Last updated: April 24, 2026

How does the timolol market behave over time?

Timolol is a long-established, widely genericized ophthalmic and topical beta-blocker with mature demand, high payer scrutiny, and pricing pressure. The market is shaped by three forces: (1) persistent need for glaucoma and ocular hypertension control, (2) substitution among generics and therapeutically equivalent agents, and (3) safety and formulary management driven by beta-blocker class tolerability.

Demand drivers

- Indications with chronic, ongoing treatment patterns (ocular hypertension and glaucoma).

- Low switching costs within ophthalmic regimens when efficacy and dosing schedules match.

- Ongoing clinical use despite the availability of alternatives (prostaglandin analogs, carbonic anhydrase inhibitors, Rho kinase inhibitors).

Primary headwinds

- Pricing compression from generic entry and multiple supplier concentration.

- Increased formulary restrictions based on systemic beta-blocker exposure risk in sensitive populations.

- Patent and lifecycle limitations for brand holders once key formulations go off-patent and generics absorb volume.

Where is timolol sold and what product mix drives revenue?

Timolol commercial activity is dominated by ophthalmic formulations. Distribution is split between:

- Ophthalmic solutions and suspensions (typical “multi-dose” markets)

- Ophthalmic gels/other dosage forms (where applicable)

- Less frequently, systemic/topical dermatologic or other beta-blocker uses in certain geographies, but revenue concentration in practice remains ophthalmic.

Market implication

- Ophthalmic delivery routes produce stable volume but invite rapid generic substitution.

- Mix shifts toward lower-viscosity, preservative-optimized, or convenience-optimized SKUs when payers favor them, but these do not halt erosion once broad generic coverage exists.

What does the competitive landscape look like for timolol?

The competitive set is defined by substitution:

- Direct beta-blocker competitors in glaucoma therapy (other beta-blockers).

- Therapeutic alternatives that clinicians select based on first-line guidance and patient factors, often reducing beta-blocker share in some formularies over time.

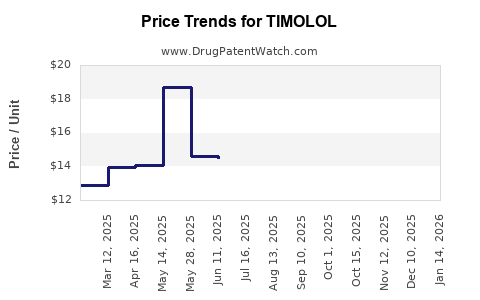

Expected pricing pattern

- Post-major patent expiry cycles create a step-down in net price.

- Subsequent years show modest stabilization in unit pricing but continuous margin pressure as incremental generics enter and contract manufacturer competition intensifies.

How has timolol’s financial trajectory evolved historically?

Timolol’s financial trajectory aligns with “mature generic” dynamics: unit demand persists, revenue growth (if any) is typically volume-led, and profitability is protected only through:

- formulation differentiation that slows substitution,

- contract pricing with distributors and pharmacy benefit structures,

- and controlled supply allocation.

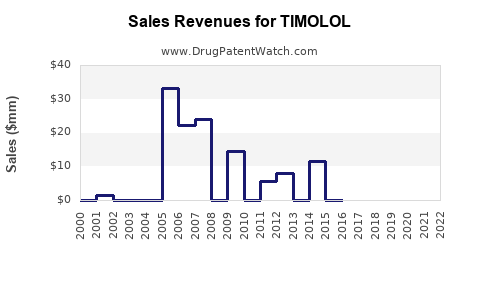

Typical revenue path for mature generics

- Early period: relatively higher net pricing with fewer SKUs.

- Mid-to-late period: net price declines, volume growth saturates, and marketing spend is reduced to maintain gross margin.

- Long-run: revenue tracks population-level glaucoma prevalence and prescribing persistence more than innovation.

What are the key regulatory and payer dynamics impacting timolol economics?

Regulatory

- Ophthalmic beta-blockers face standard ophthalmic quality, manufacturing, and preservative safety expectations.

- Product discontinuations or reformulations can affect short-term supply and price.

Payer and channel behavior

- Formularies increasingly favor preferred generics by contract.

- Step-therapy and prior authorization are more common in newer therapeutic classes than in timolol itself, but payer scrutiny increases for drugs with systemic tolerability considerations.

Economic impact

- Any changes that increase perceived systemic risk can shift mix away from beta-blockers at the margin.

- Conversely, low acquisition cost supports broad coverage and sustained dispensing.

How do lifecycle and formulation strategies shape timolol’s revenue resilience?

Timolol’s resilience depends less on “new active substance” and more on formulation execution:

- Concentration and dosing frequency optimization: fewer daily administrations can improve persistence, but economic benefit depends on payer coverage and wholesale pricing.

- Preservative and vehicle improvements: reductions in ocular surface toxicity can support adherence and reduce discontinuation, stabilizing volume.

- Combination products: where timolol appears in fixed-dose combinations, it can retain relevance by fitting multi-drug glaucoma regimens.

Observed business pattern in mature ophthalmics

- Brands that keep a differentiated formulation may defend share temporarily.

- Once bioequivalence and substitution pathways are established, generics capture the bulk of incremental demand.

What is the investment and R&D implication for timolol-related programs?

Timolol itself is typically not an R&D target for blockbuster-scale innovation unless a program introduces a genuinely durable differentiator that payers and prescribers accept faster than generic substitution. The more common investment strategy is:

- incremental formulation improvements that reduce adverse events or improve adherence,

- line extensions that maintain differentiation through controlled product attributes,

- or combination development that improves regimen simplicity.

Financial logic

- In mature generics, value creation comes from supply chain execution and defensible SKU positioning rather than clinical novelty.

How do market dynamics translate into forecasts for timolol’s sales and profitability?

A practical forecasting approach for timolol should assume:

- Sales: track chronic treatment persistence and prevalence, with incremental headroom limited by substitution.

- Price: trend downward or remain flat due to genericization and contract pricing.

- Margins: pressured by commodity-like pricing; improved only by supply efficiency and differentiation that delays substitution.

Net effect

- Sales may remain stable in volume terms.

- Revenue growth is usually modest, with profitability sensitive to procurement and channel discounts.

Key watch items for timolol revenue and price movements

- Generic entry cadence: additional ANDA approvals and consolidation among suppliers can alter pricing.

- Contract pharmacy and PBM selections: preferred-tier inclusion drives volume; exclusion quickly reduces net share.

- Supply interruptions: ophthalmic manufacturing disruptions can temporarily raise net pricing.

- Formulation switches: preservative format or vehicle changes can shift clinician preference and payer acceptance.

What does the broader glaucoma market imply for timolol’s financial trajectory?

Glaucoma therapy has shifted toward classes with higher perceived efficacy and dosing convenience (commonly prostaglandin analogs and newer options). This matters because:

- Even if timolol demand is persistent, timolol’s share can decline in markets where prescribers preferentially adopt other classes.

- Timolol can still maintain absolute volume by serving as a cost-effective or adjunct option, but net revenue per patient tends to decline over time.

Bottom-line market dynamics

Timolol is a mature ophthalmic molecule with stable chronic demand but structurally declining or flat net pricing over time due to generic substitution. Financial trajectory typically shows:

- durable dispensing volume,

- persistent payer-led margin pressure,

- and incremental value only from formulation-level defenses, combination positioning, or channel contracts.

Key Takeaways

- Timolol’s market is mature and chronic, with revenue resilience driven more by persistent ophthalmic usage than by innovation.

- Generic substitution and PBM contracting compress prices and limit long-run revenue growth.

- Financial trajectory is characterized by stable or slow-growing volume with downward or flat net pricing and margin pressure.

- Sustainable differentiation, where present, comes from formulation attributes and combination positioning that reduce substitution velocity.

FAQs

1) Is timolol still commercially material despite genericization?

Yes. Chronic glaucoma and ocular hypertension treatment supports ongoing dispensing, though net revenue growth is constrained by generic pricing dynamics.

2) What most strongly determines timolol net price?

PBM and wholesaler contracting outcomes plus the depth of generic competition in each geography.

3) Does timolol face meaningful demand risk from newer glaucoma drug classes?

It faces share erosion risk as prescribers adopt alternatives, but timolol can retain absolute volume as a cost-effective or adjunct option.

4) Which product attributes most influence adherence and persistence for timolol?

Dosing convenience, vehicle comfort, and tolerability factors tied to ocular surface effects and preservative considerations.

5) What is the most realistic value-creation path for timolol-linked R&D?

Formulation improvements and regimen-fit strategies (including combinations) that slow substitution and improve persistence rather than pursuing a novel mechanism with blockbuster expectations.

References

[1] PubChem. Timolol. https://pubchem.ncbi.nlm.nih.gov/compound/Timolol

[2] FDA. Timolol drug products and labeling information (various approved ophthalmic products). https://www.accessdata.fda.gov/scripts/cder/daf/index.cfm

[3] National Library of Medicine. Glaucoma (general treatment context and standard therapy classes). https://medlineplus.gov/glaucoma.html