Last updated: May 26, 2026

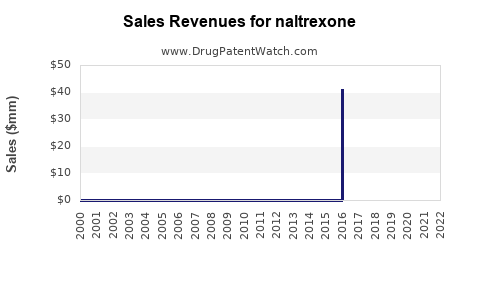

Naltrexone is a decades-old opioid-use-disorder and alcohol-use-disorder therapy with entrenched prescribing patterns, limited new entrant risk historically, and recurring generics competition concentrated in immediate-release oral dosing. The financial trajectory for the drug class is driven by (1) generic penetration in oral tablets, (2) mix shift into extended-release injectable naltrexone (XR-NTX) where patent and exclusivity dynamics matter, (3) payer coverage and prior authorization in substance-use-disorder (SUD), and (4) reimbursement volatility for office-based and clinic-administered injection delivery.

What market dynamics shape naltrexone revenue for alcohol and opioid use disorder?

Core demand drivers

- SUD prevalence and treatment access: Naltrexone competes for share within medication for opioid use disorder (MOUD) ecosystems that include buprenorphine and methadone. Uptake depends on patient eligibility for opioid-free status and clinician willingness to prescribe.

- Clinical fit: Naltrexone is used when clinicians and payers prioritize non-opioid MOUD options or when patients prefer non-dispensed opioid-substitution.

- Programmatic coverage: Outcomes-based contracting, SUD carve-outs, and Medicaid managed-care plan policies influence use rates.

Reimbursement and utilization

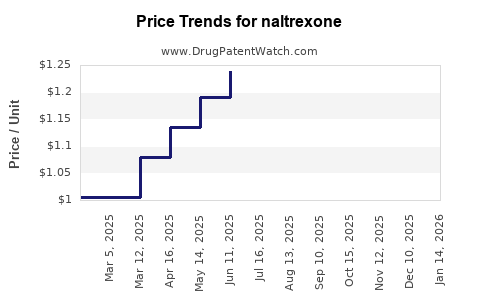

- Oral naltrexone: Typically priced at generic levels with payer resistance to premium pricing. The revenue pool is constrained by generic pricing and limited differentiation.

- Extended-release injectable (XR-NTX): Revenue is more sensitive to:

- injection administration setting (office, clinic, opioid treatment program adjacency),

- billing mechanics (drug + administration),

- prior authorization and step therapy requirements,

- payer formularies that may place XR-NTX under restricted tiers.

Competitive landscape dynamics

- For oral naltrexone, competition is primarily generic, with manufacturer rivalry focused on wholesale acquisition cost (WAC) discipline, contract pricing, and distribution coverage.

- For XR-NTX, the competitive set is smaller. Brand-originated and long-standing brand share can persist in formularies longer than oral due to administrative inertia and treatment continuity benefits.

How has naltrexone’s financial trajectory evolved amid generic entry and price erosion?

Revenue pattern by formulation

- Immediate-release oral:

- Typically experiences sustained price erosion after generic saturation.

- Company revenue contribution tends to track pharmacy benefit manager (PBM) contract pricing and volume, with fewer opportunities for premium pricing.

- XR-NTX:

- Revenue is more resilient than oral during periods when protected manufacturing processes, formulation IP, or brand-related exclusivity reduces direct price pressure.

- Once meaningful generic or biosimilar-like substitutes exist (not typical for small-molecule XR injectables, but supply and therapeutic alternative dynamics still matter), revenue generally compresses through contracting and formulary inclusion.

Material risks to financial trajectory

- MOUD preference drift: National and payer-level shifts toward buprenorphine-based models can reduce XR-NTX share even if overall MOUD utilization rises.

- SUD treatment funding cycles: Medicaid unwinds, state budget changes, and health plan redesign can change reimbursement and patient access.

- Injection administration constraints: Site-of-care transitions can interrupt continuity and reduce treated populations.

What is the patent and exclusivity framework affecting naltrexone’s commercial protection?

Key commercial implication

- Naltrexone’s market economics depend heavily on whether an administered formulation is still protected and whether payers treat it as a “must-use” option after generic oral availability.

What this means for business planning

- Oral naltrexone’s pricing pressure implies that long-term growth is not patent-driven; it is volume-driven (treatment access, clinician adoption, Medicaid participation).

- XR-NTX economics are more likely to be affected by:

- brand exclusivity timing,

- formulation and manufacturing method patents,

- regulatory exclusivity tied to specific application pathways.

(Commercial decisions in this space usually hinge on a single question: does the plan still pay for XR-NTX at contract rates that preserve margin after exclusivity windows close, or is it downgraded to cheaper alternatives.)

When does naltrexone lose exclusivity and what generic entry risks exist?

Generic entry risk reality check

- For oral naltrexone, generic entry risk is largely already realized historically; ongoing risk is less about new approvals and more about incremental erosion via contracting and substitution.

- For XR-NTX, generic entry risk exists where there are:

- supply-side barriers to production scale-up and injectable sterile manufacturing,

- bioequivalence hurdles for prolonged-release profiles,

- IP obstacles (formulation, manufacturing, and process patents).

Paragraph IV strategy vs small-molecule reality

- Paragraph IV challenges apply when a branded product still has unexpired Orange Book-listed patents. For older naltrexone, the dominant question is whether any branded XR-NTX or specialized formulations still carry unexpired listed patents that can support a 180-day exclusivity mechanism.

What is the Orange Book status of naltrexone products and how many patents cover them?

Orange Book status is product-specific (oral tablet strengths and extended-release injectables are typically treated as separate regulatory listings). A complete analysis requires product-level Orange Book extraction because listed patents can include:

- drug substance,

- drug product/formulation,

- device or delivery/administration systems,

- method of use.

Business impact

- The number and type of Orange Book listings predict whether generic competition will be immediate or delayed, and whether litigation settlements steer market entry to specific launch dates.

How do XR-NTX and oral naltrexone compare on payer coverage and access?

Payer access

- Oral: generally broadly covered once generic is established, with low copay variability and fewer restrictions.

- XR-NTX: often restricted on formulary tiers, commonly requiring prior authorization or documentation of opioid-free status and treatment plan adherence.

Clinical workflow

- Oral dosing supports flexible patient adherence but can be limited by adherence risk.

- XR-NTX shifts the adherence burden to clinic scheduling and administrative workflows. It can improve treatment persistence when the care model supports injection delivery.

Market share implications

- XR-NTX tends to hold share when:

- clinics have strong MOUD injection capacity,

- payers reimburse administration reliably,

- patient retention programs support repeat dosing.

What patent litigation affects naltrexone and downstream generic launch timing?

Where litigation matters

- Litigation has the most outsized commercial impact for XR-NTX because oral products are usually already generic and face minimal incremental delay from patent disputes.

- Litigation affects launch timing through:

- automatic stays from Hatch-Waxman filings,

- injunction outcomes,

- settlement agreements that define carve-outs by strength, dosage form, or label indications.

Settlement mechanics that change revenue

- Settlements often impose:

- launch date windows,

- required labeling modifications,

- market-entry limitations and supply commitments that delay price compression.

What FDA regulatory pathway issues drive naltrexone prescribing volume and growth?

FDA and clinical eligibility

- Naltrexone prescribing is constrained by clinical requirements, including:

- opioid-free period prior to initiation for MOUD to reduce precipitated withdrawal risk,

- patient selection criteria and monitoring protocols.

Formulation-specific regulatory considerations

- XR-NTX manufacturing consistency is critical for prolonged-release pharmacokinetics and tolerability.

- Oral naltrexone’s regulatory landscape is typically dominated by generic bioequivalence approvals, which do not materially change prescriber behavior once interchangeable and covered.

Regulatory-driven commercial effects

- Label expansions can shift addressable populations.

- Safety communications or administration guidance can alter clinician confidence and reduce utilization.

Which companies are key competitors in naltrexone (oral vs XR-NTX) and how do their strategies differ?

Oral naltrexone

- Competition centers on:

- generic contract placement,

- distribution agreements,

- PBM rebate structures,

- line extensions (strengths, packaging, and distribution format).

XR-NTX

- Competition centers on:

- formulary penetration and payer contracting,

- clinic and treatment program relationships,

- patient access programs that manage prior authorization and injection scheduling.

Market-entry posture

- Oral: mass-market pricing and contracting strategy.

- XR-NTX: managed access and continuity of care strategy.

How does naltrexone’s financial performance depend on state Medicaid and managed care?

Medicaid dynamics

- Medicaid is a major driver of MOUD utilization. Plan-level prior authorization policies and reimbursement rates for injection administration can swing XR-NTX volume.

- State-level SUD initiatives influence whether XR-NTX is used as a substitute or is deprioritized in favor of buprenorphine-based dispensing models.

Commercial payers

- Employer-based coverage often emphasizes formulary tier placement, step therapy, and adherence monitoring.

- Contracting terms can determine whether XR-NTX remains preferred for specific subpopulations.

What revenue exposure exists from biosimilar-like substitution and therapeutic competition?

Naltrexone is not a biologic, so “biosimilar” risk in the strict sense is not applicable. The relevant substitution risk is therapeutic:

- Buprenorphine: office-based induction and dispensing advantages often create durable market pressure.

- Methadone: clinic-based models can dominate for patients needing opioid agonist stabilization.

- Other MOUD adjuncts and counseling programs: payer preference for models with integrated case management can favor certain providers and modalities.

For XR-NTX, the highest substitution risk is model-driven, not product-driven.

What are the main manufacturing and IP barriers affecting cost curves?

Oral

- Manufacturing is mature; cost curves are driven by bulk APIs, sterile/non-sterile conversion, and packaging efficiency.

- The key barrier is supply chain resilience and contract pricing discipline rather than process novelty.

XR-NTX

- Injection manufacturing involves prolonged-release formulation and sterile fill-finish considerations that can raise fixed costs.

- Any IP around manufacturing process or formulation robustness can raise barriers to entry and sustain margins longer when exclusivity persists.

Key Takeaways

- Naltrexone’s financial trajectory splits sharply by formulation: oral faces persistent generic price pressure; XR-NTX carries most protection-driven and reimbursement-driven upside.

- Commercial performance is driven less by brand innovation and more by payer coverage, MOUD model adoption, and patient retention in injection-based care.

- The biggest near-term revenue swing factors are contracting dynamics for XR-NTX, state Medicaid reimbursement policies, and therapeutic competition from buprenorphine and methadone treatment models.

- Patent and Orange Book dynamics matter primarily for XR-NTX; oral naltrexone economics are largely volume and contract-price dependent after generic saturation.

FAQs

1) What drives formulary inclusion of XR-NTX versus oral naltrexone in Medicaid managed care?

Managed care decisions typically hinge on prior authorization criteria, injection administration reimbursement, and measured treatment persistence metrics.

2) What are the most common payer restrictions for naltrexone products?

Oral products usually face fewer restrictions once generic; XR-NTX commonly requires prior authorization and documentation of opioid-free eligibility.

3) How do MOUD patient retention programs affect naltrexone sales?

Injection scheduling support and adherence monitoring increase repeat-dose persistence, lifting XR-NTX utilization where payers reimburse continuity.

4) Does naltrexone compete more with buprenorphine or methadone in payer mix?

In many commercial and office-based models, it competes most directly with buprenorphine; in clinic-centric models, methadone can dominate.

5) What operational factors most impact XR-NTX profitability?

Injection administration throughput, sterile manufacturing scale, and contract pricing versus reimbursement for drug plus administration.

References (APA)

- FDA. (n.d.). Drugs@FDA. https://www.accessdata.fda.gov/scripts/cder/daf/

- FDA. (n.d.). Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations. https://www.accessdata.fda.gov/scripts/cder/ob/