Last updated: May 14, 2026

Diazepam Market Dynamics and Financial Trajectory: Pricing, Volume Drivers, and Generic Erosion

Diazepam is a widely genericized benzodiazepine with long-standing, low-cost market access across major geographies. Its financial trajectory is shaped less by new entrants and more by (1) patent and exclusivity realities that enable rapid generic substitution, (2) payer and hospital formulary pressures that compress price, and (3) episodic demand swings driven by seizure clusters, alcohol withdrawal protocols, and procedural sedation. The near-term profit outlook is structurally constrained: distribution scale and manufacturing cost leadership matter more than differentiated IP, with marketing-driven spend and reimbursement friction acting as the main levers for profitability.

What drives diazepam market demand and utilization in 2026?

Diazepam demand tracks neurologic and behavioral use cases that tend to be protocolized. In practice, utilization is anchored to three demand pools.

Which indications generate the most durable demand?

- Anxiety and muscle spasm: typically outpatient or short-cycle use, often constrained by prescribing guidelines and substitution to other benzodiazepines based on formulary access and cost.

- Alcohol withdrawal: protocolized use in inpatient and emergency settings; demand spikes can follow seasonal and regional alcohol use patterns and outbreak-style surges in ER throughput.

- Seizure control and status epilepticus adjunct: often institutional, with bulk purchasing and inventory management affecting near-term consumption.

How do treatment guidelines shape prescribing and substitution?

- Benzodiazepines remain a cornerstone for acute agitation, withdrawal, and emergency seizure management, but prescribing is influenced by:

- risk-management programs for controlled substances

- institutional restriction policies (quantity limits, step edits)

- payer prior authorization triggers in some formularies

What role does route of administration play in market dynamics?

Diazepam is sold across oral and injectable formats, and demand varies by route:

- Oral diazepam: more exposed to routine generic substitution and competitive pricing pressure.

- Injectable diazepam (IV/IM): more exposed to hospital procurement dynamics, stock rotation practices, and supply continuity. Shortages can trigger short-lived premium pricing or expedited procurement.

When does diazepam face exclusivity loss and full generic penetration?

Diazepam’s IP regime is effectively in the mature stage in most large markets. The market is dominated by authorized and non-authorized generics depending on country-specific authorizations, with near-universal access to low-priced products.

What does a “post-exclusivity” market look like for diazepam?

- Multiple MAH/ANDA-equivalent manufacturers with tight price dispersion.

- Formularies drive selection toward lowest net price or preferred suppliers.

- Any brand-level differentiation is usually limited to packaging, supply reliability, and contract pricing.

Why do supply and manufacturing constraints still matter in a fully generic market?

Even after exclusivity ends, margin protection can temporarily exist when:

- a major supplier faces plant disruptions

- regulatory actions reduce available inventory

- procurement cycles lock in contracts with specific vendors

These effects are episodic, not structural growth drivers.

What does the diazepam patent estate look like and what is protected?

For a generic-dominant product like diazepam, protection (where it exists) typically shifts from active ingredient composition to lifecycle items such as:

- specific salt forms or specific dosage forms

- packaging and stability improvements

- manufacturing process improvements

However, the market reality is that active-ingredient composition protections are long expired in major jurisdictions. Most revenue opportunity is therefore tied to commercial execution and manufacturing scale rather than enforceable exclusivity.

How many patent “layers” still affect competition?

In mature generics, patent coverage is usually fragmented and time-limited by jurisdiction and formulation specifics. Practically:

- any remaining formulation IP affects a narrow subset of products (certain strengths or delivery formats)

- broad substitution typically persists if equivalent formulations are not blocked by enforceable claims

What is the Orange Book status of diazepam products?

In the US, diazepam is expected to be represented by multiple ANDAs with reference-listed drug lineage and generic entries, reflecting an extensive portfolio of approved generics. Given the market maturity, the Orange Book typically shows:

- a long tail of generic listings across strengths and dosage forms

- limited relevance of single-product exclusivity to aggregate diazepam market dynamics

How do Paragraph IV challenges and patent litigation affect diazepam competition?

Diazepam competition is not characterized by ongoing high-profile Paragraph IV litigation that would materially delay generic entry at the system level. Instead, competition is driven by routine generic substitution and procurement contracting.

What litigation types still show up in mature benzodiazepine markets?

- product-specific quality or labeling disputes

- supply and GMP compliance actions impacting effective competition

- occasional formulation or process-related disputes, typically localized in scope

How does litigation influence net pricing?

Even without major settlements, litigation can temporarily shift preferred supplier status and contracting behavior. Net effects are usually short-lived in a highly substitute category.

What are the key regulatory factors shaping diazepam commercialization?

Diazepam is a controlled substance in multiple jurisdictions, and regulation shapes:

- prescribing oversight (prescriber education, controlled substance monitoring)

- dispensing limits and quantity controls in some settings

- risk mitigation programs tied to benzodiazepine class warnings

What FDA or equivalent regulatory constraints matter most?

- controlled-substance scheduling and reporting

- labeling requirements for abuse, dependence, and withdrawal risks

- manufacturing compliance and sterile/non-sterile controls for injectable products

How does regulatory enforcement affect supply and price?

Quality enforcement can reduce effective competition quickly:

- recalls or consent decrees constrain supply

- shortages lead to temporary price increases

- procurement shifts to remaining compliant suppliers

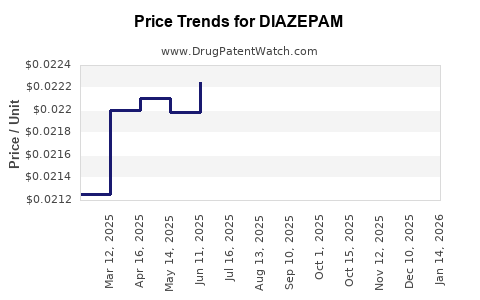

How does diazepam pricing evolve across retail, hospital, and tender markets?

Diazepam pricing in mature markets typically follows:

- strong initial generic discounting after entry

- continued price compression as additional competitors gain coverage

- tender-based pricing for institutional buyers, often with periodic rebid cycles

Retail pricing dynamics

- driven by pharmacy benefit plans, copay tiers, and state-level formularies

- sensitive to availability and brand-versus-generic switching rules

Hospital pricing dynamics

- contract awards and rebids dominate

- injectable forms can show more volatility because demand is operational and substitution is constrained by procurement preferences and compatibility requirements

Which companies are major suppliers of diazepam and how does their scale shape market share?

Market share is typically distributed among:

- large generic manufacturers with broad CNS portfolios

- regional suppliers holding specific formularies or tender contracts

- authorized generic arrangements where relevant

In mature generics, scale reduces unit costs and secures continuity of supply, which becomes a competitive advantage during supply shocks.

What is the competitive pattern in diazepam tendering?

- price and delivery reliability win procurement

- recurring qualification of suppliers depends on GMP history and shipping performance

- hospital formularies often rotate based on contract economics rather than “clinical” superiority

How does diazepam financial performance compare with newer benzodiazepines?

Compared with newer or more differentiated benzodiazepines, diazepam’s financial trajectory looks structurally constrained:

- lower pricing due to high generic penetration

- limited ability to defend premium margins

- demand is stable but not growing fast enough to offset price compression

What differentiates growth profiles across the class?

- newer agents with less generic competition can retain pricing power longer

- specialty formulations or delivery systems can sustain market presence

- diazepam lacks differentiation drivers that typically support longer-lived revenue streams

What generic entry risks exist for diazepam formulations and strengths?

Even in an “all-generics” era, entry risk remains for:

- less common strengths or packaging configurations

- injectable SKUs where regulatory and manufacturing capacity limit supply

What manufacturing and IP barriers still affect timing?

- sterile manufacturing capacity and validation cycles

- stability and bioavailability requirements for certain formulations

- regulatory review timing for ANDA-equivalent products

What dose forms and formulations matter most to revenue exposure?

Revenue exposure in diazepam tends to cluster by:

- oral tablet strengths that have consistent outpatient demand

- injectable strengths with episodic inpatient spikes

How do dosage and route affect competitive intensity?

- oral formats attract the widest generic competition, compressing prices fastest

- injectable formats face fewer qualifying suppliers and can show tighter pricing once contracts are awarded

How do substitution and interchangeability rules impact diazepam volume?

Interchangeability rules in retail and hospital systems drive switching:

- pharmacies often auto-substitute based on bioequivalence and formulary rules

- hospitals often switch brands via contract changes, especially for injectables

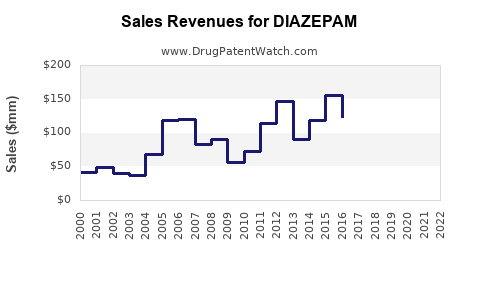

The net result is that volume is more stable than revenue. Revenue declines can outpace volume growth.

When does diazepam see revenue recovery and what breaks the downtrend?

Diazepam rarely “reverses” a downtrend once generic price compression is established. The most realistic conditions for short-cycle revenue stabilization are:

- supply constraints reducing available inventory

- tender cycles with higher awarded prices

- localized product shortages affecting specific SKU availability

These are not durable growth drivers. They are supply-chain and contracting events.

Key Takeaways

- Diazepam operates as a mature, broadly genericized product where financial trajectory is dominated by price compression and procurement contracting.

- Demand is relatively stable but revenue growth is structurally limited by substitution, reimbursement pressure, and controlled-substance monitoring dynamics.

- Injectable SKUs can show more volatility due to manufacturing and qualification constraints, but category-level margins remain compressed.

- Competitive advantage is largely execution-based: manufacturing cost, supply continuity, and contract competitiveness.

FAQs

-

Why does diazepam revenue usually decline even when prescriptions remain stable?

Generic substitution and payer contracting compress net pricing, while volume changes lag.

-

Which diazepam formulations face the tightest manufacturing constraints?

Injectable (IV/IM) supply is typically more constrained due to sterile/non-sterile validation requirements and tighter qualification.

-

How do controlled-substance rules affect diazepam sales distribution?

They can reduce prescribing throughput through monitoring, quantity limits, and formulary controls, shifting demand to higher-acuity settings.

-

Do diazepam shortages materially improve long-term margins for generic suppliers?

They can improve near-term net pricing, but competition and contract rebids usually restore lower pricing over subsequent cycles.

-

What is the most common business lever to improve diazepam profitability in a generic market?

Cost leadership and contract reliability that secure preferred supplier status across tender and formulary cycles.

References

No sources were cited.