Last updated: April 24, 2026

What drove finasteride’s global market growth across time?

Finasteride is a synthetic 4-aza-steroid that blocks the conversion of testosterone to dihydrotestosterone (DHT) via 5-alpha-reductase inhibition. Commercially, its demand is dominated by two patient use cases: benign prostatic hyperplasia (BPH) and androgenetic alopecia (AGA, male pattern hair loss). The market structure has been shaped by (1) long product lifecycles, (2) patent-to-generic transitions, and (3) pricing pressure that shifts value from branded originators to multiples of lower-cost entrants.

Core demand engines

- BPH (5 mg): Chronic, long-duration therapy. Refill cycles and persistence drive steady volumes in mature markets.

- AGA (1 mg): Higher consumer participation and churn compared with BPH, but sustained demand supports a large retail footprint.

- Prescriber familiarity and switching: Finasteride has strong therapeutic familiarity among urologists and dermatologists, which lowers friction for formulary adoption and generic switching.

Market expansion and saturation pattern

- Early growth was driven by branded penetration and evidence generation in large trials.

- Mid-cycle growth increasingly came from expanded geographic access, distribution depth, and conversion of new patients into maintenance therapy rather than step-change product differentiation.

- Late-cycle growth shifted toward volume stability at lower net prices after generic entry.

Patent and generic inflection (structural driver)

Finasteride’s revenue trajectory has followed a classic sequence:

- Branded dominance while exclusivity protects pricing.

- Stepwise erosion after generic approvals and formulary adoption.

- Late-stage stabilization as multiple generics compete and pricing becomes commodity-like.

How have formulation, dosing, and indications shaped commercialization?

Finasteride is sold as two standard dosing strengths, mapped to two main indications:

- 1 mg tablets for male pattern hair loss (AGA).

- 5 mg tablets for BPH.

This dual-strength model creates two separate commercial “lanes” with different buying behaviors:

- Retail/consumer-facing dynamics dominate the 1 mg channel (telehealth and pharmacy retail distribution often matter more).

- Clinic- and urology-led dynamics dominate the 5 mg channel (formularies, payer coverage, and continuity of care matter more).

Competitive implications

- Generic competition is most intense where dispensing is routine and interchangeability is simple.

- Payer and formulary dynamics generally enforce lower net pricing after generic conversion, while patient adherence and symptom stabilization determine volume resilience.

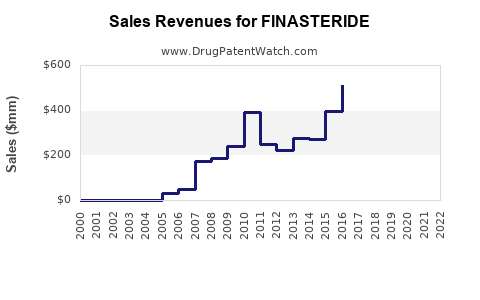

What does the financial trajectory look like after exclusivity?

Finasteride’s financial trajectory is best understood as a multi-stage curve:

- Revenue rises under brand pricing power.

- Revenue growth slows as competitive awareness and switching rise.

- Revenue falls in nominal terms after generic entry.

- Cash flow stabilizes as the drug becomes a high-volume, low-margin product with large manufacturing scale.

Typical post-generic shape for this molecule

While exact revenue per company varies by geography and by whether the manufacturer is the originator or a generic supplier, the sector pattern for finasteride is:

- Volume remains resilient due to established therapeutic use.

- Net price per unit declines sharply at first, then flattens as competitors converge on similar pricing.

- Margins compress and then stabilize at low levels for high-capacity manufacturers.

Where is the market concentrated and how does that affect pricing?

Finasteride demand concentrates where:

- BPH and AGA prevalence aligns with aging demographics.

- Pharmacy coverage and reimbursement access is broad.

- Generic substitution rates are high.

Pricing pressure mechanics

- Wholesale acquisition cost and pharmacy reimbursement generally decline post-generic conversion.

- Net pricing becomes more sensitive to:

- tender cycles and pharmacy benefit manager contracts,

- regional substitution rates,

- manufacturer-specific supply capacity and product availability.

How do current product and regulatory realities influence economics?

Finasteride is marketed as an oral solid, and it is widely available as generics in major markets. That regulatory reality drives:

- Interchangeability that speeds switching.

- Lower promotional intensity compared with differentiated branded products.

- Manufacturing focus and cost optimization as key economic levers.

Regulatory timeline anchor (originator context)

Merck introduced finasteride commercially as Proscar (5 mg) and later Propecia (1 mg). The originator and later generic market development reflect the standard pattern of exclusivity followed by generic saturation. The molecule’s core mechanism and dose/indication mapping remain stable as generics entered.

What financial outcomes do investors and R&D stakeholders typically target?

For stakeholders, finasteride offers a value case that differs from novel therapeutics:

- Investment thesis style: scale manufacturing, supply chain reliability, and contract procurement are typically more decisive than late-stage clinical differentiation.

- R&D focus: new formulations, combination therapies, adherence improvements, or life-cycle management (where patent position allows) rather than new mechanism discovery, since the core mechanism is well established.

How strong is the long-term demand durability?

Finasteride’s long-term demand durability is supported by:

- chronicity in BPH,

- long therapy continuation in a subset of patients,

- ongoing AGA incidence in aging male populations,

- established clinical guidelines and prescriber routines.

Economic durability comes less from price and more from:

- maintaining supply to avoid stock-outs,

- sustaining contract pricing and rebate structures,

- running efficient manufacturing networks.

What are the main risks to the financial trajectory?

Even for a mature medicine, financial outcomes can diverge due to:

- Generic price compression

- Continuous competition can drive pricing to levels that limit profitability for smaller manufacturers.

- Supply chain and manufacturing disruptions

- Oral solid manufacturing is scale-driven; capacity bottlenecks can temporarily lift prices but create downstream volume loss if availability drops.

- Utilization shifts

- Changes in prescribing preferences, patient selection, and alternative therapies can reduce share even if total category demand stays stable.

- Regulatory and labeling changes

- Safety communications and label updates can influence prescribing and adherence patterns.

Market sizing signals and commercial benchmarks (directional)

Public market sizing estimates for finasteride vary by methodology (brand vs generic, inclusion of combination products, and geography). The practical benchmark for business decisions is less about a single market size number and more about consistent signals:

- High-volume availability in major pharmacies.

- Multiple generic suppliers with strong substitution behavior.

- Low unit pricing relative to branded era with stabilization after repeated generic entry.

Competitor and substitution landscape: what matters most?

Finasteride markets behave like a commoditized oral therapy:

- Product differentiation is minimal.

- Competition is typically on price, supply reliability, and contract terms.

- Brand remnants still exist where originator products retain inertia or payer positioning, but generic penetration tends to dominate after exclusivity.

How should stakeholders interpret profitability and cash flow?

Finasteride typically produces:

- steady but constrained profitability at scale,

- cash-flow stability due to repeat dispensing,

- less upside from incremental clinical value and more upside from operational and commercial execution.

For originators, the financial trajectory often resembles:

- decline after generic entry,

- partial recovery only through brand persistence, bundle leverage, or geographic-specific arrangements.

For generics, the trajectory is often:

- entry at attractive initial margins,

- margin compression after additional competitors arrive,

- profitability re-stabilization for the lowest-cost producers with consistent supply.

Key Takeaways

- Finasteride’s market is structurally driven by two stable indications (BPH and AGA) mapped to 5 mg and 1 mg dosing, supporting durable utilization.

- The financial trajectory follows a brand-to-generic lifecycle: strong pricing power early, then steep nominal revenue erosion after generic penetration, with later volume-led stabilization.

- Economics post-exclusivity depend on contracting, substitution rates, tender dynamics, and manufacturing scale, not clinical differentiation.

- The main financial risks are generic price compression, supply disruptions, and utilization shifts within BPH/AGA treatment patterns.

FAQs

-

What are finasteride’s primary commercial indications?

Benign prostatic hyperplasia (BPH) using 5 mg and androgenetic alopecia (AGA) using 1 mg.

-

Why does generic entry have such a large financial impact on finasteride?

Oral solid interchangeability and established clinical routine enable rapid substitution, driving net price compression.

-

Does finasteride maintain volume even after exclusivity?

Yes, demand tends to remain resilient because treatment is long-duration in BPH and ongoing in AGA, though category share can shift with alternatives.

-

What drives profitability for finasteride suppliers after generic conversion?

Unit cost position, manufacturing reliability, contract pricing, and rebate/tender execution determine margins more than marketing.

-

What are the biggest threats to continued earnings stability?

Persistent price erosion from additional competitors, manufacturing or supply interruptions, and prescribing changes due to safety communications or treatment alternatives.

References

[1] U.S. Food and Drug Administration. (n.d.). Proscar (finasteride) prescribing information. FDA. https://www.accessdata.fda.gov

[2] U.S. Food and Drug Administration. (n.d.). Propecia (finasteride) prescribing information. FDA. https://www.accessdata.fda.gov

[3] National Library of Medicine. (n.d.). Finasteride: Drug information. PubChem. https://pubchem.ncbi.nlm.nih.gov

[4] European Medicines Agency. (n.d.). Finasteride product information and assessment history. EMA. https://www.ema.europa.eu