Last updated: June 20, 2026

Pregabalin Market Dynamics and Financial Trajectory (Revenue, Pricing, Exclusivity, and Patent/Generic Transition)

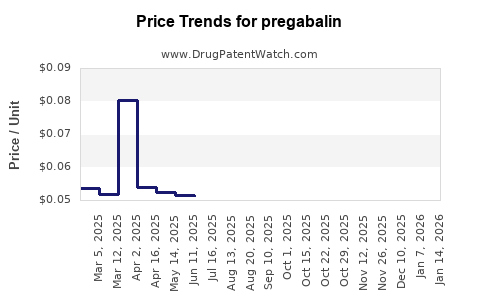

Pregabalin revenue is structurally shaped by (1) broad generic penetration across most major markets, (2) continuing demand growth in neuropathic pain and adjunct indications, and (3) incremental pricing pressure driven by multi-source supply. In the U.S., FDA-reviewed generics dominate because the brand’s remaining patent-driven exclusivity has long since ended for most formulations. Financial trajectory depends more on volume, payer restrictions, and substitution rates than on premium pricing or near-term brand patent leverage.

The market is large but commoditizing. Competitive advantage tends to shift to supply reliability, formulary positioning, and managed entry outcomes rather than to new molecule differentiation.

What drives pregabalin market dynamics (pricing, volume, payer substitution, and competition)?

Pregabalin is a systemic, oral alpha-2-delta calcium channel modulator used for neuropathic pain and other approved indications. The market is characterized by generic multiplicity and steady substitution, which compresses prices and increases the share of lowest-cost or preferred products.

Key demand drivers for pregabalin

- Neuropathic pain prevalence: diabetic peripheral neuropathy, postherpetic neuralgia, and other neuropathic pain syndromes.

- Adjunct use patterns: pregabalin is used for fibromyalgia and seizure adjunct indications in jurisdictions where approved.

- Treatment persistence: chronic use supports baseline demand even when unit pricing declines.

Key supply and competition drivers

- Multi-source generic availability: in mature markets, multiple ANDA products compete on price and packaging/form strength.

- Formulation and package line competition: extended-release variants exist in the market globally, but in many markets generics and payers determine economics more than brand differentiation.

- Manufacturing scale and regional supply: shortages or quality events can move short-term prices upward, but long-run dynamics revert to competitive equilibrium.

Pricing mechanics

- Reimbursement-led pricing: payer formularies and preferred drug lists are decisive.

- Wholesale acquisition cost compression: brand pricing loses relevance as generics capture volume.

- Net price vs list price gap: rebates and discounts dominate observed financial outcomes for large distributors and PBM-influenced settings.

Implication for financial trajectory: revenue growth, where it exists, typically comes from volume growth and expanded formularies, not from sustained premium pricing.

How is pregabalin performing financially (revenue trajectory and profit sensitivity to price erosion)?

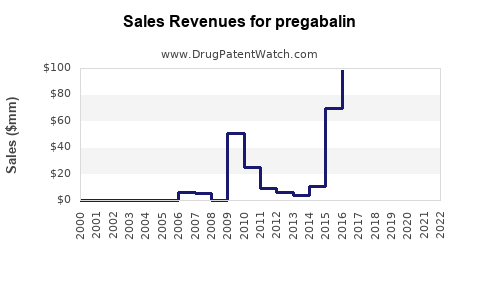

Pregabalin’s financial trajectory follows a standard small-molecule commodity pattern once generic entry matures:

- Pre-generic/brand premium period: brand holds pricing power; revenue tracks demand growth plus premium pricing.

- Early generic ramp: volume shifts quickly; net price declines; overall revenue becomes less profitable per unit.

- Mature multi-generic phase: revenue is stable only if volume and/or patient count increases enough to offset ongoing price erosion.

- Late-cycle optimization: manufacturers compete on margins through sourcing, contract manufacturing, and manufacturing yield, not on exclusivity.

Profit sensitivity

- Gross margin declines with price: multi-source competition compresses unit economics.

- Working capital and supply chain: commodity returns are sensitive to inventory turns and freight/COGS inflation.

- Litigation and at-risk launch exposure: Paragraph IV or infringement risk does not remove long-run price pressure once supply is established.

Implication: even when total prescriptions rise, category revenue can plateau or fall if per-unit net price declines faster than volume grows.

When does pregabalin lose exclusivity, and what does that mean for financial trajectory?

For pregabalin, the critical point for most major geographies is that key brand exclusivities and patent protections have already expired for the base immediate-release product in mature markets. That sets up the current market structure: generics dominate and brand revenue is limited.

Exclusivity framework that shapes “late financial” outcomes

- Composition-of-matter patents typically drive the early exclusivity window.

- Formulation/polymorph/dosage form patents can extend protection for specific SKUs if they exist and remain unexpired.

- Regulatory exclusivity (e.g., data exclusivity) is generally not a binding long-term barrier for generics in a commoditized category once ANDA pathways are established.

Implication for finance: the market has moved beyond exclusivity-led premium returns. The category’s future trajectory is largely independent of brand patent leverage and instead driven by payer substitution and competitive pricing.

What patents protect pregabalin (composition, formulations, methods of use), and how do they affect revenue?

Pregabalin patent estates are typically dominated by early-life composition claims and secondary claims that may cover particular formulations or dosing regimens. As the estate ages, the practical impact on economics shifts:

- If secondary formulation patents are expired: no SKU-specific price premium remains.

- If secondary patents persist in specific jurisdictions: they can delay generic entry for certain strengths or delivery technologies.

Revenue impact logic

- Patent strength affects launch timing, but once multi-generic penetration is achieved, revenue is driven mainly by category volume and contracting dynamics.

- Even delayed entry produces limited uplift because other generics still compete and payers often switch to alternatives.

What is the Orange Book status of pregabalin in the US?

Orange Book listings for pregabalin products generally show extensive generic presence with active and inactive patents varying by product/strength. In the U.S. market, the practical takeaway for financial trajectory is that:

- brands are not positioned for long-term pricing control

- category revenue is constrained by generic substitution

(Orange Book data is product-specific, strength-specific, and changes with patent term status and listing updates.)

What Paragraph IV challenges and generic entry risks exist for pregabalin?

Once a molecule is fully generic in major markets, Paragraph IV dynamics typically become:

- low incremental risk to category pricing for immediate-release pregabalin because supply is already entrenched

- selective risk for any remaining late-expiring formulation or method-of-use claims for specific SKUs, strengths, or new release formats

Financial implication: litigation can shift short-term market share between manufacturers, but category-wide revenue effects are usually muted once a multi-source market is established.

How does pregabalin compare with other gabapentinoids (gabapentin, duloxetine, topiramate) on market trajectory?

Pregabalin vs gabapentin

- Substitution dynamics: gabapentin also faces high generic penetration and payer-driven substitution.

- Differentiation: pregabalin can capture share where prescriber preference or formulary design favors it, but commoditization persists.

Pregabalin vs duloxetine

- Class and formulary competition: duloxetine is brand-to-generic transitioned in many markets and can compete for neuropathic pain with differing side-effect and payer dynamics.

- Revenue path: duloxetine tends to be less “mechanically” linked to supply compression in some markets because of different payer channels and competition breadth, though it is still exposed to generic price pressure where applicable.

Implication: pregabalin’s trajectory is primarily a volume-and-price function against other neuropathic pain options and generic gabapentinoids, not a high-exclusivity play.

Which companies are key players for pregabalin (generic manufacturers and distributors), and how does that shape pricing?

Pricing is influenced by the number of credible ANDA holders, regional distribution strength, and contracting behavior with wholesalers and PBMs. In mature markets, the category tends to consolidate around:

- large generic manufacturers with scale economics

- preferred supplier status via formulary and rebate contracting

- supply continuity that reduces payer risk

Financial implication: revenue is often “won” through channel access and contracting, not through patent-driven exclusivity.

How do manufacturing capacity and supply disruptions affect pregabalin revenue and margins?

In commodity pharmaceuticals, short-term price and margin shifts happen when supply tightens:

- quality issues

- plant outages

- raw material constraints

- regulatory enforcement actions

However, because multi-source manufacturing exists in most mature markets, supply shocks tend to be transient and corrected by additional supply.

Financial implication: volatility in quarterly results can occur, but long-run trend remains anchored by competitive multi-source pricing.

What generic entry scenarios could materially change pregabalin market share or revenue?

Material changes typically require one of these events:

- new formulation entry that changes payer preference (e.g., specific release profile, pack sizes, or coverage expansion)

- resolution of remaining jurisdiction-specific patent barriers for a particular SKU

- major competitor withdrawal that removes low-cost supply and temporarily raises pricing

- manufacturing scale expansion that reduces costs and triggers aggressive pricing for share gains

For most immediate-release pregabalin markets, the “generic entry” story is mostly complete; the remaining scenarios are more about supply economics than molecule risk.

How does FDA regulatory status affect pregabalin market dynamics (ANDAs, labeling, and interchangeability)?

In the U.S., FDA approval and labeling control the mechanics of:

- ANDAs obtaining permission to market

- therapeutic equivalence and substitution

- pharmacovigilance and risk communications that affect prescribing behavior

Even in a mature category, FDA-driven labeling updates can influence:

- switching rates

- payer rules for coverage

- physician willingness to substitute

Financial implication: regulatory updates generally affect share and persistence more than they re-enable premium pricing.

Key Takeaways

- Pregabalin is in a mature, multi-generic market where financial outcomes are driven by volume, payer contracting, and net price compression.

- Patent and exclusivity effects have largely transitioned to a secondary role; the category’s trajectory is now set by generic competition and supply economics.

- Litigation and Paragraph IV events can shift share among manufacturers, but category-wide revenue uplift is limited once multi-source penetration is entrenched.

- Near-term financial variability is most likely to come from supply continuity and channel contracting, not from renewed exclusivity.

FAQs

1) Will pregabalin still grow revenue as generics dominate?

Growth depends on prescription volume and persistence, plus favorable payer placement. Net revenue can grow only if unit price declines slow enough to be offset by utilization increases.

2) Do pregabalin extended-release products change the competitive landscape?

They can shift payer preference if coverage and interchangeability dynamics support the SKU. Otherwise, they compete within the same commodity pressure from generics.

3) How do patent settlements for pregabalin typically affect the timing of generic launches?

Settlements usually delay entry for the specific disputed product/SKU/market and can reallocate share to incumbents. Once entry occurs broadly, pricing pressure resumes.

4) What risks matter most for pregabalin manufacturers financially?

Margin volatility driven by price compression, supply reliability, and channel rebate/contract terms outweigh incremental patent risks in most mature markets.

5) What data best predicts pregabalin quarterly financial swings?

Rx volume trends, net price (after rebates/discounts), and supply availability indicators tend to correlate more with quarterly revenue and gross margin movement than exclusivity milestones.

References (APA)

- U.S. Food and Drug Administration. Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations. https://www.accessdata.fda.gov/scripts/cder/daf/

- FDA. Drug Approval Package for pregabalin products (varies by NDA/ANDA). https://www.accessdata.fda.gov/drugsatfda/