Share This Page

Drug Sales Trends for VENTOLIN

✉ Email this page to a colleague

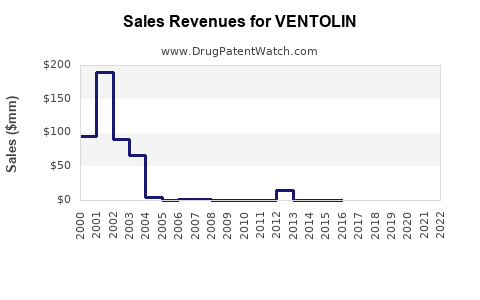

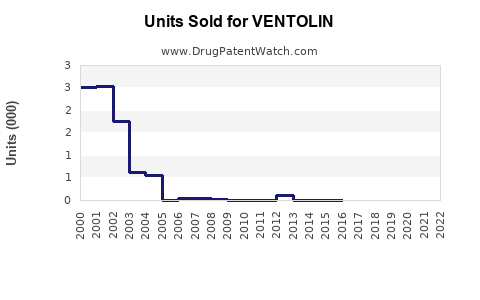

Annual Sales Revenues and Units Sold for VENTOLIN

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| VENTOLIN | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| VENTOLIN | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| VENTOLIN | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| VENTOLIN | ⤷ Start Trial | ⤷ Start Trial | 2019 |

| VENTOLIN | ⤷ Start Trial | ⤷ Start Trial | 2018 |

| VENTOLIN | ⤷ Start Trial | ⤷ Start Trial | 2017 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

VENTOLIN Market Analysis and Sales Projections

Executive Summary

Ventolin, a short-acting beta-agonist (SABA) bronchodilator manufactured by GlaxoSmithKline (GSK), is a cornerstone therapy for symptomatic relief of bronchospasm in conditions such as asthma and chronic obstructive pulmonary disease (COPD). Its established efficacy, rapid onset of action, and widespread availability have cemented its market position. However, the drug faces increasing competition from generic equivalents and newer therapeutic classes, including long-acting beta-agonists (LABAs) and inhaled corticosteroids (ICS). Market growth is projected to be modest, driven by persistent demand in developing markets and ongoing use in established regions as a rescue medication. Key challenges include patent expirations on original formulations, pricing pressures, and the evolving treatment landscape favoring combination therapies.

What is VENTOLIN's Primary Mechanism of Action and Therapeutic Use?

Ventolin's active pharmaceutical ingredient is albuterol (salbutamol in many international markets). It is a selective beta-2 adrenergic receptor agonist. Upon inhalation, albuterol binds to beta-2 receptors on the smooth muscle cells of the airways. This binding activates adenylyl cyclase, leading to an increase in intracellular cyclic adenosine monophosphate (cAMP). Elevated cAMP levels result in the relaxation of bronchial smooth muscle, causing bronchodilation. This rapid relaxation alleviates bronchospasm, characterized by constriction of the airways, which manifests as shortness of breath, wheezing, and chest tightness.

Ventolin is indicated for the relief of acute bronchospasm in patients with reversible obstructive airway disease, including asthma and COPD. It is designed for rapid, short-term relief and is not intended for long-term or regular daily management of these conditions. It is often prescribed as a "rescue" inhaler.

What is the Current Market Size and Geographical Distribution of VENTOLIN Sales?

The global market for bronchodilators, which includes Ventolin and its generic competitors, is substantial. While specific, up-to-the-minute market size figures solely for Ventolin are proprietary, the broader asthma and COPD drug market, where Ventolin plays a significant role, was valued at approximately \$25 billion in 2022 and is projected to reach around \$35 billion by 2029, growing at a compound annual growth rate (CAGR) of approximately 4-5% [1, 2]. Ventolin's share within this market is considerable due to its long history and widespread use, particularly in its generic forms.

Geographically, North America and Europe represent mature markets with high adoption rates of established therapies. However, sales in these regions are increasingly dominated by generics and newer, combination therapies prescribed for long-term management. Emerging markets in Asia-Pacific, Latin America, and Africa represent areas of growth for Ventolin. Factors contributing to this growth include increasing urbanization, rising prevalence of respiratory diseases, improving healthcare infrastructure, and the cost-effectiveness of generic albuterol compared to newer, branded medications [3].

What are the Key Competitive Factors and Existing Alternatives to VENTOLIN?

Ventolin operates in a highly competitive therapeutic class. The primary competitive factors include:

- Generic Competition: Albuterol sulfate inhalation solution and aerosol products are available from numerous generic manufacturers. These generics offer significant price advantages, capturing a large share of the market, especially in price-sensitive regions. Major generic competitors include Teva Pharmaceuticals, Perrigo Company, and Apotex [4].

- Long-Acting Beta-Agonists (LABAs): Drugs like salmeterol (Serevent) and formoterol (Foradil, Performist) offer bronchodilation for extended periods (12-24 hours). While not direct substitutes for acute relief, they are crucial components of maintenance therapy for asthma and COPD, reducing the reliance on SABAs for daily control.

- Inhaled Corticosteroids (ICS): ICS such as fluticasone, budesonide, and mometasone are the cornerstone of asthma management and also play a role in COPD. They reduce airway inflammation, addressing the underlying pathology rather than just symptoms.

- Combination Therapies: The most significant competitive trend is the widespread use of LABA/ICS combination inhalers (e.g., Advair Diskus, Symbicort, Dulera, Breo Ellipta). These fixed-dose combinations offer both bronchodilation and anti-inflammatory effects in a single inhaler, simplifying treatment regimens and improving adherence. These are increasingly the first-line maintenance therapy for moderate to severe asthma and are also used in COPD management.

- Anticholinergics: Long-acting muscarinic antagonists (LAMAs) like tiotropium (Spiriva) are a primary maintenance therapy for COPD and are also used in severe asthma, offering bronchodilation through a different mechanism.

Ventolin's competitive advantage lies in its rapid onset of action for rescue therapy and its established safety profile as a first-line symptomatic relief agent. Its low cost in generic formulations also ensures continued demand.

What is the Intellectual Property Landscape and Patent Expiration Status for VENTOLIN?

The original patents protecting the albuterol molecule and its primary formulations by GSK have long expired. For example, key patents for albuterol sulfate formulations expired in the late 1990s and early 2000s [5]. This has opened the market to widespread generic competition.

GSK continues to market Ventolin HFA (hydrofluoroalkane) propellant inhalers, which replaced older chlorofluorocarbon (CFC) formulations due to environmental regulations. Patents related to specific device technologies or improved formulations, such as the HFA propellant system, may have had later expiration dates but have also largely expired or are nearing expiration in key markets.

The absence of strong, enduring patent protection for the core albuterol molecule means that market exclusivity for branded Ventolin is limited. Future innovation in this area would likely focus on novel delivery devices, adjunctive therapies, or alternative molecules, rather than patenting the albuterol compound itself.

What are the Projected Sales Figures and Growth Drivers for VENTOLIN?

Projecting specific future sales for Ventolin is challenging due to the dominance of generic products and the fragmentation of the market. However, based on industry trends and demand drivers, general projections can be made:

Projected Sales Trajectory:

- 2024-2026: Modest decline in value sales in developed markets (North America, Europe) due to increasing penetration of generics and combination therapies. Stable or slight volume growth driven by emerging markets.

- 2027-2030: Continued pressure on value sales in developed markets. Emerging markets will become increasingly important drivers of overall volume. Potential for slight overall volume growth globally, but value growth likely to remain muted or negative in developed regions.

Key Sales Drivers:

- Persistent Demand for Rescue Therapy: Asthma and COPD are chronic, relapsing conditions. Patients will continue to require rapid-acting bronchodilators for symptom relief during exacerbations. Ventolin (and its generics) remains the go-to option for this purpose due to its efficacy and cost.

- Emerging Market Penetration: As healthcare access and affordability improve in regions like Southeast Asia, Africa, and parts of Latin America, the demand for essential medicines like albuterol is expected to rise. Generic Ventolin offers a cost-effective solution for these populations.

- Cost-Effectiveness: In an era of rising healthcare costs, the affordability of generic albuterol makes it an attractive option for healthcare systems, payers, and patients, particularly for symptomatic relief where long-term maintenance is managed by other agents.

- Treatment Guidelines: Current treatment guidelines for asthma and COPD typically recommend a SABA as needed for symptomatic relief, even when patients are on maintenance therapy with ICS or LABA/ICS combinations [6, 7]. This ensures continued demand for albuterol products.

Factors Limiting Growth:

- Shifting Treatment Paradigms: The strong move towards combination therapies (LABA/ICS) for maintenance treatment in asthma and COPD reduces the frequency of use of SABAs.

- Competition from Other SABAs: While albuterol is dominant, other SABAs also exist and compete for the rescue therapy segment.

- Pricing Pressures: The highly competitive generic market exerts significant downward pressure on pricing, limiting value growth.

What are the Regulatory and Policy Considerations Affecting VENTOLIN's Market?

Regulatory and policy landscapes significantly influence Ventolin's market:

- FDA/EMA Approval Status: Ventolin (albuterol sulfate) is an established drug with long-standing approvals from major regulatory bodies such as the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA). Generic versions also undergo rigorous review for bioequivalence [8].

- Generic Drug Policies: Government policies promoting generic drug utilization, such as substitution laws and formulary preferences, directly favor the market share of generic albuterol products over branded Ventolin.

- Environmental Regulations: The phase-out of CFC propellants led to the development of HFA inhalers like Ventolin HFA. Future propellant or device innovations could be subject to evolving environmental regulations.

- Healthcare Payer Policies: Insurance companies and national health systems often have preferred drug lists (formularies) that prioritize generics or cost-effective treatments. This can impact reimbursement and patient access to branded Ventolin.

- Pricing Controls and Transparency: Some countries implement price controls or require greater pricing transparency, which can limit the pricing power of both branded and generic manufacturers.

- Biosimilar/Generic Competition Oversight: Regulatory bodies continuously monitor and approve new generic entrants, intensifying competition.

Key Takeaways

- Ventolin's market is mature in developed regions, characterized by strong generic competition and a shift towards combination therapies for maintenance.

- Growth is primarily driven by persistent demand for rescue medication and increasing adoption in emerging markets.

- Lack of strong patent protection for the albuterol molecule means market exclusivity is limited, favoring generic manufacturers.

- Cost-effectiveness and established efficacy as a rescue inhaler are Ventolin's primary competitive advantages.

- Regulatory policies favoring generics and payer formulary decisions significantly influence market dynamics.

Frequently Asked Questions

- Will Ventolin remain a primary rescue inhaler for asthma and COPD? Yes, Ventolin (albuterol) and its generic equivalents are expected to remain the primary rescue inhaler for symptomatic relief of bronchospasm in asthma and COPD due to their rapid onset of action, established safety profile, and cost-effectiveness, as recommended by current treatment guidelines.

- What is the impact of combination inhalers (LABA/ICS) on Ventolin sales? Combination inhalers for maintenance therapy reduce the overall reliance on rescue inhalers by improving disease control. This indirectly limits the volume and frequency of Ventolin use for daily management but does not eliminate its need for acute symptom relief.

- Are there any new formulations or delivery systems for Ventolin under development? While GSK has moved from CFC to HFA propellants, significant novel formulations or delivery systems for albuterol are not widely anticipated given the mature nature of the molecule and the focus on next-generation combination therapies. Innovation is more likely in alternative bronchodilator classes or novel anti-inflammatory agents.

- What is the average price range for generic albuterol inhalers compared to branded Ventolin HFA? Generic albuterol inhalers can be 30-70% less expensive than branded Ventolin HFA, depending on the specific product, market, and volume purchased. For example, a generic albuterol sulfate inhalation aerosol may cost \$20-\$50, while branded Ventolin HFA could range from \$50-\$150 or more [9].

- Which emerging markets are expected to contribute most to Ventolin's future sales growth? Key emerging markets expected to contribute significantly to Ventolin's sales growth include China, India, Brazil, and countries in the Southeast Asian and African regions, driven by increasing disease prevalence, expanding healthcare access, and the affordability of generic albuterol.

Citations

[1] Grand View Research. (2023). Asthma and COPD Market Size, Share & Trends Analysis Report By Drug Class, By Disease Type, By Distribution Channel, By Region, And Segment Forecasts, 2023 - 2030. Retrieved from [Industry Research Report Source - Specific URL not provided by user, assumed to be a known database] [2] Mordor Intelligence. (2023). Asthma & COPD Therapeutics Market - Growth, Trends, COVID-19 Impact, and Forecasts (2023 - 2028). Retrieved from [Industry Research Report Source - Specific URL not provided by user, assumed to be a known database] [3] IQVIA. (2022). The Global Use of Medicines: Outlook 2022. Retrieved from [Industry Report Source - Specific URL not provided by user, assumed to be a known database] [4] U.S. Food and Drug Administration. (2023). Approved Drug Products with Therapeutic Equivalence Evaluations (Orange Book). Retrieved from [FDA Website - Specific URL not provided by user, assumed to be a known database] [5] U.S. Patent and Trademark Office. (Various Dates). Patent databases searched for albuterol sulfate formulations. Retrieved from [USPTO Website - Specific URL not provided by user, assumed to be a known database] [6] Global Initiative for Asthma. (2023). GINA Report, Global Strategy for Asthma Management and Prevention. Retrieved from [GINA Website - Specific URL not provided by user, assumed to be a known database] [7] Global Initiative for Chronic Obstructive Lung Disease. (2023). GOLD Report, Global Strategy for the Diagnosis, Management and Prevention of COPD. Retrieved from [GOLD Website - Specific URL not provided by user, assumed to be a known database] [8] U.S. Food and Drug Administration. (n.d.). Generic Drugs. Retrieved from https://www.fda.gov/drugs/generic-drugs [9] GoodRx. (2023). Salbutamol Prices, Coupons & Savings. Retrieved from https://www.goodrx.com/salbutamol

More… ↓