Budesonide - Generic Drug Details

✉ Email this page to a colleague

What are the generic sources for budesonide and what is the scope of patent protection?

Budesonide

is the generic ingredient in sixteen branded drugs marketed by Padagis Israel, Salix, Astrazeneca, Amneal Pharms, Aurobindo Pharma Usa, Barr Labs Div Teva, Dr Reddys Labs Sa, Natco, Rising, Sciecure Pharma Inc, Zydus Pharms, Padagis Us, Sun Pharm Inds Inc, Calliditas, Cheplapharm, Apotex, Kenvue Brands, Cipla, Eugia Pharma, Impax Labs Inc, Lupin, Nephron, Sandoz, Sun Pharm, Teva Pharms, Teva Pharms Usa, Takeda Pharms Usa, Actavis Labs Fl Inc, Mylan, Teva Pharms Usa Inc, and Astrazeneca Ab, and is included in thirty-seven NDAs. There are thirty-three patents protecting this compound and five Paragraph IV challenges. Additional information is available in the individual branded drug profile pages.Budesonide has one hundred and sixty-eight patent family members in thirty-four countries.

There are twenty-two drug master file entries for budesonide. Forty suppliers are listed for this compound.

Summary for budesonide

| International Patents: | 168 |

| US Patents: | 33 |

| Tradenames: | 16 |

| Applicants: | 31 |

| NDAs: | 37 |

| Drug Master File Entries: | 22 |

| Finished Product Suppliers / Packagers: | 40 |

| Raw Ingredient (Bulk) Api Vendors: | 1 |

| Clinical Trials: | 473 |

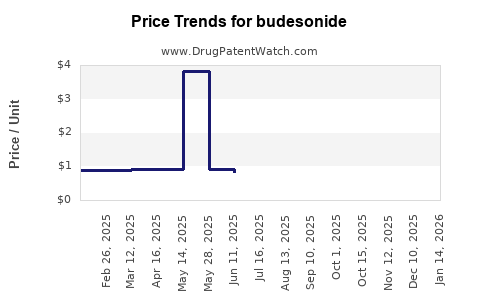

| Drug Prices: | Drug price trends for budesonide |

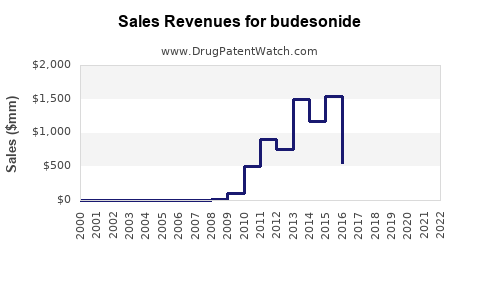

| Drug Sales Revenues: | Drug sales revenues for budesonide |

| Patent Litigation and PTAB cases: | See patent lawsuits and PTAB cases for budesonide |

| What excipients (inactive ingredients) are in budesonide? | budesonide excipients list |

| DailyMed Link: | budesonide at DailyMed |

Recent Clinical Trials for budesonide

Identify potential brand extensions & 505(b)(2) entrants

| Sponsor | Phase |

|---|---|

| Eurofarma Laboratorios S.A. | PHASE3 |

| Meriter Foundation | PHASE2 |

| University of Wisconsin, Madison | PHASE2 |

Pharmacology for budesonide

| Drug Class | Corticosteroid |

| Mechanism of Action | Corticosteroid Hormone Receptor Agonists |

Medical Subject Heading (MeSH) Categories for budesonide

Anatomical Therapeutic Chemical (ATC) Classes for budesonide

Paragraph IV (Patent) Challenges for BUDESONIDE

| Tradename | Dosage | Ingredient | Strength | NDA | ANDAs Submitted | Submissiondate |

|---|---|---|---|---|---|---|

| EOHILIA | Oral Suspension | budesonide | 2 mg/10 mL | 213976 | 1 | 2025-03-31 |

| TARPEYO | Delayed-release Capsules | budesonide | 4 mg | 215935 | 1 | 2024-12-26 |

| UCERIS | Extended-release Tablets | budesonide | 9 mg | 203634 | 1 | 2013-03-11 |

| PULMICORT RESPULES | Inhalation Suspension | budesonide | 1 mg/2 mL | 020929 | 1 | 2010-05-28 |

| ENTOCORT EC | Enteric Coated Capsules | budesonide | 3 mg | 021324 | 1 | 2008-02-01 |

| RHINOCORT ALLERGY | Nasal Spray | budesonide | 0.032 mg (32 mcg)/spray | 020746 | 1 | 2007-05-14 |

| PULMICORT RESPULES | Inhalation Suspension | budesonide | 0.25 mg/2 mL and 0.5 mg/2 mL | 020929 | 1 | 2005-09-15 |

US Patents and Regulatory Information for budesonide

| Applicant | Tradename | Generic Name | Dosage | NDA | Approval Date | TE | Type | RLD | RS | Patent No. | Patent Expiration | Product | Substance | Delist Req. | Exclusivity Expiration |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Takeda Pharms Usa | EOHILIA | budesonide | SUSPENSION;ORAL | 213976-001 | Feb 9, 2024 | RX | Yes | Yes | ⤷ Start Trial | ⤷ Start Trial | ⤷ Start Trial | ||||

| Impax Labs Inc | BUDESONIDE | budesonide | SUSPENSION;INHALATION | 078404-001 | Jul 31, 2012 | AN | RX | No | No | ⤷ Start Trial | ⤷ Start Trial | ⤷ Start Trial | |||

| Sun Pharm Inds Inc | ORTIKOS | budesonide | CAPSULE, DELAYED RELEASE;ORAL | 211929-002 | Jun 13, 2019 | DISCN | Yes | No | ⤷ Start Trial | ⤷ Start Trial | Y | ⤷ Start Trial | |||

| Astrazeneca | SYMBICORT AEROSPHERE | budesonide; formoterol fumarate | AEROSOL, METERED;INHALATION | 216579-001 | Apr 28, 2023 | RX | Yes | Yes | ⤷ Start Trial | ⤷ Start Trial | Y | ⤷ Start Trial | |||

| >Applicant | >Tradename | >Generic Name | >Dosage | >NDA | >Approval Date | >TE | >Type | >RLD | >RS | >Patent No. | >Patent Expiration | >Product | >Substance | >Delist Req. | >Exclusivity Expiration |

Expired US Patents for budesonide

| Applicant | Tradename | Generic Name | Dosage | NDA | Approval Date | Patent No. | Patent Expiration |

|---|---|---|---|---|---|---|---|

| Salix | UCERIS | budesonide | TABLET, EXTENDED RELEASE;ORAL | 203634-001 | Jan 14, 2013 | ⤷ Start Trial | ⤷ Start Trial |

| Cheplapharm | PULMICORT FLEXHALER | budesonide | POWDER, METERED;INHALATION | 021949-002 | Jul 12, 2006 | ⤷ Start Trial | ⤷ Start Trial |

| Cheplapharm | PULMICORT FLEXHALER | budesonide | POWDER, METERED;INHALATION | 021949-001 | Jul 12, 2006 | ⤷ Start Trial | ⤷ Start Trial |

| Salix | UCERIS | budesonide | TABLET, EXTENDED RELEASE;ORAL | 203634-001 | Jan 14, 2013 | ⤷ Start Trial | ⤷ Start Trial |

| >Applicant | >Tradename | >Generic Name | >Dosage | >NDA | >Approval Date | >Patent No. | >Patent Expiration |

EU/EMA Drug Approvals for budesonide

| Company | Drugname | Inn | Product Number / Indication | Status | Generic | Biosimilar | Orphan | Marketing Authorisation | Marketing Refusal |

|---|---|---|---|---|---|---|---|---|---|

| Dr. Falk Pharma GmbH | Jorveza | budesonide | EMEA/H/C/004655Jorveza is indicated for the treatment of eosinophilic esophagitis (EoE) in adults (older than 18 years of age). | Authorised | no | no | yes | 2018-01-08 | |

| Stada Arzneimittel AG | Kinpeygo | budesonide | EMEA/H/C/005653Kinpeygo is indicated for the treatment of primary immunoglobulin A (IgA) nephropathy (IgAN) in adults at risk of rapid disease progression with a urine protein-to-creatinine ratio (UPCR) ≥1.5 g/gram. | Authorised | no | no | yes | 2022-07-15 | |

| >Company | >Drugname | >Inn | >Product Number / Indication | >Status | >Generic | >Biosimilar | >Orphan | >Marketing Authorisation | >Marketing Refusal |

International Patents for budesonide

| Country | Patent Number | Title | Estimated Expiration |

|---|---|---|---|

| European Patent Office | 3346996 | ⤷ Start Trial | |

| Japan | 2018530535 | ブデゾニドの経口医薬剤形 | ⤷ Start Trial |

| World Intellectual Property Organization (WIPO) | 2017042835 | ⤷ Start Trial | |

| Australia | 2008321030 | ⤷ Start Trial | |

| >Country | >Patent Number | >Title | >Estimated Expiration |

Supplementary Protection Certificates for budesonide

| Patent Number | Supplementary Protection Certificate | SPC Country | SPC Expiration | SPC Description |

|---|---|---|---|---|

| 2435024 | 132021000000095 | Italy | ⤷ Start Trial | PRODUCT NAME: UNA COMBINAZIONE DI FORMOTEROLO (INCLUSI SUOI SALI, ESTERI, SOLVATI O ENANTIOMERI FARMACEUTICAMENTE ACCETTABILI), GLICOPIRROLATO (INCLUSI SUOI SALI, ESTERI, SOLVATI O ENANTIOMERI FARMACEUTICAMENTE ACCETTABILI) E BUDESONIDE (INCLUSI SUOI SALI, ESTERI, SOLVATI O ENANTIOMERI FARMACEUTICAMENTE ACCETTABILI)(TRIXEO AEROSPHERE); AUTHORISATION NUMBER(S) AND DATE(S): EU/1/20/1498, 20201210 |

| 2435024 | SPC/GB21/029 | United Kingdom | ⤷ Start Trial | PRODUCT NAME: A COMBINATION OF FORMOTEROL, INCLUDING PHARMACEUTICALLY ACCEPTABLE SALTS, ESTERS AND SOLVATES THEREOF, GLYCOPYRROLATE, INCLUDING PHARMACEUTICALLY ACCEPTABLE SALTS, ESTERS AND SOLVATES THEREOF, AND BUDESONIDE INCLUDING PHARMACEUTICALLY ACCEPTABLE SALTS, ES; REGISTERED: UK EU/1/20/1498 (NI) 20201210; UK PLGB 17901/0352-001 20201210 |

| 2435024 | 2190014-7 | Sweden | ⤷ Start Trial | PRODUCT NAME: A COMBINATION OF FORMOTEROL INCLUDING ANY PHARMACEUUTICALLY ACCEPTABLE SALTS, ESTERS, OR SOLVATES THEREOF, GLYCOPYRROLATE INCLUDING ANY PHARMACEUTICALLY ACCEPTABLE SALTS, ESTERS, OR SOLVATES THEREOF, AND BUDESONIDE INCLUDING ANY PHARMACEUTICALLY ACCEPTABLE SALT, ESTERS ORSOLVATES THEREOF; REG. NO/DATE: EU/1/20/1498 20201210 |

| 2435024 | 202140009 | Slovenia | ⤷ Start Trial | PRODUCT NAME: COMBINATION OF FORMOTEROL (INCLUDING ANY PHARMACEUTICALLY ACCEPTABLE SALTS, ESTERS, SOLVATES OR ENANTIOMERS THEREOF), GLYCOPYRROLATE (INCLUDING ANY PHARMACEUTICALLY ACCEPTABLE SALTS, ESTERS, SOLVATES OR ENANTIOMERS THEREOF) AND BUDESONIDE (INCLUDING ANY PHARMACEUTICALLY ACCEPTABLE SALTS, ESTERS, SOLVATES OR ENANTIOMERS THEREOF); NATIONAL AUTHORISATION NUMBER: EU/1/20/1498; DATE OF NATIONAL AUTHORISATION: 20201209; AUTHORITY FOR NATIONAL AUTHORISATION: EU |

| >Patent Number | >Supplementary Protection Certificate | >SPC Country | >SPC Expiration | >SPC Description |

BUDESONIDE: Market Dynamics and Financial Trajectory

More… ↓

Make Better Decisions: Try a trial or see plans & pricing

Drugs may be covered by multiple patents or regulatory protections. All trademarks and applicant names are the property of their respective owners or licensors. Although great care is taken in the proper and correct provision of this service, thinkBiotech LLC does not accept any responsibility for possible consequences of errors or omissions in the provided data. The data presented herein is for information purposes only. There is no warranty that the data contained herein is error free. We do not provide individual investment advice. This service is not registered with any financial regulatory agency. The information we publish is educational only and based on our opinions plus our models. By using DrugPatentWatch you acknowledge that we do not provide personalized recommendations or advice. thinkBiotech performs no independent verification of facts as provided by public sources nor are attempts made to provide legal or investing advice. Any reliance on data provided herein is done solely at the discretion of the user. Users of this service are advised to seek professional advice and independent confirmation before considering acting on any of the provided information. thinkBiotech LLC reserves the right to amend, extend or withdraw any part or all of the offered service without notice.

ISSN: 2162-2639

Privacy and Cookies

Terms & Conditions

Site Map

DrugPatentWatch Alternatives

LOE / Major Patent Expirations 2026 - 2027

NCE-1 Patent Challenge Dates 2026 - 2027

Friedman, Yali. "DrugPatentWatch" DrugPatentWatch, thinkBiotech, 2026, www.DrugPatentWatch.com.

See Primary Research Papers Citing DrugPatentWatch