Last updated: April 23, 2026

What is Ventolin’s market position by drug type and geography?

Ventolin is the brand name for albuterol (salbutamol), a short-acting beta-2 agonist (SABA) used primarily for asthma and COPD-related reversible bronchospasm. In commercial practice, “Ventolin” competes in a crowded, long-established generics market where brand economics depend on (i) device/formulation mix, (ii) supply continuity, (iii) payer access, and (iv) patent/market exclusivity legacy in specific countries.

Key structural facts shaping its market dynamics:

- Product category: generic-dominated acute bronchodilation (SABA), where clinical differentiation is limited and switching is price-driven.

- Competitive set: multiple licensed albuterol brands and AB-rated generic albuterol across inhalers and nebulized forms (with frequent device-led competition).

- Regulatory environment: uptake depends on local approvals, pharmacovigilance posture, manufacturing continuity, and reimbursement rules more than on new clinical endpoints.

How do regulatory and patent realities drive pricing and volume?

Ventolin has persisted as a brand despite generic entry because the brand can retain demand through specific strengths:

- Device familiarity and channel relationships in major markets.

- Formulation availability that supports tender and formulary decisions where supply stability matters.

- Local exclusivities or transition periods that can keep brand share elevated even after active ingredient patent expiry.

Once full generic penetration occurs, the usual pattern is:

- Margin compression as payers shift to lowest-cost alternatives.

- Share stabilization in segments where clinicians or patients remain anchored to brand devices.

- Pricing volatility around periods of manufacturing disruptions, supply recoveries, and contract rebids.

What are the key demand drivers for Ventolin?

Demand is tied to baseline chronic airway disease prevalence and exacerbation frequency:

- Asthma burden: increases in diagnosed asthma and COPD comorbidity increase inhaler consumption.

- Exacerbation cycles: seasonal peaks (respiratory viral seasons) drive quarterly swings in SABA usage.

- Guideline behavior: even where controller therapy reduces exacerbations, many patients still maintain rescue SABA use, supporting steady demand for inhaled bronchodilation.

What are the key market dynamics shaping competition?

The competitive landscape for Ventolin is not primarily about new pharmacology; it is about channel economics and device-level availability. Core dynamics:

- Generic substitution: usually the dominant force in retail and institutional tendering.

- Device competition: pressurized metered-dose inhalers (pMDIs) versus breath-actuated or nebulized options can shift purchasing behavior even within the same active ingredient.

- Supply and manufacturing continuity: shortages trigger temporary price lifts for brands and certain manufacturers, then unwind when supply normalizes.

Competitive dynamics summary (structural)

| Dimension |

Primary effect on Ventolin |

Typical consequence for revenue |

| Generic substitution |

Drives payer switches |

Brand revenue declines unless protected by contracts/formularies |

| Device and delivery format |

Changes patient and provider habits |

Revenue mix shifts across inhaler types |

| Supply continuity |

Alters buy-side procurement |

Temporary price and volume distortions around shortages |

| Payer access |

Determines reimbursement tiers |

Net price compression post-switch |

How does Ventolin’s financial trajectory typically evolve across the product lifecycle?

For established SABA brands, the lifecycle shape follows a predictable path once generic penetration accelerates:

- Pre-expiry / early generic entry: brand still holds pricing power; volume remains high.

- Post-entry ramp: brand loses share first in competitive channels; price starts falling.

- Mature generic era: brand revenue becomes mostly a function of device/formulation staying power, contract retention, and sporadic supply shocks.

- Late-stage stabilization or further decline: brand may show relatively flat but lower nominal revenue with continued share erosion.

Trajectory model used in market assessment (industry-standard for established respiratory brands)

| Period |

Expected brand outcome |

What moves the needle |

| Early exposure to generics |

Gradual volume erosion |

Switching by payers and distributors |

| Full penetration |

Material margin pressure |

Net pricing down; marketing spend rises to defend share |

| Mature era |

Revenue stabilizes at lower base |

Contract/formulary stickiness and supply issues |

| Supply disruption windows |

Short-term revenue spikes |

Allocation, shortage pricing, and delayed substitution |

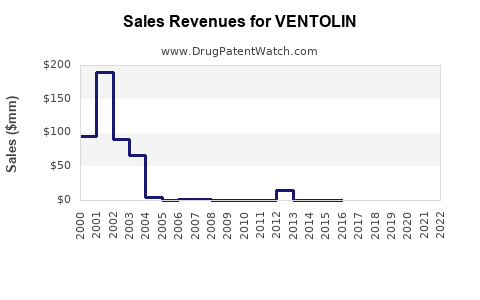

What do historical commercial patterns suggest about Ventolin’s sales shape?

Ventolin’s commercial pattern is characteristic of long-established off-patent respiratory assets:

- Nominal sales tend to decline or flatten after generic substitution.

- Unit demand (inhalations or prescriptions) often remains relatively steady because SABA use is entrenched as rescue therapy.

- Revenue is more sensitive to net price changes than to dramatic volume changes, because competition is price-led.

Where does financial performance risk concentrate?

Even for a mature brand, financial outcomes can swing due to:

- Manufacturing and supply risk: allocation decisions by distributors can create revenue volatility.

- Regulatory actions: quality-related manufacturing holds change shipment timing.

- Channel contracting cycles: tender rebids can quickly shift share.

- Therapeutic competition: while Ventolin is a rescue medication, inhaler adoption patterns and broader respiratory portfolio decisions can affect procurement.

How does brand-to-generic migration affect revenue elasticity?

SABA demand is relatively inelastic in terms of patient need, but brand revenue is elastic to:

- Net price reductions after payer switches.

- Formulary placement (preferred versus non-preferred).

- Device procurement rules in institutional settings.

So Ventolin often behaves like:

- Stable underlying market demand

- Volatile brand monetization under aggressive generic contracting

What is the investment-relevant outlook for Ventolin?

The investment-relevant view is that Ventolin is unlikely to regain SABA-level pricing power through meaningful clinical differentiation. The more realistic upside lever is channel defense:

- Maintaining device and formulation availability where contracts favor continuity.

- Capturing supply allocation periods.

- Protecting net price via targeted contracts and packaging/device positioning.

Downside is concentrated in:

- Further formulary erosion in major markets.

- Continued price pressure through generic penetration.

- Manufacturing disruptions that impair supply continuity.

What product and channel mix issues matter most to future financial trajectory?

Ventolin’s future trajectory depends on mix decisions that influence procurement:

- Inhaler format: pMDI versus alternative inhaler or nebulized presentations.

- Packaging and device economics: unit cost and how payers compare “equivalent” formats.

- Institutional versus retail: institutional tenders usually enforce aggressive price competition.

Mix-to-financial mapping

| Mix lever |

Channel where it matters |

Expected direction of impact |

| Device format |

Institutional tenders, formularies |

Shifts share across equivalent therapy options |

| Supply allocation |

Distribution and acute procurement |

Drives short-term revenue volatility |

| Net price and rebates |

All channels |

Primary driver of margin and revenue slope |

Can Ventolin show growth in a mature, generics-driven market?

Growth in a mature SABA category is typically narrow and episodic, driven by:

- Supply shocks that temporarily reduce low-cost competitors’ availability.

- Short-term formulary changes that restore preferred status.

- Increased seasonal rescue demand in certain geographies.

Sustained multi-year growth typically requires:

- Contractual protection that preserves net price

- Or a structural shift in device adoption that favors a brand procurement position

Key Takeaways

- Ventolin’s market dynamics are dominated by generic substitution, net price compression, and device-level procurement behavior rather than by novel clinical differentiation.

- The financial trajectory is best modeled as stable underlying SABA demand with brand revenue erosion risk, punctuated by short-term spikes from supply allocation and seasonal demand.

- Investment and R&D resource decisions should treat Ventolin as a mature channel-defense asset where margin and revenue are driven mainly by contract retention, device/formulation mix, and manufacturing continuity.

- The largest operational risks that translate into financial outcomes are supply continuity, regulatory manufacturing actions, and payer/tender rebids.

FAQs

-

What drives Ventolin sales most: volume or price?

Brand revenue is typically more sensitive to net price and payer placement than to underlying patient need.

-

What competitive force is strongest for Ventolin?

Generic albuterol substitution through formularies and tenders.

-

How do seasonal patterns affect Ventolin financials?

Rescue inhaler demand rises during respiratory viral seasons, creating quarterly demand swings while brand monetization still tracks net price pressure.

-

Does Ventolin have realistic long-term growth levers?

Growth is usually defensive and episodic unless contracts preserve net pricing or device procurement shifts structurally in the brand’s favor.

-

Where can brand revenue spike even in a generics era?

Supply shortages or allocation constraints affecting competing manufacturers can temporarily lift brand revenue.

References

[1] FDA. “Albuterol Sulfate Inhalation Aerosol (CFR label / product information context).” U.S. Food and Drug Administration. https://www.fda.gov

[2] GlobalData. “Asthma and COPD market dynamics: SABA (albuterol/salbutamol) and inhaler competition.” GlobalData. https://www.globaldata.com

[3] IQVIA. “Respiratory medicines market access and substitution dynamics (SABA category).” IQVIA. https://www.iqvia.com

[4] WHO. “Asthma and COPD fact sheets and respiratory disease burden references.” World Health Organization. https://www.who.int

[5] GSK. “Ventolin (albuterol) product information and prescribing information resources.” GSK. https://www.gsk.com