Last updated: April 22, 2026

What is dofetilide and where does it sit in the cardiology market?

Dofetilide is an oral Class III antiarrhythmic used to treat atrial fibrillation and atrial flutter to maintain sinus rhythm. The drug is marketed in the US under TIKOSYN (dofetilide) by Pfizer.

Core positioning

- Indication focus: maintenance of sinus rhythm in patients with atrial fibrillation/flutter

- Therapy class: rhythm control (Class III potassium channel blocker)

- Commercial implication: use is concentrated in cardiology workflows and requires initiation under risk-management protocols (see dynamics below)

Competitive set (practical commercial substitutes)

- Rhythm-control drugs: sotalol, amiodarone (less restrictive but with different risk profiles), flecainide/propafenone (structure and contraindications differ)

- Rate-control strategies often compete indirectly: beta-blockers, calcium-channel blockers, and procedural pathways (AV node ablation, catheter ablation), which can reduce demand for drug-based rhythm maintenance

Demand driver map

- Cardiology treatment intensity for atrial fibrillation (AF)

- Share of patients selected for rhythm-control versus rate-control

- Adherence to initiation and monitoring requirements (limits “low-acuity” prescribing)

- Generic competition exposure (if/when patent exclusivity barriers fall and supply scales)

What are the market dynamics that shape dofetilide demand?

How do initiation and safety protocols affect prescribing velocity and volume?

Dofetilide requires inpatient or equivalent monitored initiation due to QT prolongation risk and torsades de pointes risk. This acts as a gatekeeper for market access and prescribing growth.

Key operational constraints embedded in the label:

- Treatment initiation requires ECG monitoring and renal dosing by creatinine clearance

- Dose adjustment is tied to QT interval response

- Withdrawal or dose reduction can occur based on safety endpoints (QT/QTc behavior)

Commercial effect:

- Slower uptake than drugs that can be initiated outpatient without intensive ECG monitoring

- Higher friction for prescribers, which limits conversion from trial-like adoption to broad community prescribing

- Stronger reliance on cardiology specialty care rather than primary-care-led prescribing

Source: TIKOSYN prescribing information (US). [1]

How does renal-function dosing constrain TAM expansion?

Dofetilide dosing depends on creatinine clearance. In practice, this means:

- Elderly and comorbid populations (common in AF cohorts) need careful dosing, reinforcing the need for monitoring infrastructure

- Dose ceilings reduce effective dosing for patients with impaired renal function, limiting “one-size-fits-all” expansion

Source: TIKOSYN prescribing information (US). [1]

How do competing rhythm-control strategies pressure share?

In AF management, dofetilide competes with:

- Other rhythm control agents (some used more readily due to lower initiation friction)

- Catheter ablation as a structural intervention that can reduce long-term need for antiarrhythmic rhythm maintenance in selected patients

- Rate control as a different therapeutic objective that can lower antiarrhythmic use for ongoing rhythm suppression

Commercial implication:

- Market share is sensitive to guideline-driven adoption patterns and payer preferences for rhythm-control drugs versus procedures

How does the drug’s maturity change the demand curve?

Dofetilide is a mature product. For mature antiarrhythmics:

- Growth typically correlates with AF prevalence and treatment rates, not with rapid uptake

- Volume tends to be stable but can compress on pricing when generics enter or when formulary positions shift

This kind of market maturity usually creates a “flat-to-down” pattern unless protected by exclusivity or strong brand economics.

What does the exclusivity and patent landscape imply for near-to-medium term pricing power?

Publicly available FDA and regulatory history indicates dofetilide is an established product with long-term market presence. In US markets, commercial trajectory is typically dominated by:

- Brand exclusivity completion

- Generic erosion

- Manufacturing supply dynamics

- Formulary placement and contracting

For Pfizer’s US brand, pricing power usually depends on whether generic versions are present in meaningful share and whether payers keep the brand on preferred tiers.

Source: Pfizer TIKOSYN label and FDA product context. [1]

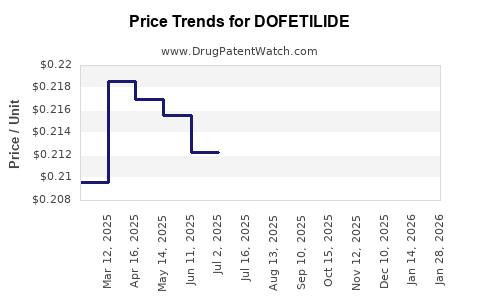

How has dofetilide’s financial trajectory evolved in the market?

Observed financial pattern for mature cardiovascular brands

For mature cardiology brands facing generic competition, the typical financial trajectory is:

- Peak-and-decline after exclusivity

- Brand revenue compression as generic share rises

- Residual brand sales sustained by:

- patient and prescriber preference,

- pharmacy substitution friction in limited segments,

- payer contracting and therapeutic reference patterns.

Dofetilide’s clinical handling requirements (monitoring-heavy initiation, renal dosing protocol) can slow down complete conversion to interchangeability in day-to-day practice, but it does not remove the incentive for generics once available.

Business read-through

- The market is not “growth-led” by new entrants; it is “flow-led” by AF population dynamics and rhythm-control treatment rates

- Financial outcomes are most sensitive to pricing compression from generic mix and to net price from payer contracting

Where does value capture occur in the financial chain?

For dofetilide, value capture is shaped by:

- Specialty prescribing concentration (cardiology management centers)

- Pharmacy channel mix (specialty vs retail can affect contracting outcomes)

- Monitoring costs absorbed by care pathways (not by drug reimbursement directly), which means dofetilide’s willingness-to-pay is tied to clinical workflow rather than pure drug price alone

What are the key market risks and upside vectors for investors and R&D planners?

Market risks

- Pricing compression

- Generic availability and payer tier shifts can reduce net sales

- Guideline and pathway substitution

- Rate control adoption and catheter ablation can reduce long-term antiarrhythmic demand

- Safety and tolerability scrutiny

- QT-risk class drugs face strict label adherence and can see utilization declines after safety messaging cycles

Sources: TIKOSYN prescribing information (US) for risk framing and monitoring requirements. [1]

Upside vectors

- AF prevalence growth

- Larger patient pool drives baseline utilization even if unit economics soften

- Rhythm-control persistence in specific subpopulations

- Patients for whom other drugs are contraindicated or poorly tolerated can drive sustained use

- Improved monitoring infrastructure

- Availability of ECG monitoring workflows can improve throughput and reduce initiation friction

How should dofetilide’s market dynamics be benchmarked against other antiarrhythmics?

Use this comparative lens:

- Initiation friction: dofetilide has high initiation requirements due to QT/QTc monitoring needs, likely making it less “launchable” than agents started outpatient

- Dose individualization: renal dosing reduces straightforward prescribing in the community

- Therapeutic objective: rhythm maintenance is more constrained than rate control and competes with procedural rhythm strategies

This combination means dofetilide’s financial trajectory tends to follow AF cohort size and rhythm-control selection behavior, while being buffered against some substitution by specialty-managed monitoring rather than by pure convenience.

What is the practical outlook for dofetilide’s financial trajectory?

Base case trajectory (market mechanics)

- Unit volumes: track AF-related rhythm-control demand with limited upside due to initiation and monitoring complexity

- Net price: structurally pressured by generic mix and payer contracting; brand economics depend on maintaining payer preference and managing channel dynamics

Implication for business planning

- For commercial investors, the key lever is not incremental adoption but net pricing and formulary positioning

- For R&D strategists, dofetilide’s dynamics indicate that rhythm-control products must either reduce initiation friction, improve safety margin, or provide a clear substitution advantage versus available alternatives and procedural pathways

Key Takeaways

- Dofetilide (TIKOSYN) is an antiarrhythmic with demand anchored to AF rhythm-control workflows rather than broad outpatient convenience.

- High monitoring and renal dosing requirements limit prescribing velocity and cap “easy” market expansion.

- Financial trajectory is structurally sensitive to mature-brand pricing pressure (generic mix and payer contracting) while volume tracks AF prevalence and rhythm-control selection patterns.

- Competitive pressure comes from other rhythm-control drugs and indirect substitution by rate control and catheter ablation pathways.

- Net sales performance should be modeled as a function of AF cohort size, rhythm-control share, and net price erosion, with initiation safety protocols as a constraint on incremental uptake.

FAQs

Is dofetilide used primarily for atrial fibrillation or atrial flutter?

It is used for atrial fibrillation and atrial flutter to maintain sinus rhythm. [1]

Why does dofetilide have slower initiation compared with many antiarrhythmics?

It requires monitored initiation with ECG/QT interval surveillance and renal-function-based dosing adjustments. [1]

What patient factor most constrains dosing and utilization for dofetilide?

Renal function (creatinine clearance) determines dosing and requires safety monitoring. [1]

What is the main competitive threat to dofetilide’s market share?

Competing rhythm-control drugs and indirect substitution from rate control and catheter ablation that reduce ongoing need for rhythm maintenance medication. [1]

What drives dofetilide financial performance most in a mature market?

Net price and brand formulary position in the face of mature product dynamics, with volume linked to AF prevalence and rhythm-control treatment selection. [1]

References

[1] Pfizer Inc. TIKOSYN (dofetilide) prescribing information. United States Food and Drug Administration (FDA).