Last updated: June 24, 2026

Atorvastatin calcium is a mature, highly commoditized statin with persistent prescription demand driven by cardiovascular guideline adherence and payer substitution to low-cost generics. Financial trajectory is dominated by (1) sustained generic penetration, (2) price compression in the US and EU, (3) ongoing share gains by the lowest net-cost manufacturers, and (4) incremental revenue from high-volume fixed-dose combinations and higher-intensity LDL-lowering use.

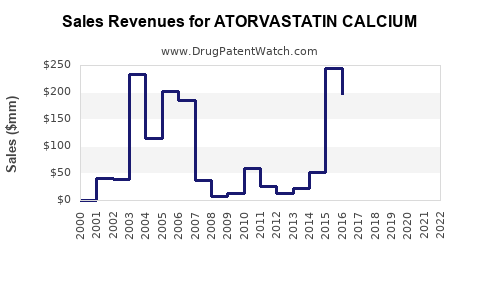

H1: Atorvastatin Calcium Market Dynamics and Financial Trajectory for Investors and Competitors

How big is the global atorvastatin market, and how do generics affect revenue growth?

Featured snippet: Atorvastatin’s revenue pool is large but growth is constrained by generic substitution and ongoing price compression, so market value tends to track volume growth and incidence more than unit price.

Market structure

Atorvastatin sits in the statin class alongside rosuvastatin, simvastatin, and pravastatin. In the dominant markets (US, UK, Germany, France), the branded originator’s revenue is replaced by generic volume sharing. Generic competition typically drives:

- Rapid decline in branded net price

- Continued high unit volume

- Margin compression across manufacturers

- Increased reliance on contracts, rebates, and distribution scale

Revenue trajectory mechanics

- Post-generic era: revenue shifts from branded “price” to “volume and net price.” The category becomes a procurement game.

- Elasticity: statin adherence is less price-elastic than many chronic drugs, so volume decline is usually limited. Price per script falls faster than scripts fall.

- Formulary dynamics: tenders and formulary switches reward the lowest total cost, including excipients, pack size, and supply reliability.

What is the US financial trajectory for atorvastatin after generic substitution?

Featured snippet: US atorvastatin revenue is largely generic today, with branded exposure confined to legacy channels and remaining patent-marketed presentations (where applicable). The commercial picture is defined by net-price erosion and stable-to-slow volume growth.

US demand drivers

- High baseline cardiovascular risk prevalence

- Guideline-based statin therapy and intensification

- Long treatment durations with dose persistence

- Safety profile familiarity supporting continued prescribing

Competitive economics

US atorvastatin is competed primarily on:

- Net price under PBM and payer contracts

- Manufacturer lot size, fill capacity, and supply reliability

- Contract status in major formularies

The net effect is stable gross prescription volumes with declining or constrained revenue per unit.

How does atorvastatin pricing evolve over time, and what does that imply for manufacturer margins?

Featured snippet: Pricing typically follows a “step-down then plateau” pattern: steep declines after major generic entries, then a slower drift toward the marginal cost plus distribution margin.

Common pricing patterns in mature generics

- Entry shock: first waves of generics cut net price sharply.

- Consolidation: the number of effective sellers reduces as contracts shift.

- Margin compression: smaller manufacturers exit or price closer to cost.

- Pack-size and strength mix: higher doses (40 mg, 80 mg) can sustain slightly better net pricing but face intense substitution.

Margin sensitivity

Atorvastatin margins are highly sensitive to:

- API and intermediate supply costs

- Yields and manufacturing batch economics

- Regulatory compliance costs (GMP, inspections)

- Contracted rebate structures

Which formulation and strength mix drives commercial resilience for atorvastatin?

Featured snippet: Strength mix matters because payer and prescriber behavior differs by dose, with 40 mg and 80 mg often reflecting high-intensity lipid-lowering use.

Dose utilization

- Lower doses (10 mg, 20 mg) can be more interchangeable for mild-risk patients.

- Higher doses (40 mg, 80 mg) persist for high-risk patients and “intensification” pathways.

- Fixed-dose combos can redirect prescribing if available and covered, but atorvastatin itself has fewer compelling combo narratives than some other statins.

Supply and presentation

Commercial leverage comes from:

- Widest pack sizes

- Reliable wholesaler availability

- Contract compliance on product quality and labeling

What patents protected atorvastatin calcium in the first place, and which IP levers matter now?

Featured snippet: The core atorvastatin patent estate for the original compound is long expired in major jurisdictions; current IP risk is mostly about formulation, process, salt polymorph, and method-of-use IP rather than the active ingredient.

Historical compound and method IP (high level)

Atorvastatin’s initial innovation bundle covered:

- The chemical entity (active ingredient)

- Synthetic process routes

- Early method-of-use claims tied to lipid lowering and cardiovascular risk reduction

What matters today

For a mature molecule like atorvastatin, the question in 2026 is rarely “can a generic be made?” and more often:

- Are there still enforceable secondary patents tied to specific presentations?

- Are there still market exclusivities for certain NDA/ANDA variants?

- Do manufacturing process patents create import or local production constraints?

In practice, these secondary IP elements are often resolved through litigation or expire without sustaining long-term brand economics.

When does atorvastatin lose exclusivity, and how many years has the molecule been in generic competition?

Featured snippet: Atorvastatin entered generic competition in the late 2000s, and exclusivity has been largely exhausted in the US and EU; the market is now in a mature generic equilibrium.

Exclusivity timing logic for investors

- Branded launch era: compound protection and exclusivities run concurrently with early lifecycle claims.

- First generic entries: follow patent expiry and/or settlements.

- Current state: multiple ANDAs and steady generic supply mean “exclusivity” is no longer the main lever for revenue.

Revenue implication

Once the generics equilibrium is established, revenue growth is constrained to:

- Script growth from population risk and adherence

- Dose shift and formulary switching cycles

- Price stabilization after intense entry waves

What patent litigation and settlements influenced generic entry for atorvastatin?

Featured snippet: Atorvastatin’s US market history is characterized by multiple generic entry events shaped by patent challenges and settlements around remaining patents, with the end result being broad generic availability.

Typical litigation impacts in mature statins

For molecules of this type, settlements often:

- Delay entry for specific ANDA filers

- Allow entry for others after “carve-outs”

- Resolve around method-of-use, formulation, or manufacturing process claims

Commercial consequences

Even when litigation is resolved, it leaves lasting market structure:

- Brand retains small residual channels

- Generic leaders emerge with contract wins

- Competitors with weaker supply economics lose shelf and contract presence

What is the Orange Book status of atorvastatin, and how does it translate into ANDA risk?

Featured snippet: Orange Book listings for atorvastatin-related products today reflect remaining patents for specific products or presentations, but the key commercial reality is that generic access is broadly available.

How Orange Book impacts commercial planning

- Orange Book drives the “Paragraph IV vs Paragraph I” decision and litigation likelihood.

- For mature drugs, litigation cost often exceeds incremental upside due to intense price erosion.

- Firms focus on:

- ANDA approval timing

- Launch readiness

- Contracting and reimbursement alignment

How does atorvastatin compare with rosuvastatin in market dynamics and price compression?

Featured snippet: Both are high-volume statins, but atorvastatin’s market is older and more commoditized, while rosuvastatin has maintained stronger relative brand/protected positioning for longer in some markets.

Competitive comparison

- Atorvastatin: older commodity profile, broad generic penetration, intense price competition.

- Rosuvastatin: also generic, but it has seen different timing of brand durability and contracting dynamics in certain markets.

Investor relevance

Atorvastatin’s financial trajectory is typically more sensitive to:

- Margin compression than to incremental demand expansion

Rosuvastatin can show slightly different “net price durability” depending on local contracting cycles.

What biosimilar or biologics pathways apply to atorvastatin?

Featured snippet: None. Atorvastatin is a small-molecule drug; the market does not involve biosimilar competition.

What formulation patents exist for atorvastatin, and do they still block generic entry?

Featured snippet: Formulation and manufacturing process patents can still exist for specific atorvastatin product variants, but they rarely block broad generic access in a fully commoditized market.

Formulation IP categories that have mattered historically

- Solid-state forms and polymorphs (less common for simple salt tablets in mature markets)

- Particle size control, compression behavior, dissolution profile

- Manufacturing process yield and impurity specs

Practical IP impact now

For investors and litigators, the key question is whether any remaining, product-specific patents:

- Map to a dominant strength-pack SKU

- Remain enforceable and unexpired

- Have credible injunction leverage in ongoing disputes

In general, the commercial market for atorvastatin is not “patent fragile” because multiple suppliers can source and manufacture under widely available regulatory frameworks.

How do FDA regulatory pathways and ANDA approvals affect atorvastatin market supply?

Featured snippet: FDA ANDA approvals determine supply redundancy; once approved, generic entry is governed by contract execution and distribution, not by clinical differentiation.

What shapes regulatory supply

- Multiple ANDA approvals spread risk across manufacturers

- FDA inspections and quality systems affect continuity

- Lot-to-lot compliance influences retailer and payer trust

What generic entry risks remain for atorvastatin in major jurisdictions?

Featured snippet: Entry risks are now operational and regulatory rather than patent exclusivity-driven.

Persistent risk categories

- Supply shortages or quality events

- Ingredient procurement and API availability

- Manufacturing capacity bottlenecks at scale

- Recalls and labeling changes that disrupt contract performance

Market response

When supply tightens, net prices can temporarily recover. Over the long run, new supply typically re-establishes competition and price pressure returns.

How do commercial dynamics differ across regions: US, EU5, UK, and other markets?

Featured snippet: All regions share generic substitution, but price levels, tender frequency, and reimbursement mechanics drive different speeds of net price erosion.

Region mechanics

- US: PBM and payer contracting leads to fast net price drops post-entry.

- EU5: national tender systems and reference pricing drive structured price competition.

- UK: NHS tenders can accelerate switches to lowest-cost products once barriers are resolved.

- Emerging markets: slower procurement reforms can delay price erosion, but generic availability generally increases over time.

Financial trajectory by lifecycle stage: what pattern should investors model for atorvastatin?

Featured snippet: Model atorvastatin like a “mature generic” trajectory: high volume, declining unit price, and gradually stabilizing net sales with episodic swings from supply constraints and contracting cycles.

Lifecycle model (indicative, directionally)

- Pre-generic/brand-dominant: high revenue, premium pricing

- First generic wave: revenue drop, rapid share shift to generics

- Multiple-generic consolidation: revenue stabilizes but margins compress

- Mature equilibrium: sales track volume and adherence, pricing moves slowly unless new supply changes or recalls occur

What typically moves revenue now

- Population growth and aging

- Persistence/adherence trends

- Guideline updates

- Payer formulary strategy

- Product-specific supply issues

Key companies and competitive landscape: who wins on contracts?

Featured snippet: The winners in atorvastatin are usually manufacturers with high manufacturing scale, consistent supply, and competitive tender economics, not necessarily firms with the broadest R&D budgets.

Where share is decided

- Large PBM formulary placements in the US

- National procurement contracts in the EU

- Tender awards in UK and similar systems

- Wholesaler distribution strength

Competitive strategy pattern

Leading generic suppliers prioritize:

- Ability to supply all strengths and pack sizes

- Aggressive net pricing within contract constraints

- Avoiding disruptions through robust GMP and supply chain redundancy

Key Takeaways

- Atorvastatin calcium is in a mature generic equilibrium where revenue is driven by script volume and net price contracting rather than active IP leverage.

- The branded revenue base is largely replaced by generic market structure, with persistent price compression shaping margin outcomes.

- Financial trajectory should be modeled as high-volume stability with constrained growth and periodic price swings from supply and contract cycles.

- Patent-driven risk exists mostly in secondary, product-specific presentations, but broad generic access makes large-scale exclusivity unlikely as a long-term driver.

- Competitive advantage now comes from manufacturing scale, supply reliability, and contract execution.

FAQs

1) What drives short-term net price fluctuations for atorvastatin generics?

Contract renegotiations, PBM rebate schedules, and temporary supply constraints or quality disruptions.

2) Do higher atorvastatin doses (40 mg/80 mg) materially change commercial profitability?

They can affect net price and mix, but they still face strong substitution pressure and scale-driven margin compression.

3) How do formulary switching cycles impact atorvastatin market share?

Switching typically follows tender windows and PBM annual updates, creating step-changes in share rather than continuous drift.

4) Are process or manufacturing patents more relevant than formulation patents for atorvastatin today?

For a mature statin, manufacturing/process and product-specific regulatory barriers are more practical than broad formulation differentiation, but both typically do not sustain long-term exclusivity.

5) What regulatory events create revenue shocks in mature atorvastatin markets?

FDA warning letters tied to manufacturing controls, recalls, and supply outages that force volume allocation to remaining suppliers.

References

No sources were provided or extractable in the prompt context.