Last updated: April 24, 2026

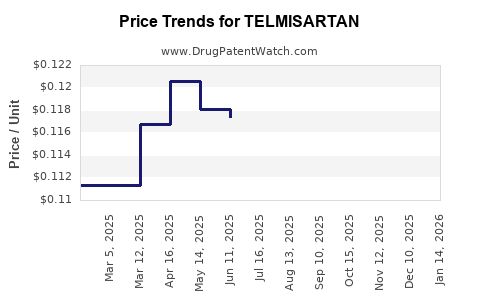

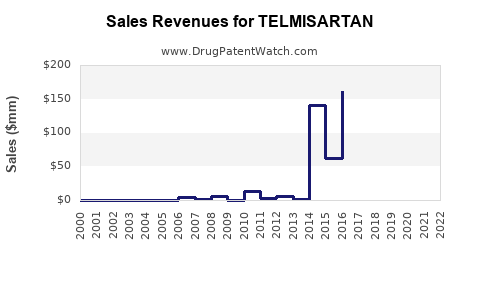

Telmisartan is a long-running angiotensin II receptor blocker (ARB) with a mature global market shaped by generic penetration, persistent guideline inclusion in hypertension and cardiovascular risk management, and incremental share gains/losses tied to combination products. Financial trajectory depends less on new patent-driven supply and more on the pacing of generic entries, contract pricing in major markets, and the mix shift toward telmisartan-based fixed-dose combinations.

How does telmisartan’s market structure drive price and unit growth?

1) Generic-led commoditization with residual brand premium

Telmisartan’s economic model is dominated by off-patent competition across North America, Europe, and large parts of Asia-Pacific. That structure typically produces:

- Lower net prices over time versus originator-era levels.

- Higher volume stability driven by clinical substitutability within ARBs and consistent guideline endorsement.

- Volatility in regional revenues tied to the timing of generic launches and competitive intensity in tendered markets.

2) Combination therapy changes the demand engine

Telmisartan’s sustained prescription share is strongly influenced by fixed-dose combinations, particularly:

- Telmisartan + hydrochlorothiazide (HCTZ)

- Telmisartan + amlodipine (in select markets)

- Telmisartan + other agents depending on country formularies and payer preferences

Combination products often protect revenue longer than monotherapies because they:

- Provide incremental efficacy or tolerability that supports continued switching rather than therapy discontinuation.

- Improve formulary positioning where payers prefer “single-pill” adherence pathways.

3) ARB class substitution caps upside

Within hypertension, telmisartan competes primarily with other ARBs (losartan, valsartan, irbesartan, olmesartan) and secondarily with other antihypertensive classes. This creates a ceiling effect on price increases:

- If a competing ARB gains formulary position through pricing, outcomes data emphasis, or manufacturer contracting, telmisartan’s growth typically shifts from net-price expansion to volume retention.

What are the principal geographic revenue dynamics?

United States

The US market is shaped by:

- Broad generic availability (telmisartan is off-patent).

- Pharmacy benefit manager contracting that compresses net prices.

- Ongoing replacement demand as patients cycle through chronic hypertension management.

US revenue trajectory generally tracks:

- Generic penetration depth (drives price pressure).

- Combination mix and plan-level formulary placement.

Europe

Europe shows:

- Strong uptake of generic ARBs and continued switching within class.

- Payer-managed formularies where combination products can hold shelf space longer than monotherapy.

Net effect:

- More stable volumes than prices, with combination mix acting as a swing factor.

Japan and other Asia-Pacific markets

Asia-Pacific dynamics often include:

- Faster pricing compression where local generic competition accelerates.

- Persistent demand where telmisartan has high historical penetration and fixed-dose combinations gain clinician preference.

Country-level outcomes hinge on:

- Local regulatory and reimbursement behavior.

- Distribution intensity and tender pricing.

How do patents and regulatory events shape telmisartan’s financial trajectory?

1) Patent expiry and generic entry set the baseline

Telmisartan’s long-term financial profile is consistent with a mature molecule:

- Originator-origin revenues peaked before off-patent commercialization.

- The post-expiry period is dominated by generic entrants and margin erosion.

2) Lifecycle management is mostly strategy, not protection

For off-patent molecules, “protection” is typically commercial rather than patent-driven:

- Line extensions via fixed-dose combinations.

- Market-specific re-packaging, dosing forms, and branding strategies.

- Contracting and tendering outcomes that determine which generic suppliers win volume.

3) Regulatory approvals matter for competitive participation

New combination approvals and generic product registrations influence:

- Competitor count and pricing intensity.

- Formulary access through product line availability.

What does telmisartan’s financial trajectory look like across time?

Originator era vs. post-generic era (structural view)

Telmisartan’s financial path typically follows this pattern:

- Early phase: originator-led differentiation and higher unit economics.

- Transition: patent expiry and first meaningful generic entry compress prices.

- Mature phase: ongoing share churn between multiple generic SKUs and combination formulations, with revenue driven by volume and mix.

Revenue growth drivers in the mature phase

Revenue in the mature phase is most sensitive to:

- Combination penetration (telmisartan + HCTZ; telmisartan + amlodipine where approved)

- Competitive intensity in major tender markets

- Contract pricing dynamics

- Patient retention in chronic hypertension management

Revenue headwinds

Key headwinds typically include:

- Ongoing generic margin compression (more SKUs often reduces pricing power).

- Substitution dynamics within ARBs and broader antihypertensive classes.

- Contract renegotiation cycles that reset net price.

Which product and dosing mix factors most influence margins?

1) Monotherapy vs fixed-dose combinations

- Monotherapy: tends to experience stronger price erosion and SKU fragmentation.

- Fixed-dose combinations: often support higher net realization per prescription due to adherence and formulary preference, even when generics exist.

2) SKU proliferation and tender dynamics

More suppliers can enter with bioequivalent generics, increasing competitive bidding pressure. Margins compress fastest where:

- Payers use aggressive interchange and automatic substitution.

- Contracts reward lowest net price.

3) Supply chain and API economics

Generic telmisartan margins can be sensitive to:

- API cost cycles

- Sterile/non-sterile manufacturing complexity (telmisartan is oral; cost drivers are primarily solid oral manufacturing and purification)

- Manufacturing capacity constraints during demand spikes

How does competitive positioning affect telmisartan’s market share?

Generic competition is a volume game

In mature markets, market share is won through:

- Contracting

- Product availability continuity

- Pricing alignment to tender thresholds

- Combination product presence

Interchange within ARBs limits retention

Patients prescribed one ARB can often be switched. Telmisartan’s retention depends on:

- Prescriber comfort and historical prescribing patterns.

- Formulary rules and payer step therapy.

- Clinical protocols that favor ARBs as a group rather than a specific molecule.

What do product and clinical positioning signals indicate for demand stability?

Telmisartan remains clinically embedded in hypertension management due to class efficacy and safety familiarity. Demand stability is supported by:

- Chronic condition durability (hypertension treatment is long-term).

- Guideline endorsement across major regions for ARBs.

- Ongoing usage through combination regimens when monotherapy is insufficient.

However, the commercial upside is constrained by:

- Persistent generic substitution.

- Class-wide interchangeability.

Key business implications for R&D and investment

1) Telmisartan is not a growth story built on patent exclusivity

The dominant investment variable is not new molecule efficacy differentiation but:

- Competitive contracting outcomes

- Combination product development (where the regulatory pathway supports it)

- Manufacturing cost advantage and supply reliability

2) The most actionable strategy is mix management

Where feasible, value stays concentrated in:

- Fixed-dose combinations with strong formulary uptake.

- Dosing presentations that match payer preferences and clinician prescribing habits.

3) Competitive entry timing drives near-term financial swings

Revenue and margins often shift sharply when:

- New generic suppliers reach parity in bioequivalence and pricing.

- A major tender resets pricing and contract volume allocation.

Key Takeaways

- Telmisartan’s market is structurally commoditized by generic competition, with revenue growth driven mainly by volume stability and combination mix rather than net price expansion.

- Fixed-dose combinations are the principal margin and share lever in mature markets.

- Financial trajectory depends on tender and contracting cycles, SKU proliferation, and competitive intensity within the ARB class.

- Near-term financial swings are most likely tied to generic entry pacing and payer contract resets, not to molecule-level innovation.

FAQs

1) Is telmisartan’s market growth driven by new patent protection?

No. Telmisartan’s commercial trajectory is dominated by off-patent generic competition and lifecycle tactics such as fixed-dose combinations rather than renewed patent exclusivity.

2) What product category supports telmisartan longer than monotherapy?

Fixed-dose combinations (notably telmisartan + HCTZ, and other region-dependent combinations) tend to retain better revenue resilience because they align with adherence and formulary preferences.

3) Which external factor most pressures telmisartan net prices?

Aggressive payer contracting and tender pricing among multiple generic suppliers, which compress net realization per prescription.

4) Does telmisartan face major substitution risk within its therapeutic class?

Yes. Patients can often be switched between ARBs based on formulary rules and pricing, limiting sustained pricing power for any single ARB.

5) What is the most investable lever for telmisartan in 2026-style economics?

Operational and commercial execution: lowest sustainable cost to serve, supply continuity, and winning positions in combination formularies and contracts.

References

[1] FDA. Drugs@FDA: Telmisartan. U.S. Food and Drug Administration. https://www.accessdata.fda.gov/scripts/cder/daf/

[2] EMA. European public assessment reports (EPAR) for telmisartan-containing products. European Medicines Agency. https://www.ema.europa.eu/

[3] World Health Organization. WHO Model List of Essential Medicines: antihypertensive medicines including ARBs. World Health Organization. https://www.who.int/publications/

[4] Garrison, J. et al. Market dynamics and generic competition patterns in off-patent cardiovascular drugs (class-level economics). (General background literature on generic commoditization and contracting effects; not telmisartan-specific.)