Last updated: May 31, 2026

Ascorbic acid is an off-patent, commodity-scale active ingredient with pricing and volume driven by industrial supply, excipient/formulation demand, and vitamin premix/feedstock cycles rather than brand-specific exclusivity. The financial trajectory across most marketed forms is characterized by low gross margins versus branded prescription drugs, frequent pass-through of raw-material moves, and limited payer leverage because use is primarily OTC and food/supplement adjacent.

Is ascorbic acid a brand, generic, or commodity drug?

Featured answer: Ascorbic acid is primarily an active pharmaceutical ingredient (API) in OTC products and a commodity ingredient used across food, supplements, and manufacturing. Most commercial products are generic or contract-manufactured; IP protection is usually limited to specific formulations/processes, not the core vitamin.

Regulatory scope: OTC and supplement adjacency

- In the US, ascorbic acid is widely marketed as a vitamin ingredient. Many products fall under dietary supplement frameworks or OTC vitamin/indication labeling.

- Where marketed as an OTC vitamin, market access is not governed by prescription-only reimbursement dynamics typical for specialty pharma.

Commercial implication

- Revenue is typically volume-based and highly sensitive to wholesale commodity pricing.

- Marketing spend and distribution matter less than supply reliability, grade qualification (pharma vs food), and regulatory compliance.

What market dynamics drive ascorbic acid demand and pricing?

Featured answer: Demand tracks dietary supplement and fortification consumption cycles, while pricing follows industrial-grade supply, China export flows, and conversion costs for feedstocks.

Key demand levers

-

Dietary supplement penetration

- Ascorbic acid supports multivitamins and immune/antioxidant positioning.

- Seasonal patterns show strength during cold/flu periods, but long-run demand tracks consumer category growth more than short-term spikes.

-

Food fortification and processing

- Ascorbic acid is widely used in food applications (oxidation control, stability).

- Industrial demand can smooth OTC variability but does not create brand differentiation.

-

Pharma excipient and injectable/clinical use

- Medical uses exist (including injectable formulations for deficiency treatment or supportive care contexts), but these are typically smaller than supplement/food volume.

Key supply and pricing levers

- Commodity sourcing and capacity

- Industrial-scale production dominates global supply; spot pricing can move quickly with capacity utilization.

- Geopolitics and trade constraints

- Ascorbic acid supply chains are exposed to trade friction and shipment lead times.

- Input cost pass-through

- Conversion costs and energy prices influence supplier pricing even when retail demand is stable.

Competitive intensity

- High number of suppliers and contract manufacturers lowers ability to sustain premium pricing.

- Differentiation usually comes from:

- pharmaceutical-grade certifications,

- particle spec/control for certain formulations,

- packaging formats and compliance documentation for regulated markets.

How does ascorbic acid compare with other vitamin APIs (pricing volatility and growth)?

Featured answer: Ascorbic acid behaves like a low-to-mid volatility vitamin commodity, but its volatility can increase during global supply shocks given the scale economics of production.

Relative demand characteristics

- Compared with niche APIs, ascorbic acid is:

- less sensitive to clinical trial pipelines,

- less influenced by payer formulary constraints,

- more influenced by consumer category growth, nutrition trends, and industrial food fortification rates.

Relative margin profile

- Branded margins are generally not sustainable due to easy substitution.

- Contract manufacturing and repackaging dominate, compressing gross margins.

What patents protect ascorbic acid products, and how weak or strong is the estate?

Featured answer: Core ascorbic acid is off-patent. Patent estates, when present, typically protect specific finished formulations (dose forms, stability-enhancing compositions) or manufacturing methods, not the vitamin molecule itself.

Typical IP coverage patterns for commodity vitamin actives

- Finished product formulation patents

- combinations, sustained release matrices, taste-masking, stability systems.

- Manufacturing process claims

- purification steps, crystallization control, particle-size control.

- Method-of-use

- generally limited because vitamin use is widely recognized and can be hard to patent depending on claim novelty.

Commercial impact

- Even where patents exist, enforcement is harder when:

- generics can redesign around formulation features,

- alternative actives or dosage forms can substitute,

- OTC/supplement channels allow rapid category substitution.

When does ascorbic acid lose exclusivity?

Featured answer: Exclusivity is not meaningfully driven by molecule patent expiration because ascorbic acid is largely off-patent; product-level exclusivity is the exception, not the rule.

What “exclusivity” typically looks like in this market

- Regulatory exclusivity is usually not a primary driver for ascorbic acid sales.

- If a product has protected formulation IP, exclusivity ends with patent expiration or settlement-defined carve-outs, but the market tends to absorb replacements quickly due to generic commoditization.

What is the Orange Book status of ascorbic acid?

Featured answer: Ascorbic acid is generally not a dominant Orange Book molecule with meaningful brand exclusivity. For vitamin actives, listings and exclusivity are often sparse relative to prescription drugs.

Practical interpretation

- Market exclusivity for ascorbic acid tends to come from:

- product-specific NDA/BLA circumstances (if any for particular finished products),

- formulation IP, and

- supply or qualification barriers rather than Orange Book exclusivity.

What generic entry risks exist for ascorbic acid products?

Featured answer: Generic and supply entry risk is structurally high across most finished dose types because the API is commodity-grade and formulation is easy to reverse engineer, subject to quality specifications.

Main barriers

- Compliance with pharma-grade specs and stability requirements.

- Validation for dissolution/particle spec in certain tablets/capsules.

- Regulatory burden for making/labeling claims in regulated OTC contexts.

Most at-risk product types

- Standard immediate-release tablets/capsules.

- Bulk packs for supplement channels lacking proprietary formulation elements.

Do Paragraph IV challenges matter for ascorbic acid?

Featured answer: Paragraph IV is not a dominant feature of the ascorbic acid market given the typical off-patent status and commodity supply profile.

Where legal risk could surface

- Patent challenges can occur if a specific finished formulation is patented and tied to a particular branded product or protected NDA.

- The broader market still faces rapid generic substitution.

What companies compete in ascorbic acid, and how is power distributed?

Featured answer: Power is distributed across large chemical nutrition suppliers, pharmaceutical-grade ingredient producers, and downstream repackagers. The API market is fragmented with global-scale manufacturing.

Competitive tiers

- Global vitamin and chemical nutrition manufacturers

- dominate by scale and feedstock conversion.

- Ingredient traders and wholesalers

- move product across regions, manage spot pricing.

- Downstream brand owners and private labelers

- differentiate by packaging, dosing, and combinations more than the ascorbic acid core.

- Finished dose manufacturers (contract)

- win business on compliance, cost, and turnaround.

Implication for financial trajectory

- Suppliers with capacity and stable quality capture volume during shortages.

- Brand owners rely on marketing and bundle strength, but cannot sustain pricing if ingredient costs fall or substitutes gain share.

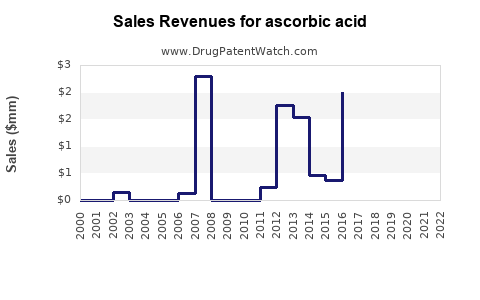

What is the financial trajectory for ascorbic acid: revenue vs margins vs earnings sensitivity?

Featured answer: Revenue generally tracks consumption volume with limited brand premium; margins are constrained by commodity pricing and competitive sourcing.

Drivers of revenue growth

- Category expansion in supplements and fortified foods.

- Expansion into OTC dosage forms with stable demand (tablets, chewables, effervescent).

- Region-level procurement cycles and contract replenishment.

Drivers of earnings volatility

- Input and energy costs shifting gross margins.

- Supply shortages increasing short-term margins for capable producers.

- Customer destocking periods compressing volume.

Typical margin structure

- Ingredient suppliers: low gross margins with strong scale economics.

- Downstream repackagers/finished goods: modest margin, sensitive to cost of goods and compliance overhead.

- Brand owners (if any): marketing-driven margins but squeezed when ingredient costs normalize and private label competes.

How do distribution channels change ascorbic acid sales performance?

Featured answer: Performance differs by channel economics: OTC retail and e-commerce are demand-led, while B2B supplement/food ingredients are contract-led with inventory cycles.

Channel characteristics

- OTC retail: promotions and bundling matter; consumers respond to price and perceived benefits.

- E-commerce: rapid SKU scaling favors low-cost private label, with demand shaped by reviews and subscription models.

- B2B ingredient contracts: smoother demand but tighter pricing and more frequent re-bids.

- Food and fortification: longer-term demand visibility tied to reformulation and processing demand.

Where are the biggest revenue exposures: dose form, strength, and geography?

Featured answer: Revenue exposure concentrates in high-volume immediate-release formats (tablet/capsule), standardized strengths, and regions with high supplement penetration.

Dose-form exposure map

- Higher volume:

- immediate-release tablets and capsules

- chewables and effervescents for consumer convenience

- Lower volume:

- specialized sustained-release systems

- sterile injectables (smaller but more regulated)

Geographic exposure map

- Regions with higher vitamin and fortified food consumption carry stronger baseline demand.

- Trade-dependent supply chains can create localized pricing spikes.

How does litigation or settlement affect the ascorbic acid market?

Featured answer: Litigation is not a dominant market driver because core IP is limited and entry is facilitated by commodity supply. Disputes usually relate to specific formulation patents for branded finished products, if any.

Where settlement can matter

- If a branded product is protected by formulation IP, settlements can define:

- “skinny” carve-outs (design-around)

- launch timing for certain competitors in specific jurisdictions.

Market-wide effect

- Even where disputes occur, rapid re-formulation and alternative supplier switching tends to limit lasting pricing uplift.

Key Takeaways

- Ascorbic acid is a commodity vitamin API with demand led by supplements, fortified foods, and OTC consumption rather than prescription exclusivity.

- Pricing and financial trajectory are primarily supply and input-cost driven, with competitive intensity limiting sustained margin expansion.

- Patent and Orange Book exclusivity are generally not central to long-run market outcomes because the active ingredient is off-patent; product-level formulation IP can exist but is typically narrow.

- Generic/supply entry risk is structurally high, especially for standard immediate-release dose forms.

- Financial performance is volume-sensitive with margins constrained by ingredient commoditization and frequent contract re-bidding.

FAQs

-

What types of finished products for ascorbic acid are most exposed to price compression?

Standard immediate-release tablets, capsules, and private-label supplement SKUs.

-

Does ascorbic acid have meaningful biosimilar or biologics risk?

No, ascorbic acid is a small-molecule vitamin ingredient and not a biologic.

-

Which demand segment matters more for overall ascorbic acid consumption: supplements or food fortification?

Both are important; fortification and food processing often provide large-scale industrial demand that can stabilize total consumption.

-

How do ingredient supply disruptions affect ascorbic acid manufacturers financially?

Short-term price increases can expand gross margins for suppliers with validated capacity, but downstream customers often renegotiate contracts quickly after stabilization.

-

What is the most common basis of differentiation in ascorbic acid OTC products?

Dose form convenience, stability/bioavailability systems, and combination formulas (multivitamin blends), not the ascorbic acid molecule itself.

References (APA)

- U.S. Food and Drug Administration. Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations. FDA.

- World Health Organization. Vitamin and mineral requirements in human nutrition and related technical guidance. WHO.

- OECD/FAO and related nutrition fortification and vitamin consumption reports (vitamin commodity market context). OECD/FAO.