PREGABALIN Drug Patent Profile

✉ Email this page to a colleague

When do Pregabalin patents expire, and when can generic versions of Pregabalin launch?

Pregabalin is a drug marketed by Actavis Elizabeth, Adaptis, Alembic, Alkem Labs Ltd, Amneal Pharms Co, Apotex, Aurobindo Pharma, Cadila Pharms Ltd, Changzhou Pharm, Chartwell Rx, Cipla, Creekwood Pharms, Dr Reddys, Eskayef, Fourrts Labs, Hetero Labs Ltd Iii, Invagen Pharms, Jubilant Generics, Lupin Ltd, Macleods Pharms Ltd, MSN, Pharmobedient, Prinston Inc, Regcon Holdings, Renata, Rising, Sciegen Pharms, Strides Pharma, Sun Pharm, Teva Pharms, Torrent, Unichem, Yiling, Zydus Pharms, Patrin, Aiping Pharm Inc, Alvogen, Epic Pharma Llc, and Rubicon Research. and is included in fifty-two NDAs.

The generic ingredient in PREGABALIN is pregabalin. There are forty-one drug master file entries for this compound. Fifty-six suppliers are listed for this compound. Additional details are available on the pregabalin profile page.

DrugPatentWatch® Litigation and Generic Entry Outlook for Pregabalin

A generic version of PREGABALIN was approved as pregabalin by ALEMBIC on July 19th, 2019.

AI Deep Research

Questions you can ask:

- What is the 5 year forecast for PREGABALIN?

- What are the global sales for PREGABALIN?

- What is Average Wholesale Price for PREGABALIN?

Summary for PREGABALIN

| US Patents: | 0 |

| Applicants: | 39 |

| NDAs: | 52 |

| Finished Product Suppliers / Packagers: | 53 |

| Raw Ingredient (Bulk) Api Vendors: | 69 |

| Clinical Trials: | 577 |

| Patent Applications: | 5,812 |

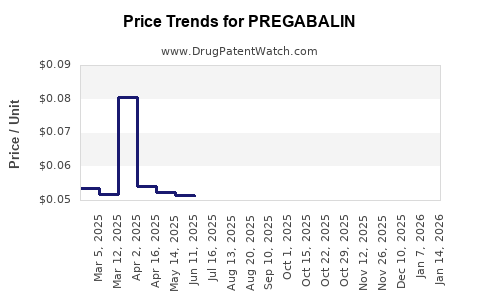

| Drug Prices: | Drug price information for PREGABALIN |

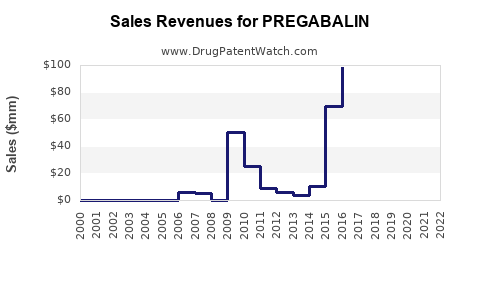

| Drug Sales Revenues: | Drug sales revenues for PREGABALIN |

| What excipients (inactive ingredients) are in PREGABALIN? | PREGABALIN excipients list |

| DailyMed Link: | PREGABALIN at DailyMed |

Recent Clinical Trials for PREGABALIN

Identify potential brand extensions & 505(b)(2) entrants

| Sponsor | Phase |

|---|---|

| McMaster University | PHASE4 |

| Eurofarma Laboratorios S.A. | PHASE3 |

| Tanta University | NA |

Medical Subject Heading (MeSH) Categories for PREGABALIN

Anatomical Therapeutic Chemical (ATC) Classes for PREGABALIN

Paragraph IV (Patent) Challenges for PREGABALIN

| Tradename | Dosage | Ingredient | Strength | NDA | ANDAs Submitted | Submissiondate |

|---|---|---|---|---|---|---|

| LYRICA CR | Extended-release Tablets | pregabalin | 82.5 mg and 165 mg | 209501 | 1 | 2018-02-02 |

| LYRICA CR | Extended-release Tablets | pregabalin | 330 mg | 209501 | 1 | 2018-01-29 |

| LYRICA | Oral Solution | pregabalin | 20 mg/mL | 022488 | 1 | 2010-05-19 |

| LYRICA | Capsules | pregabalin | 25 mg, 50 mg, 75 mg, 100 mg, 150 mg, 200 mg, 225 mg and 300 mg | 021446 | 8 | 2008-12-30 |

US Patents and Regulatory Information for PREGABALIN

| Applicant | Tradename | Generic Name | Dosage | NDA | Approval Date | TE | Type | RLD | RS | Patent No. | Patent Expiration | Product | Substance | Delist Req. | Exclusivity Expiration |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Changzhou Pharm | PREGABALIN | pregabalin | CAPSULE;ORAL | 214322-007 | Jul 15, 2021 | AB | RX | No | No | ⤷ Start Trial | ⤷ Start Trial | ⤷ Start Trial | |||

| Pharmobedient | PREGABALIN | pregabalin | TABLET, EXTENDED RELEASE;ORAL | 211948-001 | Apr 13, 2021 | DISCN | No | No | ⤷ Start Trial | ⤷ Start Trial | ⤷ Start Trial | ||||

| Sun Pharm | PREGABALIN | pregabalin | CAPSULE;ORAL | 091157-001 | Nov 29, 2019 | DISCN | No | No | ⤷ Start Trial | ⤷ Start Trial | ⤷ Start Trial | ||||

| Eskayef | PREGABALIN | pregabalin | CAPSULE;ORAL | 212988-001 | Mar 8, 2022 | AB | RX | No | No | ⤷ Start Trial | ⤷ Start Trial | ⤷ Start Trial | |||

| Teva Pharms | PREGABALIN | pregabalin | CAPSULE;ORAL | 091224-004 | Jul 19, 2019 | DISCN | No | No | ⤷ Start Trial | ⤷ Start Trial | ⤷ Start Trial | ||||

| Apotex | PREGABALIN | pregabalin | CAPSULE;ORAL | 211685-001 | Jul 7, 2021 | DISCN | No | No | ⤷ Start Trial | ⤷ Start Trial | ⤷ Start Trial | ||||

| Alkem Labs Ltd | PREGABALIN | pregabalin | CAPSULE;ORAL | 207799-006 | Jul 19, 2019 | AB | RX | No | No | ⤷ Start Trial | ⤷ Start Trial | ⤷ Start Trial | |||

| >Applicant | >Tradename | >Generic Name | >Dosage | >NDA | >Approval Date | >TE | >Type | >RLD | >RS | >Patent No. | >Patent Expiration | >Product | >Substance | >Delist Req. | >Exclusivity Expiration |

EU/EMA Drug Approvals for PREGABALIN

| Company | Drugname | Inn | Product Number / Indication | Status | Generic | Biosimilar | Orphan | Marketing Authorisation | Marketing Refusal |

|---|---|---|---|---|---|---|---|---|---|

| Zentiva k.s. | Pregabalin Zentiva k.s. | pregabalin | EMEA/H/C/004277Neuropathic painPregabalin Zentiva k.s. is indicated for the treatment of peripheral and central neuropathic pain in adults.EpilepsyPregabalin Zentiva k.s. is indicated as adjunctive therapy in adults with partial seizures with or without secondary generalisation.Generalised anxiety disorderPregabalin Zentiva k.s. is indicated for the treatment of generalised anxiety disorder (GAD) in adults. | Withdrawn | yes | no | no | 2017-02-27 | |

| Zentiva, k.s. | Pregabalin Zentiva | pregabalin | EMEA/H/C/003900Neuropathic pain, , , Pregabalin Zentiva is indicated for the treatment of peripheral and central neuropathic pain in adults., , , Epilepsy, , , Pregabalin Zentiva is indicated as adjunctive therapy in adults with partial seizures with or without secondary generalisation., , , Generalised anxiety disorder, , , Pregabalin Zentiva is indicated for the treatment of generalised anxiety disorder (GAD) in adults., , | Authorised | yes | no | no | 2015-07-17 | |

| Mylan S.A.S. | Pregabalin Mylan Pharma | pregabalin | EMEA/H/C/003962EpilepsyPregabalin Mylan Pharma is indicated as adjunctive therapy in adults with partial seizures with or without secondary generalisation.Generalised Anxiety DisorderPregabalin Mylan Pharma is indicated for the treatment of Generalised Anxiety Disorder (GAD) in adults. | Withdrawn | yes | no | no | 2015-06-25 | |

| Upjohn EESV | Pregabalin Pfizer | pregabalin | EMEA/H/C/003880Neuropathic painPregabalin Pfizer is indicated for the treatment of peripheral and central neuropathic pain in adults.EpilepsyPregabalin Pfizer is indicated as adjunctive therapy in adults with partial seizures with or without secondary generalisation.Generalised Anxiety DisorderPregabalin Pfizer is indicated for the treatment of Generalised Anxiety Disorder (GAD) in adults. | Authorised | no | no | no | 2014-04-10 | |

| Upjohn EESV | Lyrica | pregabalin | EMEA/H/C/000546Neuropathic painLyrica is indicated for the treatment of peripheral and central neuropathic pain in adults.EpilepsyLyrica is indicated as adjunctive therapy in adults with partial seizures with or without secondary generalisation.Generalised anxiety disorderLyrica is indicated for the treatment of generalised anxiety disorder (GAD) in adults. | Authorised | no | no | no | 2004-07-05 | |

| Sandoz GmbH | Pregabalin Sandoz GmbH | pregabalin | EMEA/H/C/004070EpilepsyPregabalin Sandoz GmbH is indicated as adjunctive therapy in adults with partial seizures with or without secondary generalisation.Generalised Anxiety DisorderPregabalin Sandoz GmbH is indicated for the treatment of Generalised Anxiety Disorder (GAD) in adults. | Withdrawn | yes | no | no | 2015-06-19 | |

| Accord Healthcare S.L.U. | Pregabalin Accord | pregabalin | EMEA/H/C/004024EpilepsyPregabalin Accord is indicated as adjunctive therapy in adults with partial seizures with or without secondary generalisation.Generalised Anxiety DisorderPregabalin Accord is indicated for the treatment of Generalised Anxiety Disorder (GAD) in adults. | Authorised | yes | no | no | 2015-08-28 | |

| >Company | >Drugname | >Inn | >Product Number / Indication | >Status | >Generic | >Biosimilar | >Orphan | >Marketing Authorisation | >Marketing Refusal |

More… ↓