Last updated: June 5, 2026

Methylprednisolone Acetate Market Dynamics and Financial Trajectory (2024–2034): Sales Drivers, Patent/Exclusivity Pressure, and Forecast Scenarios

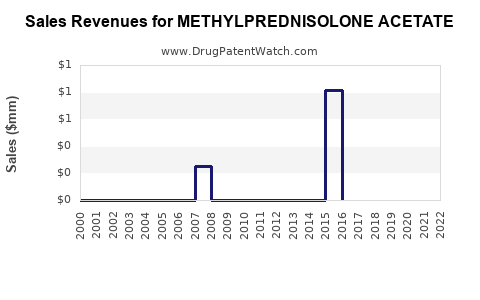

Methylprednisolone acetate is an off-patent, commodity-like corticosteroid injectable sold in multiple jurisdictions and dosage strengths, with demand driven by chronic inflammatory and autoimmune indications, hospital outpatient usage, and payer reimbursement dynamics. The financial trajectory is shaped less by brand-cycle mechanics and more by (1) substitution risk from multisource generics, (2) supply stability and manufacturing capacity constraints for sterile injectables, (3) tender and hospital formulary behavior, and (4) legal/regulatory outcomes affecting specific manufacturers’ lots or labeling. Net pricing pressure is structurally high; volume resilience typically depends on storage/handling fit, needle-use profile, and contracting terms rather than on differentiated clinical innovation.

Is methylprednisolone acetate still a brand or is it generic-dominated?

Answer: Generic-dominated. Methylprednisolone acetate injection is widely available as multisource generic product in the US and other major markets, with “brand” share typically concentrated in a small number of legacy labels or niche distributors, if any.

What dosage forms and strengths drive demand

Methylprednisolone acetate is typically commercialized as:

- Injection (sterile aqueous suspension) in multiple strengths (commonly 20 mg/mL and 40 mg/mL in various markets).

- Used across settings: hospital inpatient, ambulatory infusion centers, outpatient specialty clinics, and sometimes procedural settings for local or systemic steroid use.

Why corticosteroid injectables behave like formularies, not innovation

Injectable corticosteroids are standard-of-care therapies with:

- Short prescribing windows

- Broad clinical familiarity

- High likelihood of therapeutic interchange within the same active ingredient

- Strong payer governance of WAC/AWP-driven procurement

This structure yields low product differentiation and fast diffusion to low-cost alternatives.

What market dynamics affect pricing for injectable methylprednisolone acetate?

Answer: Pricing pressure is dominated by procurement contracting, wholesale inventory cycles, and supply availability for sterile injectables.

Core dynamics

-

Multisource competition

- Multiple manufacturers reduce pricing power.

- Loss of any one supplier can temporarily raise prices, but that effect is usually transient.

-

Tender-based purchasing

- Hospitals and government systems often award contracts to the lowest “all-in” price.

- Clinical selection tends to focus on availability and handling rather than premium formulation claims.

-

Sterile manufacturing capacity constraints

- Sterile injectables are sensitive to production outages, aseptic line constraints, and regulatory inspections.

- Temporary shortages can create “price spikes,” but demand is typically rationed and later rebounds to baseline.

-

Reimbursement and budget controls

- In many systems, corticosteroids are categorized as low-cost generics, limiting upside.

- Private payer formularies can still push down net pricing through rebates.

Financial implication

- Gross margin is volume-dependent but pricing is structurally constrained.

- Revenue can hold up if supply is stable and hospital use remains constant, but growth typically relies on contract capture or geographic expansion, not on price increases.

How does demand vary across indications for methylprednisolone acetate?

Answer: Demand is spread across inflammatory and autoimmune use cases, but the mix is stable and varies by healthcare system practice patterns.

Indication mix (typical drivers)

Common use categories include:

- Rheumatologic inflammatory diseases (flares where steroid is part of acute management)

- Dermatologic inflammatory conditions (systemic or bridging therapy where injectable steroid is used)

- Respiratory inflammatory exacerbations

- Adrenal insufficiency replacement strategies in select settings

- Allergic and inflammatory reactions in protocols that include parenteral corticosteroids

What changes the demand profile

- Guideline updates can shift preference toward other steroids or routes, but the active ingredient remains entrenched.

- Increased use of outpatient management can raise demand for rapid-access injection supply.

- Shorter flare-duration protocols can reduce total units, but generics make switching easy.

When does methylprednisolone acetate lose exclusivity and why does that matter financially?

Answer: It is effectively already in the post-exclusivity regime. Financial impact comes from ongoing generic competition, not from a single remaining expiration date.

Exclusivity framing

For a mature active ingredient like methylprednisolone acetate, exclusivity risk is typically:

- Long since expired for primary active-ingredient patents (if any existed historically).

- Still subject to product-specific intellectual property such as formulation or manufacturing-process patents, which are often narrow and may not constrain broad generics.

Why “exclusivity timeline” still matters

Even in off-patent markets, some labels can remain protected by:

- Process IP that affects manufacturing changes

- Specific presentation IP (for example, certain package configurations or rare strengths)

- Patent settlements involving particular manufacturers

Those effects can temporarily influence market shares and pricing for specific SKUs.

What is the Orange Book status of methylprednisolone acetate in the US?

Answer: The US market is expected to show broad generic availability; originator-style exclusivity is not a dominant factor for strategy because multiple ANDA products typically exist.

Practical interpretation for business planning

- Revenue forecasts should use a multisource unit demand model with scenario-based price erosion rather than single-product exclusivity curves.

- Patent analytics should focus on any remaining listed patents tied to specific NDCs rather than on active-ingredient ownership.

Which patents protect methylprednisolone acetate products and how strong are they?

Answer: If any patents remain, they are usually narrow product/process protections rather than broad method-of-use blocks.

Where remaining IP tends to exist

- Manufacturing method claims for sterile suspension characteristics

- Particle size distribution or stability-related formulation parameters

- Packaging and reconstitution guidance (rare for corticosteroid suspensions but possible for specific label claims)

How strong is the estate in practice

Given the commodity nature and wide generic availability, the typical outcome is:

- Limited ability to sustain premium pricing

- Likely focus on avoiding “design-around” rather than licensing broad market exclusion

What Paragraph IV challenges are relevant for methylprednisolone acetate?

Answer: Market-level effects exist, but Paragraph IV is usually not a major strategic event for commodity corticosteroids relative to branded high-revenue drugs.

Business impact if litigation occurs

When it occurs, it mostly affects:

- Specific manufacturers’ ability to launch early

- Short-term market share movements for certain strengths/NDCs

- Temporary price swings due to supply substitution

Financial trajectory then becomes event-driven (court outcome dates, FDA approval dates, settlements) rather than product-line innovation.

What generic entry risks exist for methylprednisolone acetate?

Answer: Entry risk is high for new competitors because market access barriers are mostly regulatory and manufacturing rather than IP.

Main barriers

- Sterility and aseptic processing compliance

- Stability and suspension equivalence

- Batch-to-batch consistency

- Inspection outcomes and quality system performance

Economic result

- New entrants compete on price quickly after approvals.

- Incumbents defend share primarily through contracts and reliable supply rather than through exclusivity.

How does methylprednisolone acetate compare with competing corticosteroid injectables financially?

Answer: It competes as part of a corticosteroid “class” procurement basket, typically anchored by unit price, availability, and label fit.

Competitive substitute dynamics

Key substitution channels:

- Other injectable corticosteroid suspensions/solutions (different active ingredients)

- Oral steroid bridging in some indications

- Long-acting steroid protocols replacing injections in certain care pathways

Financial implication

- Even if methylprednisolone acetate performs well on volume, ASP volatility is driven by the lowest-cost competitor winning tenders.

- If a competing product experiences supply disruption, methylprednisolone acetate can temporarily gain share.

How do FDA regulatory events and manufacturing quality affect revenue?

Answer: For sterile injectables, FDA events and quality issues can create abrupt revenue and supply disruptions that persist until remediation.

Event types that matter

- Form 483 observations

- Warning letters tied to sterile manufacturing controls

- Recall events

- Cessation or limitations of production pending CAPA completion

- Labeling updates that impact contracting or switching

Financial mechanism

- Revenue can drop sharply if supply is constrained.

- If remediated and reinstated, share may not fully return because procurement contracts rotate among suppliers.

What sales and financial trajectory is most plausible for methylprednisolone acetate? (Scenario framework)

Answer: A mature, price-down trajectory with stable-to-slow volume growth where supply stability and tender wins determine share.

Scenario 1: Base case (stable supply, continued price erosion)

- Units stable or slightly growing through replacement demand and protocol inertia.

- Net pricing continues to fall due to competitive contracting.

- Revenue growth is modest, with margin compression.

Scenario 2: Upside (temporary shortage or contract capture)

- Short-term price increase occurs when a supplier exits or production is constrained.

- Incumbents can increase market share during the disruption.

- Revenue outperformance lasts until supply normalizes and procurement resets.

Scenario 3: Downside (quality event or recall in major SKU)

- Revenue declines through supply interruption and loss of contract standing.

- Reputational procurement effects delay recovery.

- Competitors expand share and may remain preferred after reinstatement.

Where do the highest-margin opportunities typically sit for companies selling methylprednisolone acetate?

Answer: Margin is most affected by:

- Contract structure (bundled tenders)

- Supply reliability

- SKU coverage (multiple strengths and package sizes)

- Geography-specific procurement economics

Commercial levers

- Locking multi-year supply agreements with wholesalers and IDNs

- Optimizing sterile manufacturing throughput to reduce unit costs

- Using diversified NDC portfolios to avoid single-line disruption risk

- Managing inventory to minimize lost sales during batch release delays

How does manufacturing strategy influence financial trajectory?

Answer: For sterile suspensions, capacity and compliance drive both cost and continuity.

Key operational economics

- Cost of goods is driven by aseptic line utilization, batch yields, and rework/scrap.

- Working capital depends on raw material lead times and long batch release timelines.

- Compliance costs rise after inspections, affecting margins until throughput normalizes.

Key Takeaways

- Methylprednisolone acetate is a generic-dominated injectable with pricing shaped by tender procurement and multisource competition.

- The financial trajectory is primarily supply-and-contract driven rather than exclusivity-driven, with structural margin compression.

- Upside is typically short-cycle and linked to supplier disruptions; downside is event-driven via quality or recall risks.

- Strategy should prioritize SKU coverage, manufacturing reliability, and contract capture to stabilize volume and defend share despite continuing ASP erosion.

FAQs

1. What factors most affect net pricing for injectable corticosteroids like methylprednisolone acetate?

Tender contracts, multisource competition, and supply availability for sterile manufacturing lines.

2. How quickly do market shares shift among generic suppliers of methylprednisolone acetate?

Often within procurement cycles (weeks to months), accelerating during shortages.

3. What are the most common regulatory risks for sterile injectable generics?

Aseptic processing controls, sterility assurance system performance, and batch release documentation integrity.

4. Are there meaningful formulation differences among generic methylprednisolone acetate suspensions?

Differences are usually constrained to meet equivalence requirements; clinically relevant differentiation is limited in most settings.

5. Does litigation materially change revenue prospects for methylprednisolone acetate?

It can affect specific NDC launches, but the commodity structure limits sustained financial impact compared with high-revenue branded products.

References

- FDA. Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations. US Food and Drug Administration.

- FDA. Drug Quality and Manufacturing (inspections, recalls, enforcement actions). US Food and Drug Administration.

- FDA. ANDA approval and requirements for generic drug products (sterile injectables and quality standards). US Food and Drug Administration.