Drospirenone - Generic Drug Details

✉ Email this page to a colleague

What are the generic drug sources for drospirenone and what is the scope of patent protection?

Drospirenone

is the generic ingredient in twenty-one branded drugs marketed by Exeltis Usa Inc, Mayne Pharma, Bayer Hlthcare, Novast Labs, Barr, Glenmark Pharms Ltd, Hetero Labs, Jubilant Cadista, Pharmobedient, Watson Labs, Xiromed, Sun Pharm, Aurobindo Pharma Ltd, Lupin, Apotex, Dr Reddys Labs Sa, Lupin Ltd, Naari Pte, and Watson Labs Inc, and is included in thirty-eight NDAs. There are twenty-six patents protecting this compound. Additional information is available in the individual branded drug profile pages.Drospirenone has sixty-nine patent family members in thirty-one countries.

There are eleven drug master file entries for drospirenone. One supplier is listed for this compound. There are two tentative approvals for this compound.

Summary for drospirenone

| International Patents: | 69 |

| US Patents: | 26 |

| Tradenames: | 21 |

| Applicants: | 19 |

| NDAs: | 38 |

| Drug Master File Entries: | 11 |

| Finished Product Suppliers / Packagers: | 1 |

| Raw Ingredient (Bulk) Api Vendors: | 79 |

| Clinical Trials: | 121 |

| Patent Applications: | 4,062 |

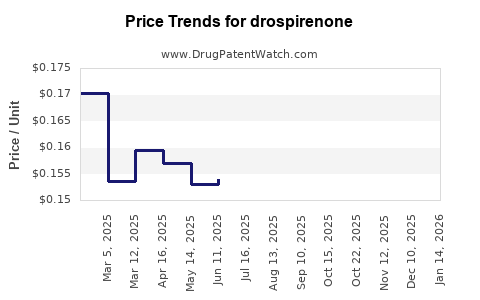

| Drug Prices: | Drug price trends for drospirenone |

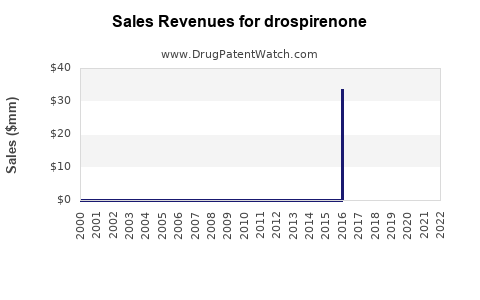

| Drug Sales Revenues: | Drug sales revenues for drospirenone |

| Patent Litigation and PTAB cases: | See patent lawsuits and PTAB cases for drospirenone |

| What excipients (inactive ingredients) are in drospirenone? | drospirenone excipients list |

| DailyMed Link: | drospirenone at DailyMed |

DrugPatentWatch® Estimated Loss of Exclusivity (LOE) Date for drospirenone

Generic Entry Dates for drospirenone*:

Constraining patent/regulatory exclusivity:

Dosage:

TABLET, CHEWABLE;ORAL |

Generic Entry Dates for drospirenone*:

Constraining patent/regulatory exclusivity:

Dosage:

TABLET;ORAL |

*The generic entry opportunity date is the latter of the last compound-claiming patent and the last regulatory exclusivity protection. Many factors can influence early or later generic entry. This date is provided as a rough estimate of generic entry potential and should not be used as an independent source.

Recent Clinical Trials for drospirenone

Identify potential brand extensions & 505(b)(2) entrants

| Sponsor | Phase |

|---|---|

| Oregon Health and Science University | PHASE4 |

| Novartis Pharmaceuticals | PHASE1 |

| Institut de Recherches Internationales Servier (I.R.I.S.) | PHASE1 |

Generic filers with tentative approvals for DROSPIRENONE

| Applicant | Application No. | Strength | Dosage Form |

| ⤷ Start Trial | ⤷ Start Trial | 4MG | TABLET;ORAL |

| ⤷ Start Trial | ⤷ Start Trial | 0.5MG;1MG | TABLET;ORAL |

The 'tentative' approval signifies that the product meets all FDA standards for marketing, and, but for the patents / regulatory protections, it would approved.

Anatomical Therapeutic Chemical (ATC) Classes for drospirenone

Paragraph IV (Patent) Challenges for DROSPIRENONE

| Tradename | Dosage | Ingredient | Strength | NDA | ANDAs Submitted | Submissiondate |

|---|---|---|---|---|---|---|

| SLYND | Tablets | drospirenone | 4 mg | 211367 | 1 | 2022-01-07 |

US Patents and Regulatory Information for drospirenone

| Applicant | Tradename | Generic Name | Dosage | NDA | Approval Date | TE | Type | RLD | RS | Patent No. | Patent Expiration | Product | Substance | Delist Req. | Exclusivity Expiration |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Xiromed | DROSPIRENONE AND ETHINYL ESTRADIOL | drospirenone; ethinyl estradiol | TABLET;ORAL-28 | 202131-001 | May 4, 2015 | AB | RX | No | No | ⤷ Start Trial | ⤷ Start Trial | ⤷ Start Trial | |||

| Watson Labs | DROSPIRENONE AND ETHINYL ESTRADIOL | drospirenone; ethinyl estradiol | TABLET;ORAL | 078833-001 | Nov 28, 2011 | AB | RX | No | No | ⤷ Start Trial | ⤷ Start Trial | ⤷ Start Trial | |||

| Exeltis Usa Inc | SLYND | drospirenone | TABLET;ORAL | 211367-001 | May 23, 2019 | RX | Yes | Yes | ⤷ Start Trial | ⤷ Start Trial | ⤷ Start Trial | ||||

| Bayer Hlthcare | BEYAZ | drospirenone; ethinyl estradiol; levomefolate calcium | TABLET;ORAL | 022532-001 | Sep 24, 2010 | AB | RX | Yes | Yes | ⤷ Start Trial | ⤷ Start Trial | Y | ⤷ Start Trial | ||

| >Applicant | >Tradename | >Generic Name | >Dosage | >NDA | >Approval Date | >TE | >Type | >RLD | >RS | >Patent No. | >Patent Expiration | >Product | >Substance | >Delist Req. | >Exclusivity Expiration |

International Patents for drospirenone

| Country | Patent Number | Title | Estimated Expiration |

|---|---|---|---|

| Argentina | 081670 | COMPOSICION FARMACEUTICA QUE COMPRENDE DROSPIRENONA Y KIT ANTICONCEPTIVO | ⤷ Start Trial |

| Australia | 2011273605 | Pharmaceutical composition comprising drospirenone and contraceptive kit | ⤷ Start Trial |

| Brazil | 112012033391 | kit contraceptivo, método contraceptivo para uma paciente do sexo feminino necessitando do mesmo e composição farmacêutica compreendendo drospirenova. | ⤷ Start Trial |

| Brazil | 122019008317 | kit contraceptivo, método contraceptivo para uma paciente do sexo feminino necessitando do mesmo e composição farmacêutica compreendendo drospirenona | ⤷ Start Trial |

| >Country | >Patent Number | >Title | >Estimated Expiration |

Supplementary Protection Certificates for drospirenone

| Patent Number | Supplementary Protection Certificate | SPC Country | SPC Expiration | SPC Description |

|---|---|---|---|---|

| 3632448 | LUC00266 | Luxembourg | ⤷ Start Trial | PRODUCT NAME: DROSPIRENONE; AUTHORISATION NUMBER AND DATE: 61678, 20210401 |

| 3632448 | 122022000040 | Germany | ⤷ Start Trial | PRODUCT NAME: DROSPIRENON; NAT. REGISTRATION NO/DATE: 7002248.00.00 20210426; FIRST REGISTRATION: DAENEMARK 61678 20191016 |

| 3701944 | 202240021 | Slovenia | ⤷ Start Trial | PRODUCT NAME: DROSPIRENONE IN COMBINATION WITH ESTETROL; NATIONAL AUTHORISATION NUMBER: EU/1/21/1547, EU/1/21/1548; DATE OF NATIONAL AUTHORISATION: 20210519; AUTHORITY FOR NATIONAL AUTHORISATION: EU |

| 2588114 | LUC00227 | Luxembourg | ⤷ Start Trial | PRODUCT NAME: DROSPIRENONE; AUTHORISATION NUMBER AND DATE: 31332 20191022 |

| >Patent Number | >Supplementary Protection Certificate | >SPC Country | >SPC Expiration | >SPC Description |

Drospirenone: Market Dynamics and Financial Trajectory

More… ↓