Last updated: April 24, 2026

What drives budesonide’s market dynamics?

Budesonide is a corticosteroid used for inflammatory control across respiratory, gastrointestinal, and off-label indications. Its market behavior is shaped by (1) dose-form substitution within inhaled and intranasal segments, (2) patent and lifecycle management for key brands, and (3) reimbursement and payer pressure toward lower-cost generics and authorized biosimilars/therapeutic equivalents where applicable.

Demand profile by therapeutic area

Budesonide’s demand concentrates in three channels:

- Respiratory anti-inflammatory (notably asthma and COPD-adjacent inflammatory management via inhaled forms; and allergic rhinitis via intranasal forms).

- Otolaryngology and allergy (intranasal corticosteroid use).

- Gastroenterology (oral/enteric or rectal formulations used in inflammatory bowel disease contexts, depending on product and jurisdiction).

Competitive structure

The competitive set typically follows a “brand-to-generic ladder”:

- Established originator brands remain present where switching friction exists (formulation-specific devices, dosing equivalence perceptions, patient history, and physician preference).

- Generic entry compresses price and shifts volume to lower wholesale acquisition costs where formularies permit.

- Device competition matters for inhaled products: delivery device and formulation attributes affect payer coverage and prescriber behavior.

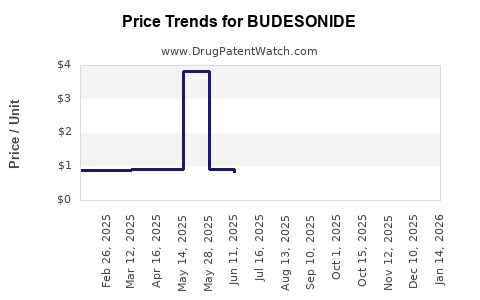

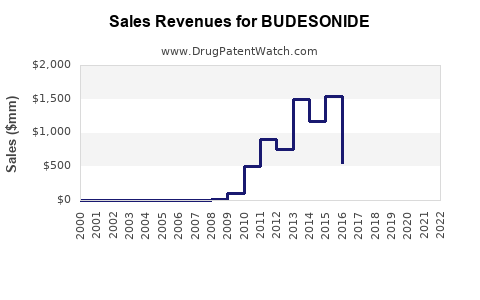

How has pricing and volume evolved since generic penetration?

Budesonide’s financial trajectory is structurally tied to generic penetration in multiple jurisdictions. Price compression tends to show up first in high-volume formulations with mature patent estates, then later in lower-volume formulations with steeper switching barriers (device and patient-specific management).

Typical market pattern for budesonide

- Early cycle: Brand pricing holds while originator exclusivity persists.

- Mid cycle: Generic launch shifts the mix toward lower-cost SKUs. Net revenue decelerates even when unit volume rises.

- Late cycle: Consolidation across wholesalers and aggressive formulary controls accelerate margin erosion.

What this means for financial trajectory

For the portfolio as a whole, budesonide’s financial curve generally shows:

- Revenue stability driven by entrenched indications and continued guideline use.

- Profit margin pressure after generic entry and tendering.

- Volume resilience relative to higher-risk specialty launches because the clinical positioning is maintenance and anti-inflammatory rather than curative.

Which formulations and product types matter most to revenue?

Market value is distributed across budesonide product formats. The revenue ranking changes by country and channel, but the general global pattern is:

- Inhaled budesonide (asthma control backbone; often the largest chronic-use segment).

- Intranasal budesonide (allergic rhinitis).

- Oral GI formulations (IBD-related use, where marketed).

- Other routes (rectal/oral liquid in some markets; typically smaller revenue share but can be important where specific indications dominate).

Route-to-cash linkage

- Inhaled and intranasal products are high-frequency repeat prescriptions. They monetize through durable demand and wide guideline acceptance, offset by fast generic substitution after entry.

- GI products often face more payer nuance and prescriber specificity, which can slow erosion in select markets versus inhaled products.

What does the financial trajectory look like for manufacturers?

Budesonide is usually owned and marketed through originator and generic competition rather than high-cost manufacturing economics. As a result, manufacturer financial performance often breaks into two regimes:

- Originator period: higher pricing and margin; moderate volume growth; strong brand share.

- Generic-led period: revenue shifts to volume and contract wins; margins shrink; some manufacturers exit low-margin SKUs.

Market-relevant financial mechanisms

- Tendering and formulary placement drive revenue more than pure demand.

- Channel inventory cycles can temporarily boost sales after launches and stocking agreements.

- Regulatory approval timing (especially for device-combination products) creates discrete commercial steps.

How do ex-U.S. and U.S. dynamics differ?

Budesonide’s global trade patterns reflect differences in:

- Patent and exclusivity timing by jurisdiction.

- Formulary access (especially for inhaled products).

- Competitive intensity and authorized generic strategies.

Practical impact on trajectory

- In markets with earlier generic authorization, budesonide tends to experience faster gross margin decline.

- In markets with more constrained switching or where branded devices persist longer, unit share may transfer more slowly, flattening revenue decline.

What patent and lifecycle factors shape the outlook?

Budesonide’s long-standing clinical use means the main drivers are lifecycle events, not breakthrough exclusivity:

- Generic expiration and entry for existing budesonide SKUs.

- Product-by-product formulation patents (salt form, device, delivery mechanism, or manufacturing process claims).

- Brand-specific device ecosystems that delay full therapeutic interchange.

Why lifecycle matters for cash flow

Even after active ingredient patents expire, line-extension strategy can preserve:

- Device-specific share.

- Higher-cost reimbursement positioning for branded formulations.

- Patient adherence through consistent delivery performance.

What are the key market metrics that determine future sales?

For budesonide specifically, the most predictive metrics are not clinical endpoints but commercial execution variables:

- Formulary inclusion and step-therapy rules for respiratory and GI indications.

- Generic penetration rates and number of competing SKUs in each country.

- Device adoption for inhaled products and patient retention effects.

- Price erosion curves driven by tender cycles and wholesaler rebate structures.

Where does growth come from in a mature molecule?

Growth does not typically come from new clinical paradigms. It comes from:

- Geographic expansion into markets with later generic entry.

- Increased utilization within guideline-defined care pathways.

- Demand stability from chronic conditions and ongoing maintenance treatment.

How do regulatory and safety issues influence commercial trajectory?

Budesonide is well-established, with regulatory focus mainly on:

- Formulation/device quality and bioequivalence for generic entries.

- Label updates and indication-specific language affecting payer policies.

- Risk communications that can influence prescriber behavior and device selection.

For mature corticosteroids, these effects are usually incremental rather than structural, but they can affect switching behavior at launch windows.

Financial trajectory summary (investment framing by phase)

The most business-relevant view is the phase-based trajectory that maps to market structure:

| Phase |

Market condition |

Revenue behavior |

Margin behavior |

Main driver |

| Brand-dominant |

Limited competition; active originator position |

Higher, steadier topline growth |

Stronger gross margin |

Brand pricing and formulary positioning |

| Generic-transition |

Generic SKUs enter; contracting intensifies |

Units may hold or rise; net sales compress |

Sharp margin compression |

Price competition and payer rebates |

| Mature-generic |

Broad generic availability |

Low growth; sensitivity to tenders |

Persistently low margins |

Contract wins, distribution leverage |

Key Takeaways

- Budesonide’s market dynamics are dominated by formulation-specific competition, generic penetration, and payer-driven contracting, not by innovation cycles.

- Its financial trajectory typically shows stable demand with margin erosion after generic entry across major respiratory and intranasal channels.

- Growth in a mature molecule is usually geographic and utilization-based, with device and formulary placement determining whether brands and select manufacturers retain share.

- Portfolio-level cash flow depends on SKU mix (inhaled vs GI), device ecosystems, and tender timing that resets pricing on a recurring basis.

FAQs

1) Why does budesonide revenue often decline after generic entry?

Generic substitution shifts purchasing to lower-priced equivalents. Even if unit volume stabilizes, net price and gross margin compress through rebate and tender structures.

2) Which budesonide formulations are most commercially durable?

Inhaled and intranasal products generally remain most durable because they align with chronic and recurring maintenance therapy, creating steady prescribing and repeat demand.

3) What most affects tender and contracting outcomes?

Therapeutic equivalence, bioequivalence outcomes, device performance considerations, and formulary mechanics such as step therapy rules and substitution policies.

4) Does lifecycle management still matter for a mature corticosteroid?

Yes. Originators can extend commercial relevance through device-specific ecosystems, formulation-level IP, and manufacturing or delivery improvements that reduce switching friction.

5) Where can manufacturers still find growth in budesonide?

Growth typically comes from markets with later generic entry, incremental increases in utilization in guideline care pathways, and winning share in contracted formularies through reliable supply and pricing discipline.

References

[1] FDA. (n.d.). Drug approvals and related information for budesonide products. U.S. Food and Drug Administration. https://www.fda.gov/drugs

[2] EMA. (n.d.). Medicines: budesonide. European Medicines Agency. https://www.ema.europa.eu/

[3] National Library of Medicine. (n.d.). Budesonide: PubChem compound summary. PubChem. https://pubchem.ncbi.nlm.nih.gov/