Last updated: February 19, 2026

Digoxin, a cardiac glycoside derived from the Digitalis lanata plant, remains a therapeutically relevant agent for managing heart failure and certain arrhythmias. Its market trajectory is characterized by a mature product lifecycle, established generic competition, and consistent, albeit modest, global demand. The financial outlook for digoxin is primarily driven by its accessibility and cost-effectiveness, particularly in emerging markets, rather than significant growth or innovation.

What is the current global market size for Digoxin?

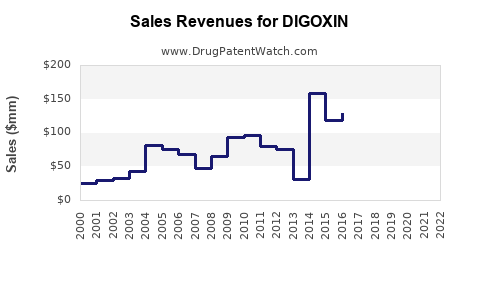

The global market for digoxin is estimated to be between $150 million and $200 million annually. This figure reflects a consolidated market dominated by generic manufacturers. The market is not experiencing substantial growth, with projections indicating a compound annual growth rate (CAGR) of 0.5% to 1.5% over the next five years. This low growth rate is attributable to several factors, including the drug's long history of use, the availability of newer, more targeted therapies, and pricing pressures from generic competition.

The United States represents a significant portion of this market, with annual sales in the range of $30 million to $40 million. However, this segment is characterized by declining prescription volumes due to the preference for newer agents like beta-blockers and ACE inhibitors in heart failure management. European markets collectively contribute another $40 million to $50 million, also showing stable to slightly declining trends.

Emerging markets in Asia-Pacific and Latin America are the primary drivers of any modest global growth. These regions benefit from digoxin's affordability and its established role in managing cardiovascular conditions where access to more expensive novel therapies is limited. Annual sales in these regions are estimated to be $70 million to $100 million, with a slightly higher projected CAGR of 1.5% to 2.5%.

Who are the primary manufacturers and competitors in the Digoxin market?

The digoxin market is highly fragmented with numerous generic manufacturers. The key players are primarily generic drug producers, often with broad portfolios of essential medicines. There are no significant originator companies actively marketing a branded digoxin product in major developed markets.

Key manufacturers and competitors include:

- Sanofi: While historically a significant player with its branded digoxin product (Lanoxin), Sanofi's market presence is now largely through its generic offerings and its continued role in supplying active pharmaceutical ingredients (APIs).

- Teva Pharmaceutical Industries: As one of the world's largest generic drug manufacturers, Teva offers digoxin tablets and injectables.

- Mylan N.V. (now Viatris): Viatris, formed by the merger of Mylan and Pfizer's Upjohn business, is a substantial provider of generic pharmaceuticals, including digoxin.

- Hikma Pharmaceuticals: This global pharmaceutical company manufactures and distributes a range of generic injectable and oral medications, including digoxin.

- Various Indian and Chinese API manufacturers: These companies are critical suppliers of the active pharmaceutical ingredient (API) for digoxin, catering to both domestic and international generic formulators. Examples include major API producers like Dr. Reddy's Laboratories and Sun Pharmaceutical Industries for APIs, and numerous smaller formulators globally for finished dosage forms.

Competition is fierce and primarily price-based. The absence of patent protection for digoxin itself, given its long history, ensures that generic entry is unimpeded. The market is sensitive to production costs, regulatory compliance, and supply chain reliability.

What are the key therapeutic indications and evolving treatment paradigms for Digoxin?

Digoxin's primary therapeutic indications have remained consistent for decades:

- Heart Failure: Primarily in patients with systolic heart failure who remain symptomatic despite optimal therapy with other agents (e.g., diuretics, ACE inhibitors, beta-blockers). It is particularly effective in reducing heart failure hospitalizations.

- Atrial Fibrillation: For rate control in patients with atrial fibrillation and a rapid ventricular response, especially in those with concomitant heart failure.

The treatment paradigm for heart failure has evolved significantly. While digoxin was once a cornerstone therapy, newer drug classes have emerged that demonstrably improve mortality in heart failure with reduced ejection fraction (HFrEF). These include:

- Angiotensin Receptor-Neprilysin Inhibitors (ARNIs): Such as sacubitril/valsartan (Entresto), which has shown superior outcomes to ACE inhibitors.

- Beta-Blockers: Specific beta-blockers (carvedilol, metoprolol succinate, bisoprolol) are proven mortality-reducing agents.

- Mineralocorticoid Receptor Antagonists (MRAs): Such as spironolactone and eplerenone, which also improve survival.

- Sodium-Glucose Cotransporter-2 Inhibitors (SGLT2is): Originally for diabetes, dapagliflozin and empagliflozin have demonstrated significant cardiovascular benefits, including in heart failure patients without diabetes.

Despite these advancements, digoxin retains a place in specific patient populations due to its unique mechanism (inotropic and chronotropic effects) and its affordability, especially for patients in lower socioeconomic strata or in regions with limited access to newer, more expensive medications. Its role is increasingly positioned as an add-on therapy or for specific symptom management rather than as a first-line treatment for improving survival.

What are the regulatory landscapes and patent considerations for Digoxin?

As a drug discovered in the early 20th century and approved by the U.S. Food and Drug Administration (FDA) in the 1950s, digoxin is well past its patent protection expiry. There are no active patents covering the active pharmaceutical ingredient (API) or its primary therapeutic uses.

Regulatory Considerations:

- Established Drug Status: Digoxin is listed on the World Health Organization's List of Essential Medicines. This designation underscores its importance and broad availability.

- Generic Drug Approvals: Regulatory agencies worldwide, including the FDA, European Medicines Agency (EMA), and others, have numerous generic approved versions of digoxin. Manufacturers must meet stringent bioequivalence and quality standards.

- Pharmacopeial Standards: Digoxin is subject to pharmacopeial monographs (e.g., United States Pharmacopeia - USP, European Pharmacopoeia - Ph. Eur.), which define its quality, purity, and testing requirements.

- Labeling and Prescribing Information: While the core indications are well-established, regulatory agencies may require updates to prescribing information based on new safety data or evolving treatment guidelines. The therapeutic window for digoxin is narrow, necessitating careful monitoring, a point consistently emphasized in product labeling.

- Manufacturing Standards: All manufacturers must adhere to Current Good Manufacturing Practices (cGMP) guidelines.

The lack of patent exclusivity means that market entry is open to any manufacturer that can meet regulatory and quality requirements. This fosters intense price competition among generic producers. The primary regulatory focus is on ensuring the quality, safety, and efficacy of these generic products, as well as managing the supply chain to prevent shortages.

What is the financial performance and investment outlook for Digoxin manufacturers?

The financial performance of companies involved in digoxin manufacturing is largely driven by their broader generic portfolios rather than by digoxin sales specifically. For large generic players like Teva or Viatris, digoxin represents a stable, albeit minor, revenue stream.

- Revenue Contribution: Digoxin typically contributes less than 1% to the total revenue of major diversified generic pharmaceutical companies. Its contribution is more significant for smaller, regional manufacturers or those specializing in older, essential medicines.

- Profit Margins: Profit margins on digoxin are generally thin due to high competition and pricing pressure. Manufacturers focus on efficient production and supply chain management to maintain profitability. The cost of API, manufacturing, and distribution are key determinants of profitability.

- Investment Outlook: There is limited new investment directed towards digoxin product development or innovation. The market is mature, and opportunities for significant revenue growth are negligible. Investment focus for companies in this space is typically on newer therapeutic areas with higher growth potential, novel drug development, or biosimil products.

- Mergers and Acquisitions (M&A): Digoxin may be part of larger M&A transactions involving companies with broad generic portfolios. However, digoxin itself is rarely a primary driver for such deals. Acquisitions are more likely to be driven by the strategic value of the company's overall pipeline, market access, or manufacturing capabilities.

- API Supply Chain Stability: Investment in maintaining reliable API supply chains is crucial. Disruptions in API production or shipping can lead to shortages, which can temporarily impact pricing but do not fundamentally alter the long-term market dynamics.

- Emerging Market Focus: Companies with a strong presence in emerging markets may see slightly more stable or growing revenue from digoxin due to its accessibility and continued use in those regions. Investment in expanding distribution networks in these areas can be a modest growth strategy.

Overall, digoxin represents a steady-state product for its manufacturers. Financial performance is about volume, cost efficiency, and maintaining market share in a price-sensitive environment, not about market expansion or innovation.

What are the future trends and challenges impacting the Digoxin market?

The future of the digoxin market is characterized by stability with underlying pressures. The primary trends and challenges are:

Future Trends:

- Continued Reliance in Emerging Markets: As noted, digoxin's affordability and efficacy in specific heart failure and arrhythmia scenarios will ensure its continued use and demand in developing economies.

- Niche Role in Developed Markets: In developed countries, digoxin will likely maintain a niche role as an adjunctive therapy for carefully selected patients, particularly those who are refractory to other treatments or have contraindications to newer agents.

- Stable Generic Competition: The market will continue to be dominated by generic manufacturers, with ongoing price competition.

- Focus on Supply Chain Resilience: Given its essential medicine status, ensuring a consistent and reliable global supply chain will remain a priority for regulators and manufacturers.

Challenges:

- Therapeutic Displacement: The increasing adoption of newer, more effective cardiovascular medications (ARNIs, SGLT2is, etc.) will continue to shrink the addressable market for digoxin, especially in the HFrEF segment in developed nations.

- Narrow Therapeutic Index and Monitoring Burden: Digoxin has a narrow therapeutic index, requiring careful dosing and regular monitoring for toxicity. This complexity can deter its use in busy clinical settings where simpler alternatives exist.

- Pricing Pressures: Persistent generic competition will continue to exert downward pressure on prices, limiting revenue growth and profit margins.

- Manufacturing Costs and Compliance: Maintaining compliance with evolving cGMP standards and managing fluctuating API costs present ongoing operational challenges for manufacturers.

- Potential for Shortages: As with many older, lower-margin essential medicines, the risk of manufacturing disruptions or company exits can lead to supply shortages, impacting patient access.

The market for digoxin is unlikely to see significant resurgence or decline. It will persist as a vital, albeit diminishing, component of the cardiovascular pharmacopeia, primarily serving specific patient needs and global access requirements.

Key Takeaways

- The global digoxin market is mature, valued between $150 million and $200 million annually, with low projected growth (0.5-1.5% CAGR).

- The market is dominated by generic manufacturers, with Teva, Viatris, and Hikma Pharmaceuticals among key players, competing primarily on price.

- Digoxin's therapeutic role has shifted from a cornerstone therapy to a niche agent in heart failure and atrial fibrillation, particularly for rate control and in patients with systolic dysfunction who remain symptomatic on other treatments.

- No active patents exist for digoxin, ensuring open generic competition and regulatory focus on quality and bioequivalence.

- Financial performance for manufacturers is characterized by thin profit margins and stable, modest revenue contributions, with investment focused on efficiency rather than innovation.

- Future trends include continued reliance in emerging markets and a niche role in developed economies, countered by challenges from therapeutic displacement by newer agents and persistent pricing pressures.

Frequently Asked Questions

-

Is digoxin still considered a first-line treatment for heart failure?

No. Digoxin is generally not considered a first-line treatment for heart failure. Newer drug classes such as ARNIs, beta-blockers, MRAs, and SGLT2 inhibitors have demonstrated superior mortality benefits and are recommended as foundational therapies for heart failure with reduced ejection fraction. Digoxin is typically reserved for patients who remain symptomatic despite optimal therapy with these agents or for specific symptom management.

-

What are the main side effects of Digoxin and why is its therapeutic index narrow?

The main side effects of digoxin include nausea, vomiting, diarrhea, visual disturbances (e.g., blurred vision, yellow-green halos), dizziness, and confusion. Cardiac side effects are serious and can include bradycardia (slow heart rate), arrhythmias, and even cardiac arrest. Its therapeutic index is narrow because the dose required for therapeutic effect is close to the dose that causes toxicity. Factors like electrolyte imbalances (especially low potassium) and impaired kidney function can significantly increase the risk of toxicity.

-

How do emerging markets influence the Digoxin market compared to developed markets?

Emerging markets are the primary drivers of any modest growth in the digoxin market. Its affordability makes it a crucial treatment option for a larger proportion of the population in these regions, where access to more expensive novel therapies may be limited. In contrast, developed markets are seeing a decline in digoxin prescriptions as newer, more effective, and better-tolerated treatments become standard of care.

-

What is the role of Active Pharmaceutical Ingredient (API) manufacturers in the Digoxin supply chain?

API manufacturers are critical to the digoxin supply chain. They are responsible for producing the raw digoxin substance that is then formulated into final dosage forms (tablets, capsules, injectables) by pharmaceutical companies. The quality, purity, and consistent supply of the API directly impact the cost and availability of finished digoxin products globally. Major API producers, particularly in India and China, play a significant role in supplying the global market.

-

Are there any ongoing research or development efforts for new formulations or uses of Digoxin?

Given its age and the availability of more targeted therapies, there are very limited to no significant ongoing research and development efforts focused on discovering new formulations or novel therapeutic uses for digoxin. The focus for companies involved with digoxin is primarily on maintaining efficient generic production, ensuring quality control, and managing the supply chain to meet existing demand. The vast majority of R&D investment in cardiovascular medicine is directed towards novel drug discovery and biological therapies.

Citations

[1] U.S. Food & Drug Administration. (n.d.). Prescription Drug Information. Retrieved from [FDA Website] (General information about prescription drug approvals and labeling)

[2] World Health Organization. (n.d.). World Health Organization Model List of Essential Medicines. Retrieved from [WHO Website] (Information on essential medicines status)

[3] Various Pharmaceutical Industry Market Research Reports (Confidential data sources not publicly attributable). (Undated). Global Cardiovascular Drug Market Analysis.

[4] European Medicines Agency. (n.d.). Human Medicines. Retrieved from [EMA Website] (General information about drug approvals and pharmacopeias in Europe)

[5] United States Pharmacopeia. (n.d.). Pharmacopeial Information. Retrieved from [USP Website] (Information on pharmacopeial standards)