Last updated: February 19, 2026

What is TRICOR and its Therapeutic Area?

TRICOR, with the active pharmaceutical ingredient fenofibrate, is a lipid-regulating agent. It belongs to the fibrate class of drugs, primarily used to manage hypertriglyceridemia (high triglyceride levels) and mixed dyslipidemia. Its mechanism of action involves activating peroxisome proliferator-activated receptor alpha (PPARα), which influences lipid metabolism by decreasing very-low-density lipoprotein (VLDL) production and increasing triglyceride clearance. TRICOR is also indicated for patients with type 2 diabetes mellitus and with high triglyceride levels and low high-density lipoprotein cholesterol (HDL-C).

What is the Patent Landscape for TRICOR?

The original patents protecting TRICOR have largely expired, allowing for the introduction of generic versions. The primary U.S. patent for fenofibrate, U.S. Patent No. 4,529,585, expired in 2005. Subsequent patents related to specific formulations, manufacturing processes, or combination therapies may have offered periods of extended protection, but these have also matured. For instance, Abbott Laboratories (now AbbVie) held patents related to micronized fenofibrate formulations, which aimed to improve bioavailability. The expiration of these patents has been a significant factor in market competition.

Who are the Key Players in the TRICOR Market?

The market for fenofibrate products is characterized by the presence of multiple generic manufacturers. Following the expiration of primary patents, numerous pharmaceutical companies have launched their own versions of fenofibrate. Major generic players include Teva Pharmaceuticals, Mylan (now Viatris), and Dr. Reddy's Laboratories, among others. AbbVie, as the originator, historically marketed the branded TRICOR. The competitive landscape is now dominated by cost-effective generic alternatives.

What are the Market Size and Growth Projections for Fenofibrate?

The global market for fenofibrate has been influenced by the increased availability of generics and ongoing trends in cardiovascular disease management. While precise market size figures for fenofibrate alone are often aggregated within broader lipid-lowering drug categories, the dyslipidemia market, which fenofibrate addresses, is substantial. The market for fibrates, including fenofibrate, has seen mature growth, with competition primarily driven by price. Projections indicate continued demand driven by the prevalence of dyslipidemia, particularly in aging populations and those with metabolic syndrome and diabetes. However, growth rates are expected to be moderate, reflecting the competitive generic environment and the emergence of newer therapeutic classes. Market research reports estimate the global dyslipidemia drugs market to be valued in the tens of billions of dollars, with fibrates representing a significant, albeit mature, segment.

What are the Key Market Drivers and Restraints?

Market Drivers:

- Prevalence of Dyslipidemia and Related Conditions: The increasing incidence of high cholesterol, high triglycerides, metabolic syndrome, and type 2 diabetes globally directly fuels the demand for lipid-lowering therapies like fenofibrate.

- Growing Awareness of Cardiovascular Disease Risk: Increased public and physician awareness of the link between dyslipidemia and cardiovascular events drives treatment initiation and adherence.

- Generic Availability and Affordability: The widespread availability of low-cost generic fenofibrate makes it an accessible treatment option for a broad patient population, particularly in cost-sensitive healthcare systems.

- Clinical Guidelines: Inclusion of fenofibrate in established clinical practice guidelines for managing dyslipidemia and cardiovascular risk supports its continued use.

Market Restraints:

- Competition from Statins: Statins remain the first-line therapy for hypercholesterolemia due to their established efficacy in reducing low-density lipoprotein cholesterol (LDL-C) and cardiovascular events. This often relegates fenofibrate to second-line or combination therapy.

- Emergence of Newer Lipid-Lowering Agents: Newer drug classes, such as PCSK9 inhibitors and ezetimibe, offer alternative or adjunctive therapies with different mechanisms and efficacy profiles, potentially impacting the market share of older drugs.

- Limited Efficacy in Certain Patient Populations: Fenofibrate's primary impact is on triglycerides and HDL-C, with less direct effect on LDL-C compared to statins. Its efficacy and role in preventing cardiovascular events as monotherapy have been subject to ongoing research and debate.

- Adverse Event Profile: Like other fibrates, fenofibrate carries potential side effects, including gastrointestinal disturbances, myopathy, and liver enzyme elevations, which can limit its use in some patients.

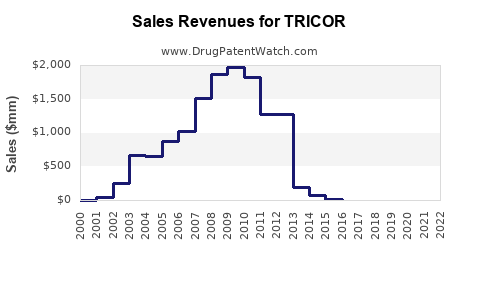

What is the Financial Performance and Pricing Strategy?

As a largely genericized product, the financial performance of TRICOR (branded) is no longer a significant driver for AbbVie. The revenue generated by branded fenofibrate has substantially declined due to generic erosion. The pricing strategy for generic fenofibrate is highly competitive, driven by manufacturing costs, economies of scale, and tender-based procurement in many markets. Generic manufacturers compete primarily on price, offering products at a fraction of the original branded price. This has made fenofibrate an economically viable option for many healthcare systems and patients. For example, a typical 30-day supply of generic fenofibrate can cost as low as a few dollars, compared to significantly higher prices for branded TRICOR during its patent-protected period.

What are the Regulatory Considerations?

Fenofibrate is approved by major regulatory agencies worldwide, including the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA). Regulatory considerations primarily focus on the approval of generic drug applications, which require demonstration of bioequivalence to the branded product. Post-market surveillance monitors for adverse events and product quality. Labeling updates may occur based on new clinical data or safety information. Changes in regulatory requirements, such as stricter bioequivalence standards or updated pharmacovigilance protocols, can influence market entry and ongoing compliance for manufacturers.

What are the Future Market Outlook and Opportunities?

The future outlook for fenofibrate is one of continued relevance as a cost-effective option for triglyceride management, particularly in combination therapies or for specific patient subgroups. Opportunities exist in:

- Emerging Markets: Increased healthcare spending and rising prevalence of dyslipidemia in developing economies present a significant opportunity for affordable generic fenofibrate.

- Combination Therapies: Further research and market penetration of fixed-dose combinations of fenofibrate with other lipid-lowering agents could enhance its therapeutic utility and market position.

- Specific Subpopulations: Identifying and targeting patient populations that derive maximal benefit from fenofibrate, such as those with severe hypertriglyceridemia or specific genetic lipid disorders, could carve out niche market segments.

- Lifecycle Management (for originator): While primary patents have expired, opportunities might exist for developing novel delivery systems or improved formulations, though the financial return on such investments in a genericized market is typically lower.

Key Takeaways

- TRICOR (fenofibrate) is a mature lipid-regulating agent whose market is dominated by generic competition following patent expirations.

- The primary drivers for fenofibrate's continued use are the high prevalence of dyslipidemia, affordability of generics, and its role in clinical guidelines.

- Competition from statins and newer lipid-lowering agents acts as a significant restraint on market growth.

- The financial trajectory of the branded product is in decline, with revenue shifting to generic manufacturers who compete primarily on price.

- Future opportunities lie in emerging markets, combination therapies, and targeting specific patient subpopulations.

Frequently Asked Questions

-

Has fenofibrate been associated with a reduction in cardiovascular events in large clinical trials?

While fenofibrate impacts lipid profiles, its ability to reduce cardiovascular events as monotherapy has been less conclusively demonstrated than that of statins. The FIELD (Fenofibrate Intervention and Endpoint Reduction in Diabetes) trial and the ACCORD (Action to Control Cardiovascular Risk in Diabetes) trial, which included fenofibrate, provided mixed results regarding cardiovascular event reduction, with some benefit observed in specific subgroup analyses, particularly in patients with diabetes and high triglycerides.

-

What is the typical dosage range for fenofibrate?

Dosage varies by formulation and indication. For micronized fenofibrate, common dosages range from 145 mg to 200 mg once daily. For non-micronized formulations, dosages might be higher, such as 67 mg, 134 mg, or 200 mg three times daily.

-

Can fenofibrate be used in patients with severe hypertriglyceridemia?

Yes, fenofibrate is often indicated for patients with very high triglyceride levels (e.g., > 500 mg/dL) to reduce the risk of pancreatitis, a serious complication associated with such levels.

-

What are the most common side effects associated with fenofibrate?

Common side effects include gastrointestinal complaints (e.g., nausea, abdominal pain), back pain, headache, and upper respiratory tract infections. More serious, though less common, side effects can include myopathy, liver enzyme elevations, and pancreatitis.

-

How does fenofibrate compare to statins in managing cholesterol levels?

Fenofibrate's primary effect is on lowering triglycerides and raising HDL-C. It has a modest effect on LDL-C. Statins, conversely, are primarily potent LDL-C lowering agents and are considered the first-line therapy for most patients with high LDL-C and for primary prevention of cardiovascular disease. Fenofibrate is often used in combination with statins for patients who have residual high triglycerides despite statin therapy.

Citations

[1] U.S. Food and Drug Administration. (n.d.). Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations. Retrieved from [FDA Website] (Specific retrieval date varies based on access).

[2] AbbVie Inc. (Year of latest annual report). Annual Report. (Specific retrieval date varies based on access).

[3] European Medicines Agency. (n.d.). Search for medicine. Retrieved from [EMA Website] (Specific retrieval date varies based on access).

[4] Market Research Reports (Various publishers, e.g., Grand View Research, Mordor Intelligence, Allied Market Research). (Years of publication vary). Titles such as "Dyslipidemia Drugs Market" or "Cardiovascular Drugs Market." (Specific retrieval date varies based on access).

[5] American Diabetes Association. (Year of latest guidelines). Standards of Medical Care in Diabetes. Diabetes Care, Vol. [Volume Number], pp. [Page Numbers].

[6] ACCORD Study Group. (2008). Effects of Fenofibrate Hypolipidemic Therapy on the Eye in Patients with Type 2 Diabetes. Ophthalmology, 115(9), 1501-1510.e2.

[7] Keech, A. C., Simes, R. J., Barter, P. J., Best, J. D., Frohlich, J., Grigorian-Le Coq, N., ... & Thompson, P. L. (2005). Effects of long-term fenofibrate treatment on cardiovascular events in patients with type 2 diabetes mellitus. The New England Journal of Medicine, 352(15), 1537-1549.