Last updated: August 3, 2026

Zoloft, Pfizer’s branded sertraline hydrochloride antidepressant, generated multibillion-dollar annual sales before U.S. patent expiry in 2006. Its commercial decline was rapid after generic entry, but sertraline remained one of the largest selective serotonin reuptake inhibitor markets because of broad clinical use, low manufacturing complexity, and extensive generic substitution. Current value is concentrated in generic sertraline, overseas branded products, hospital and institutional purchasing, and differentiated formulations rather than in the original Zoloft brand.

What is Zoloft and how large is its market?

Zoloft is the U.S. brand name for sertraline hydrochloride, an SSRI approved for major depressive disorder, obsessive-compulsive disorder, panic disorder, post-traumatic stress disorder, social anxiety disorder, and premenstrual dysphoric disorder. Pfizer markets or has marketed the product through its legacy pharmaceutical business, while generic sertraline is supplied by numerous manufacturers.

| Product characteristic |

Detail |

| Active ingredient |

Sertraline hydrochloride |

| Drug class |

Selective serotonin reuptake inhibitor |

| Original U.S. sponsor |

Pfizer |

| Original U.S. approval |

1991 |

| U.S. dosage forms |

Tablets and oral concentrate historically marketed |

| Major indications |

Depression, OCD, panic disorder, PTSD, social anxiety disorder, PMDD |

| FDA reference product |

Zoloft, NDA 019839 |

| Generic status |

Widely available |

| Biosimilar relevance |

None; Zoloft is a small-molecule drug |

Sertraline competes with fluoxetine, escitalopram, citalopram, paroxetine, venlafaxine, duloxetine, and newer branded psychiatric products. Its competitive advantages are clinician familiarity, low price, broad indication coverage, and extensive generic availability. Its commercial disadvantages are the absence of meaningful molecule-level exclusivity and intense price competition.

When did Zoloft lose patent exclusivity?

Zoloft lost effective U.S. market exclusivity in 2006 when generic sertraline products entered after expiration of Pfizer’s principal compound patent and associated regulatory protection.

The principal U.S. patent historically associated with sertraline was U.S. Patent No. 4,536,518, covering sertraline compounds and pharmaceutical compositions. The patent issued in 1985 and reached its ordinary U.S. term in 2006, subject to applicable patent-term and pediatric-exclusivity calculations. FDA approval of generic sertraline followed the end of the relevant exclusivity period.

| Milestone |

Approximate timing |

Commercial effect |

| Pfizer patent filing and development period |

Early 1980s |

Established compound protection |

| U.S. Patent No. 4,536,518 issued |

1985 |

Principal composition protection |

| FDA approval of Zoloft |

1991 |

U.S. commercial launch |

| Peak branded commercialization |

Early to mid-2000s |

Annual sales reached roughly $3 billion |

| Generic entry |

2006 |

Rapid erosion of branded sales |

| Current market |

2006 onward |

Predominantly generic sertraline |

Patent expiry did not eliminate every possible form of protection. Patents covering specific formulations, salts, manufacturing methods, or later-developed delivery systems can have separate terms. Those rights did not preserve broad branded exclusivity for conventional sertraline tablets.

What patents protect Zoloft?

The historical patent estate centered on the sertraline active pharmaceutical ingredient rather than a complex delivery technology.

Composition-of-matter protection

U.S. Patent No. 4,536,518 was the critical U.S. patent for sertraline. Composition patents generally provide the strongest protection because they cover the active molecule itself across multiple formulations and indications. Once the patent expired, generic manufacturers could market conventional sertraline products subject to FDA approval.

The patent family also included international counterparts and related filings. Geographic coverage varied by jurisdiction because national patent terms, prosecution outcomes, supplementary protection rules, and launch dates differed.

Formulation patents

Zoloft was marketed primarily as conventional tablets and an oral concentrate. Conventional immediate-release dosage forms are difficult to protect commercially after active-ingredient exclusivity ends unless a later formulation provides a meaningful clinical or technical distinction.

Potential formulation protections can cover:

- Tablet composition and excipient combinations.

- Oral liquid or concentrate formulations.

- Particle size and crystallinity.

- Stability and manufacturing parameters.

- Modified-release or controlled-release delivery.

- Combination products or treatment regimens.

These rights generally have narrower infringement scope than a composition patent. Generic applicants can often design around them or pursue a Paragraph IV certification asserting that the listed patent is invalid, unenforceable, or not infringed.

What is the Orange Book status of Zoloft?

Zoloft was listed in the FDA Orange Book as the reference product for sertraline hydrochloride. The relevant commercial issue is the status of patents listed against the reference NDA and whether those patents remain enforceable or relevant to an ANDA applicant.

After generic entry, the Orange Book’s commercial significance shifted from blocking broad market access to defining the patent certifications required for later ANDAs. A generic applicant generally must certify to listed patents under one of four pathways:

- The patent information has not been submitted.

- The patent has expired.

- The applicant will launch after patent expiration.

- The patent is invalid, unenforceable, or will not be infringed.

A Paragraph IV certification can trigger patent litigation and, under the Hatch-Waxman framework, a 30-month stay of FDA approval if the brand sponsor files suit within the statutory period. Because Zoloft’s primary compound protection expired in 2006, current generic competition is not dependent on a single active molecule patent in the way it was before launch.

Which companies challenged Zoloft patents?

Generic competition came from multiple ANDA sponsors after the core exclusivity period ended. The competitive group has included major generic manufacturers such as Apotex, Ivax or Teva-related entities, Lupin, Ranbaxy, Mylan, Sandoz, and other suppliers that obtained FDA approval or entered the U.S. market over time.

The principal litigation risk in the Zoloft market was concentrated in the pre-expiry period, when generic applicants sought approval through Paragraph IV certifications. The relevant litigation questions included:

- Whether the sertraline patent claims were valid.

- Whether the generic product infringed the asserted claims.

- Whether the generic formulation used a protected polymorph, salt, or process.

- Whether the patent was enforceable after prosecution or regulatory conduct.

- Whether settlement terms delayed or permitted generic launch.

The commercial result was a broad generic market rather than a prolonged, highly concentrated exclusivity period. The absence of a durable post-expiry formulation franchise limited Pfizer’s ability to retain substantial U.S. revenue.

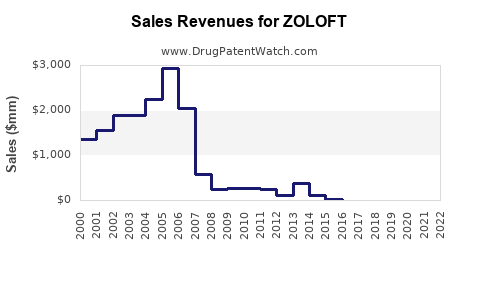

How did generic entry affect Zoloft revenue?

Zoloft followed the standard small-molecule patent-cliff pattern: strong growth before patent expiry, followed by a steep fall in branded revenue once low-cost substitutes became available.

Pfizer’s Zoloft sales were approximately $3 billion annually at their peak before generic erosion. Public company reporting indicates that sales declined sharply after 2005 and continued falling as additional generic suppliers entered and formularies substituted generic sertraline for branded Zoloft.

| Period |

Financial trajectory |

Market interpretation |

| 1990s |

Rapid uptake |

Expansion of SSRI use and indication breadth |

| 2000-2004 |

High-growth to mature blockbuster |

Broad physician adoption and recurring prescriptions |

| 2005 |

Near peak |

Patent expiry approached |

| 2006 |

Sharp decline |

Generic entry and payer substitution |

| 2007 onward |

Residual branded revenue |

Generic dominance and limited brand retention |

The exact reported revenue depends on whether a source uses worldwide product revenue, Pfizer segment reporting, or calendar-year versus fiscal-year presentation. The strategic conclusion is consistent: the brand lost most of its economic value after generic entry.

How does Zoloft compare with competing antidepressants?

Sertraline remains commercially important because it occupies a durable generic position across primary care, psychiatry, pediatrics, and hospital formularies. Its competitive position differs from branded antidepressants that rely on patent-protected delivery systems, combination products, or new mechanisms.

| Drug |

Active ingredient |

Exclusivity position |

Generic competition |

Commercial profile |

| Zoloft |

Sertraline |

Expired |

Extensive |

Low-cost, high-volume generic |

| Prozac |

Fluoxetine |

Expired |

Extensive |

Mature SSRI market |

| Lexapro |

Escitalopram |

Expired |

Extensive |

Strong historical branded franchise |

| Paxil |

Paroxetine |

Expired |

Extensive |

Mature SSRI market |

| Effexor XR |

Venlafaxine |

Expired |

Extensive |

SNRI with historical extended-release value |

| Cymbalta |

Duloxetine |

Expired |

Extensive |

SNRI with broad pain and psychiatric use |

| Trintellix |

Vortioxetine |

Later-generation exclusivity |

Limited relative to sertraline |

Branded differentiated antidepressant |

Sertraline has no biosimilar exposure because biosimilars apply to biologic products, not chemically synthesized small molecules. Its relevant substitution risk is generic, not biosimilar.

What generic entry risks exist for Zoloft?

The key generic-entry risk is already realized in the United States. Future competitive pressure will come from additional manufacturers, contract manufacturers, API suppliers, and price reductions rather than from a first generic launch.

Price erosion

Generic sertraline is a high-volume, low-margin product. Multiple approved suppliers can drive significant reductions in average selling prices. Retail prices can vary by dosage, pharmacy channel, insurance design, and manufacturer availability.

Supply-chain concentration

Although many companies can manufacture sertraline tablets, shortages can arise from API disruptions, manufacturing observations, quality recalls, or changes in supplier economics. A low-margin market can reduce the number of commercially active suppliers even when many approvals remain on record.

Formulation and dosage competition

Generic manufacturers can compete across 25 mg, 50 mg, and 100 mg tablets and other approved strengths. Oral concentrate products have a narrower commercial market and may have different manufacturing and distribution economics.

Regulatory substitution

FDA-approved generic sertraline products generally receive therapeutic-equivalence ratings that support pharmacy substitution under state law and payer policy. This accelerates conversion away from branded Zoloft.

What manufacturing and intellectual-property barriers remain?

Sertraline does not have the manufacturing complexity associated with biologics, sterile injectables, or advanced antibody-drug conjugates. The main technical barriers are process consistency, impurity control, polymorph management, tablet uniformity, dissolution performance, and regulatory compliance.

Manufacturing know-how can remain commercially valuable even after patent expiry. Companies with reliable sertraline API access, validated processes, established FDA compliance records, and strong wholesaler relationships can operate more efficiently than smaller entrants.

The remaining intellectual-property barriers are narrower than the original compound patent. They may involve:

- Process patents.

- Crystal or polymorph claims.

- Formulation patents.

- Packaging and stability systems.

- Specialized liquid or modified-release products.

- Manufacturing trade secrets.

These rights can support targeted litigation but do not recreate Zoloft’s former market-wide exclusivity.

What licensing deals affected Zoloft?

Zoloft’s commercial history was primarily an internal Pfizer product franchise rather than a modern platform asset built around extensive external licensing. Pfizer obtained the economic benefit of discovery, development, regulatory approval, and global commercialization through its predecessor and corporate operations.

The main transaction-related issue is corporate ownership. Pfizer’s legacy portfolio included products developed or acquired through predecessor companies, and Zoloft revenue was reported within Pfizer’s pharmaceutical operations. No current licensing arrangement is required for generic manufacturers to sell approved sertraline products in the United States after patent expiry.

What is the litigation status for Zoloft?

The major Zoloft patent disputes were tied to generic ANDA filings and the pre-expiry period. Current litigation risk is more likely to involve product liability, manufacturing quality, supply contracts, trademark use, or narrow formulation claims than a dispute over broad ownership of sertraline.

Trademark protection remains separate from patent protection. Generic manufacturers can sell sertraline hydrochloride under their own names but cannot market their products as Zoloft or use Pfizer’s protected branding in a manner that creates confusion.

What is Zoloft’s current commercial value?

Zoloft’s current value is primarily market-based rather than patent-based. The molecule remains clinically established, but Pfizer no longer controls the U.S. sertraline market through exclusivity.

Revenue exposure is concentrated in:

- Generic sertraline volume.

- International markets where brand penetration and local patent histories differ.

- Institutional purchasing.

- Prescriptions that remain branded because of physician preference or patient continuity.

- Specialty or liquid formulations with smaller supplier pools.

For Pfizer, the product’s strategic value is substantially lower than during its blockbuster period. For generic manufacturers, sertraline is a mature-volume opportunity with limited pricing power and modest differentiation. For investors, its economics are better analyzed through prescription volume, channel share, manufacturing cost, and supply reliability than through patent duration.

Key Takeaways

- Zoloft is Pfizer’s original brand for sertraline hydrochloride, an SSRI approved in the United States in 1991.

- Its principal U.S. composition patent, U.S. Patent No. 4,536,518, expired in 2006.

- Generic sertraline entered the U.S. market in 2006, causing a rapid decline in branded Zoloft revenue.

- Peak annual Zoloft sales were approximately $3 billion before generic erosion.

- The current market is dominated by generic manufacturers and payer-driven substitution.

- Formulation, process, polymorph, and liquid-product patents may create narrow barriers but do not restore broad molecule-level exclusivity.

- Zoloft has no biosimilar risk because sertraline is a small-molecule drug.

- The principal commercial risks are price erosion, manufacturing reliability, API supply, and further generic competition.

- Current Zoloft value is driven by brand persistence, international sales, and generic market volume rather than active U.S. patent protection.

FAQs About Zoloft Patents, Revenue, and Generic Competition

Is Zoloft still protected by a U.S. patent?

The principal U.S. sertraline composition patent expired in 2006. Narrow patents covering particular formulations or manufacturing methods may have had different terms, but they did not preserve broad exclusivity for conventional sertraline.

Who manufactures generic Zoloft?

Generic sertraline has been supplied by multiple companies, including large generic manufacturers and contract suppliers. The active supplier group can change based on FDA approvals, commercial launches, recalls, pricing, and API availability.

Can a generic manufacturer launch a product called Zoloft?

No. Generic manufacturers can sell FDA-approved sertraline hydrochloride under their own names. Zoloft is Pfizer’s brand and trademark.

Did Pfizer launch an authorized generic version of Zoloft?

Authorized-generic arrangements depend on commercial agreements and market periods. The post-2006 market included multiple generic sertraline suppliers, and branded Zoloft no longer held broad U.S. exclusivity.

Is sertraline a high-growth pharmaceutical market?

No. Sertraline is a mature, high-volume generic market. Growth is driven mainly by prescription volume, treatment prevalence, geographic expansion, and channel utilization rather than by premium pricing or patent-protected innovation.

References

-

U.S. Food and Drug Administration. (1991). Zoloft (sertraline hydrochloride) prescribing information, NDA 019839. FDA.

-

U.S. Food and Drug Administration. (2024). Approved drug products with therapeutic equivalence evaluations. FDA.

-

U.S. Patent and Trademark Office. (1985). U.S. Patent No. 4,536,518: Cis-4-phenyl-1-(dimethylamino)-1,2,3,4-tetrahydronaphthalene. USPTO.

-

Pfizer Inc. (2006). Annual report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. Pfizer.

-

U.S. Food and Drug Administration. (2024). Orange Book: Approved drug products with therapeutic equivalence evaluations. FDA.

-

U.S. Food and Drug Administration. (2024). Abbreviated new drug application approvals and patent certifications under the Hatch-Waxman Act. FDA.