Last updated: April 24, 2026

What drives the ezetimibe market today?

Ezetimibe is an oral lipid-lowering drug used primarily for cholesterol management, most commonly in combination with statins and other lipid agents. The commercial market structure is shaped by (1) statin-anchored lipid therapy, (2) entrenched payer formularies and guideline adoption, (3) generic entry and price compression, and (4) manufacturer mix across geographies.

Key demand drivers

- Chronic condition, ongoing therapy: Indication use is tied to long-term cardiovascular risk management rather than episodic treatment.

- Combination regimens with statins: Ezetimibe’s standard market position is add-on therapy when statin response is insufficient or not tolerated, supporting sustained demand even as monotherapy use fluctuates.

- Guideline alignment: Clinical guidelines support ezetimibe use in specific risk strata and treatment intensification pathways, supporting continued payer coverage.

- Evolving lipid management pathways: Growth in cardiovascular prevention programs supports volume stability, while incremental penetration depends on payer step edits and competing non-statin classes.

Key supply and pricing drivers

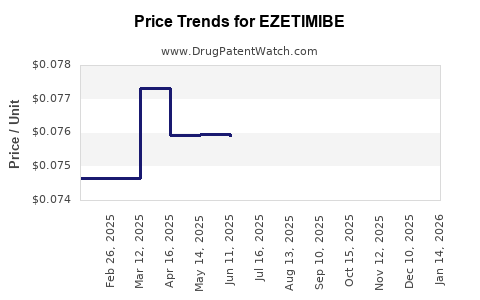

- Generic-led price compression: Once oral small-molecule generics enter, net pricing typically declines quickly, shifting the revenue model toward volume scale and low-cost procurement.

- Formulation and brand portfolio turnover: Brand-only revenue is capped by generic availability; manufacturers must rely on geography, contractual pricing, and mix-shifts to sustain value.

- Competitive class pressure: Ezetimibe competes indirectly with newer lipid agents (e.g., PCSK9 inhibitors, bempedoic acid in certain markets) where payers steer high-risk patients toward higher-cost pathways.

How is the product positioned versus alternatives?

Ezetimibe sits in the non-statin ecosystem as a lower-cost add-on that can be used broadly at earlier points in the lipid-risk management pathway compared with high-cost injectable therapies.

Competitive set (commercial lens)

- Statins: Typically first-line; ezetimibe captures “insufficient response” and intolerance-driven step-up segments.

- Other non-statin oral agents: Competes for formulary placement based on incremental LDL-C reduction, tolerability profile, and payer cost-effectiveness.

- Injectables (e.g., PCSK9 inhibitors): Higher-priced and used in narrower, high-risk segments; they can reduce incremental demand growth for ezetimibe in those segments when payers restrict access.

What does the financial trajectory look like across a typical lifecycle?

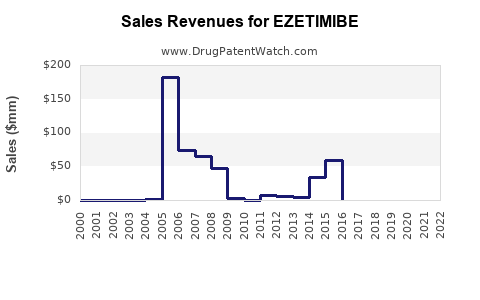

Ezetimibe’s financial trajectory is dominated by the transition from brand-led penetration to generic-led volume and pricing normalization.

Lifecycle pattern for ezetimibe economics

- Early growth / brand scaling

- Establishes guideline use and payer acceptance.

- Revenue is supported by branded pricing and protected market access in early years.

- Patent expiry and generic entry

- Net prices decline as branded share is replaced by generics.

- Revenue becomes volume-driven and tends to flatten or contract in nominal terms.

- Mature generic market

- Market growth mainly follows underlying cardiovascular patient pool and adherence.

- Value growth depends on brand persistence in certain geographies, distribution concentration, and payer mix.

Where does ezetimibe revenue concentrate geographically?

Ezetimibe revenue is generally shaped by generic adoption timelines and payer formulary behavior across major markets. In mature categories, revenue tends to concentrate where generic availability is broad and where reimbursement is stable.

Market concentration logic

- US: Large generic participation tends to compress unit economics, but high volume supports continued category revenue.

- EU5 (France, Germany, Italy, Spain, UK): Formularies and generic penetration shape price declines; prescribing patterns influence relative stability.

- Japan and other developed markets: Longer brand persistence in some cases can extend nominal revenues, but generic normalization still dominates long-run trend.

What has happened to competition and pricing after generic entry?

In mature oral small-molecule markets, generic penetration usually results in:

- Rapid decline in branded unit prices

- Shift to multi-source generic bidding

- Increased role for distribution scale and contract manufacturing economics

- Ongoing promotional pressure in remaining brand pockets

Ezetimibe follows that standard pattern because the asset is a small-molecule with broad therapeutic interchange and mature regulatory status.

How do payers typically influence utilization and net sales?

Payer controls influence utilization via:

- Step edits (statin first; ezetimibe add-on where criteria met)

- Prior authorization triggers for non-statin add-ons when criteria require documented LDL-C levels or statin intolerance

- Formulary tiering that determines out-of-pocket friction and adherence

In practice, net sales performance correlates with how easily patients pass payer criteria and how often clinicians intensify therapy without switching to alternate classes.

What is the likely medium-term financial outlook?

The medium-term trajectory is driven by two opposing forces:

- Volume stability: Patient pool for chronic lipid management supports baseline demand.

- Continued net price pressure: Generic competition and ongoing tender-driven pricing keep value growth constrained.

As newer lipid agents gain access in high-risk segments, ezetimibe’s incremental growth depends on payer willingness to sustain ezetimibe as an add-on rather than forcing escalation to higher-cost alternatives early.

Market and financial trajectory summary (business view)

Trajectory by stage

| Lifecycle stage |

Dominant revenue driver |

Typical market behavior |

Financial profile |

| Brand scaling |

Differentiated access and premium pricing |

Rapid uptake with payer adoption |

Faster nominal growth |

| Generic transition |

Price compression and share migration |

Generic-driven unit decline |

Nominal revenue flattening |

| Mature generic market |

Volume and contracting |

Tender-driven pricing stability |

Low single-digit nominal growth or contraction |

What to watch for

- Formulary status changes in major markets (tier movement, PA tightening)

- Generic tender dynamics affecting net prices

- Relative class access for PCSK9 inhibitors and other non-statin agents

- Patent and exclusivity events for brand or combination formats in specific geographies

Key Takeaways

- Ezetimibe market demand is anchored to chronic cardiovascular prevention and statin add-on use, with payer step edits shaping utilization.

- Financial performance follows a classic small-molecule lifecycle: branded scaling then generic-led price compression, shifting the model toward volume and contractual pricing.

- Medium-term growth is constrained by multi-source competition, while upside depends on payer persistence in ezetimibe add-on pathways and mix stability across geographies.

- Competitive substitution risk is real as payers steer higher-risk patients toward higher-efficacy, higher-cost lipid agents.

FAQs

-

What is ezetimibe’s main commercial use case?

It is used as an oral lipid-lowering add-on, most often with statins, to improve LDL-C reduction in patients who need additional lowering or cannot tolerate higher statin doses.

-

What typically happens to ezetimibe pricing after generic entry?

Net pricing usually declines sharply as branded units lose share to generics, and contracts shift to lowest-cost multi-source supply.

-

Why does payer policy matter so much for ezetimibe sales?

Step edits and prior authorization determine whether clinicians can intensify therapy quickly, which directly affects patient volume and adherence.

-

Does ezetimibe face direct competition from newer lipid drugs?

Indirectly. It competes for formulary placement within non-statin pathways, but newer agents often target higher-risk segments with different access criteria.

-

What is the most likely driver of future ezetimibe revenue?

It is volume stability in chronic lipid management, tempered by ongoing generic price pressure and payer-driven substitution dynamics.

References

[1] FDA. “Zetia (ezetimibe).” FDA Prescribing Information. U.S. Food and Drug Administration. https://www.accessdata.fda.gov/ (accessed 2026-04-24).

[2] EMA. “Zetia: EPAR - Product Information.” European Medicines Agency. https://www.ema.europa.eu/ (accessed 2026-04-24).

[3] NICE. “Cardiovascular disease: risk assessment and management (lipid management guidance).” National Institute for Health and Care Excellence. https://www.nice.org.uk/ (accessed 2026-04-24).

[4] ESC/EAS. “2019 Guidelines for the management of dyslipidaemias.” European Society of Cardiology/European Atherosclerosis Society. European Heart Journal. (accessed 2026-04-24).