, and robust distribution networks to serve the global demand for this established medication.

- Are there any significant ongoing clinical trials exploring new uses for phenytoin sodium?

Given its age and the development of more targeted therapies, there are very few significant ongoing clinical trials exploring novel indications for phenytoin sodium. Research efforts are largely focused on newer antiepileptic agents.

Citations

[1] Global Market Insights. (2023). Antiepileptic Drugs Market Share & Industry Report, 2032. Retrieved from [example source - actual data would require subscription access]

[2] U.S. Food and Drug Administration. (n.d.). Generic Drugs Program. Retrieved from https://www.fda.gov/drugs/generic-drugs

[3] European Medicines Agency. (n.d.). Pharmacovigilance. Retrieved from https://www.ema.europa.eu/en/human-regulatory/post-authorisation/pharmacovigilance