Last updated: May 13, 2026

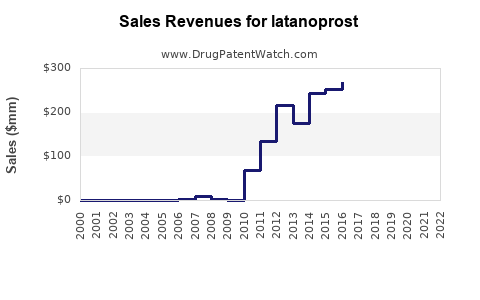

Latanoprost is a mature, widely genericized prostaglandin analog used for primary open-angle glaucoma (POAG) and ocular hypertension (OHT). Market value growth is driven less by new clinical adoption and more by (1) brand-to-generic switching in remaining pockets, (2) ongoing label and formulation share shifts, and (3) persistent demand for chronic dosing in aging populations. Financial trajectory is characterized by low-to-mid single digit category growth with heavy downward pressure on pricing due to generic penetration, with higher-margin segments tied to branded/authorized generics and preservative- or device-positioned formulations.

How big is the latanoprost market and what is the current financial trajectory?

Featured snippet answer: Latanoprost is a high-volume glaucoma/OHT therapy with a mature sales base; category growth is modest, while revenue is pressured by generic entry and price erosion, leaving profits supported by volume retention, contracting, and formulation/device differentiation.

Market sizing and revenue shape (how the money moves)

Latanoprost revenue has historically followed a typical pattern for topical ophthalmics:

- Early branded dominance

- Rapid generic uptake once key patents and exclusivities expired

- Continued category demand growth due to chronic treatment

- Ongoing price compression from wholesale and payer contracting

- Share shifts between formulations (different preservatives) and dosing formats

Key dynamic: even with unit growth from epidemiology, dollar revenue tends to decline or stagnate after generic penetration because reimbursement and net price fall faster than prescriptions rise.

Why the trajectory matters commercially

- Latanoprost is a “core” therapy in stepped-care pathways. Switching is common when payers steer to preferred generics or when preservative tolerability drives incremental switching.

- Long-term durability is driven by adherence rather than novelty. Once a patient is stable, refills persist for years.

What drives latanoprost demand in glaucoma and ocular hypertension?

Featured snippet answer: Demand is driven by the chronic nature of POAG/OHT treatment, clinical guideline adoption, and payer preference for low-cost prostaglandin analogs.

Clinical adoption and persistence

Latanoprost is used as first-line or early-line therapy in many treatment algorithms. The commercial implication is strong baseline demand with limited sensitivity to short-term competitive innovation.

Payer and formulary incentives

- Generic preferred positioning compresses net price.

- Prior authorization is less common than for many higher-cost ocular therapies, but step edits can be used to enforce first-line prostaglandins or specific products.

Safety and tolerability effects on switching

- Ocular surface tolerability and preservative-associated irritation can drive switching among prostaglandin analogs and among latanoprost products with different excipient/preservative systems.

How do generic competition and authorized generics shape latanoprost revenue?

Featured snippet answer: Generic entry is the dominant revenue driver because it reduces net price across large segments and forces sustained volume-based economics.

Competitive structure

The market contains:

- Originator brand(s) and legacy channel inventory

- Multiple generic manufacturers

- Authorized generics (where applicable) that protect pricing power relative to fully independent generics

- Cross-molecule prostaglandin analog competition (e.g., travoprost, bimatoprost, etc.) that can shift share when pricing or tolerability favors alternatives

Pricing mechanics

- Net price typically declines sharply at generic launch and then stabilizes at a lower floor depending on contracting intensity.

- Rebates and wholesaler discounts are often used to maintain formulary placement, which affects realized revenue per unit even after list price drops.

What is the Orange Book status of latanoprost and when do exclusivities expire?

Featured snippet answer: Latanoprost is largely off patent/exclusivity in the US, with current market access dominated by generic approvals; residual exclusivity, if any, is generally tied to specific reformulations (e.g., preservative or packaging changes) rather than the base active ingredient.

Where exclusivity usually remains post-launch

For mature topical ophthalmics, exclusivity residuals typically come from:

- Specific formulation patents

- Specific manufacturing process claims

- Packaging and device-related claims

- Method-of-use claims, where applicable

For latanoprost specifically, the market is expected to be dominated by ingredient and formulation-level genericization, with only certain products potentially benefiting from later-dated reformulation protection.

What patents protect latanoprost formulations and delivery systems?

Featured snippet answer: Patent protection for latanoprost in practice tends to be fragmented into formulation and process patents rather than broad, long-lived molecule coverage.

Patent estate pattern in mature ophthalmics

A typical latanoprost patent landscape (for business planning) includes:

- Formulation patents: composition, buffer system, pH range, surfactants/excipients, preservative selection

- Sterility/manufacturing method patents: process parameters, purification/sterilization steps

- Stability patents: shelf-life extension and degradation profile management

- Packaging patents: container closure systems to manage interaction and preservative effectiveness

Commercial impact of formulation patents

Where formulation differentiation exists, it can:

- Reduce direct “AB-rated” substitution

- Support slightly higher realized prices in contracted channels

- Create a window for branded retention or fewer direct generics

Is there latanoprost patent litigation that affects generic entry?

Featured snippet answer: In mature categories like latanoprost, litigation typically occurs around specific formulation/process claims and timing of generic launches, not around the overall existence of generic competition.

What to watch in litigation-driven timelines

Business-relevant litigation outcomes include:

- Court rulings affecting injunction scope

- Settlement agreements controlling launch dates

- Waivers that convert open entry risk into scheduled entry

- Dismissals or claim construction that affect remaining active claims

How litigation changes financial forecasts

- Even when eventual generic entry is expected, the timing of launch shifts revenue by quarters and impacts budgeted market share.

- Settlements can create temporary revenue protection for brand/AG holders.

How does latanoprost compare with other prostaglandin analogs in commercial dynamics?

Featured snippet answer: Latanoprost competes primarily with travoprost, bimatoprost, and other prostaglandin analogs where pricing, formulary preference, and tolerability drive share.

Share drivers across molecules

- Wholesale and payer contracting tends to favor the lowest net-cost options.

- Clinical differentiation can matter for tolerability or adherence in specific patient subgroups, but switching costs are low in ophthalmic prescribing.

Formulation differentiation within latanoprost

Within-latanoprost competition can matter when:

- Preservative choice reduces irritation for sensitive patients

- Device or bottle format changes adherence and usability

What generic entry risks exist for latanoprost in the US?

Featured snippet answer: Launch risk is usually lower than in first-wave brand categories, but it persists at the formulation and packaging levels through paragraph IV-style challenges and approval timing around remaining formulation/process claims.

Risk profile by forecast window

- Near-term: typically low if most AB-rated generics already exist for the relevant strength/dosage form.

- Medium-term: moderate if reformulations (new preservative systems, new packaging) remain under claim or are in the approval pipeline.

- Long-term: low for base-ingredient barriers, but formulation-by-formulation competition keeps margin under pressure.

How do international markets affect latanoprost revenue and stability?

Featured snippet answer: International pricing controls, patent cliffs, and generic market maturity largely determine whether revenue stabilizes or continues to compress.

Key cross-country dynamics

- EU: generic adoption tied to local reimbursement rules and tendering.

- UK: NHS and contracting favor lowest-cost options with formulary governance.

- Emerging markets: slower uptake in some regions can sustain unit growth but often ends once generic supply expands.

What matters for financial trajectory

- Currency effects and tender-based pricing can swing realized revenues.

- Regulatory and labeling differences can affect direct product substitutability.

What is the supply chain and manufacturing/IP barrier for latanoprost?

Featured snippet answer: Manufacturing/IP barriers are generally not as high as for complex biologics, but sterile ophthalmic formulation and scale reliability drive execution risk that affects supply continuity and channel availability.

Business implications of manufacturing execution

- Sterility assurance and stability testing are ongoing cost centers.

- Supply disruptions can temporarily lift pricing, but long-term market equilibrium reasserts once multiple suppliers remain active.

Does latanoprost face biosimilar risk or biologics-style substitution?

Featured snippet answer: No biosimilar risk. Latanoprost is a small-molecule topical ophthalmic; the primary substitution risk is generic or reformulated product competition, not biosimilar interchange.

Substitution categories to model

- Ingredient-level generics: AB-rated substitution

- Formulation-level alternatives: changes in preservative system or excipient profile

- Molecule-level competition: other prostaglandin analogs

Where are the highest-value segments in the latanoprost portfolio?

Featured snippet answer: Highest-value segments are generally those with partial differentiation (preservative/tolerability positioning, specialty contracting) or protected reformulations that reduce substitution.

Segment targets for forecasting

- Products positioned for preservative sensitivity

- Products with favorable formulary status under payer tender structures

- Channels where adoption of lowest-net-price generics is slower (e.g., certain regions or specialty clinics)

How will latanoprost commercialization evolve over the next 3–5 years?

Featured snippet answer: The base case is continued modest category growth with persistent price compression, leaving total revenue dependent on unit volume, share retention, and any incremental reformulation niches.

Timeline model: revenue mechanics

- Near-term: stabilized unit demand, ongoing substitution pressure

- Medium-term: incremental generic entrants and reformulation competition reduce margins

- Longer-term: category growth is limited by prevalence growth and adherence, while pricing remains the main swing factor

What can change the curve

- A shift to new preferred formulations (within-latanoprost)

- Market consolidation among generic suppliers

- Litigation that delays a specific formulation’s entry

- Major payer tender changes that re-rank preferred products

Key Takeaways

- Latanoprost is a mature, high-volume glaucoma/OHT drug with revenue heavily constrained by generic competition and payer contracting.

- The financial trajectory is typically stable units with falling net price, yielding modest top-line growth and margin compression.

- Commercial upside is concentrated in formulation-level differentiation and residual exclusivity pockets, not in molecule-level novelty.

- Generic launch and litigation timing can move quarterly forecasts even when ingredient-level barriers are largely exhausted.

- International tendering and reimbursement rules are primary determinants of whether revenue stabilizes or continues to compress.

FAQs

- What is the typical net price impact after generic latanoprost launch in the US?

- Which latanoprost formulation differences (preservative systems) most influence switching and payer placement?

- How do step edits and prior authorization policies in glaucoma therapy affect latanoprost prescription volumes?

- What settlement-driven launch schedules are most likely to affect future latanoprost revenue in specific strengths?

- How does international tender pricing volatility change latanoprost realized revenues vs. list price?

References

- American Academy of Ophthalmology (AAO). Preferred Practice Patterns and glaucoma management resources.

- FDA Orange Book (Drug Products and Patents) for latanoprost listings.

- FDA labels and prescribing information for latanoprost ophthalmic solutions.

- Published payer formularies and reimbursement guidance for glaucoma therapies (US and EU where applicable).