Last updated: August 2, 2026

Paricalcitol is a mature vitamin D receptor agonist used to control secondary hyperparathyroidism in patients with chronic kidney disease. Its commercial profile has shifted from branded specialty medicine to a generic injectable and oral product. The principal value drivers are dialysis-center utilization, generic pricing, renal-care treatment protocols, and competition from calcimimetics such as cinacalcet and etelcalcetide.

Zemplar, the original paricalcitol brand, no longer has meaningful exclusivity protection in the United States. Generic entry has compressed pricing and removed the economic basis for substantial branded revenue. The market remains clinically relevant, but its financial trajectory is mature, fragmented, and volume-driven.

What is paricalcitol and how is it used?

Paricalcitol is a synthetic vitamin D analog and selective vitamin D receptor agonist. It is indicated for the prevention and treatment of secondary hyperparathyroidism associated with chronic kidney disease, including patients receiving hemodialysis and, depending on formulation and jurisdiction, patients with earlier-stage renal impairment.

The drug reduces parathyroid hormone production while producing less intestinal calcium and phosphate absorption than some conventional vitamin D therapies. Its main clinical objectives are:

- Lowering elevated parathyroid hormone levels.

- Reducing the risk of renal osteodystrophy.

- Managing mineral-bone disorder associated with chronic kidney disease.

- Controlling parathyroid hormone in dialysis populations.

Paricalcitol is marketed in injectable and oral forms. The injectable product is administered primarily in dialysis settings, while capsules are used in outpatient treatment.

The drug does not replace renal-replacement therapy and does not correct the underlying loss of kidney function. Its commercial demand is therefore linked to the size of the chronic kidney disease and dialysis populations rather than to short-course prescribing.

What is the FDA regulatory status of paricalcitol?

The FDA approved Zemplar injection in 1998 and later approved oral capsules for secondary hyperparathyroidism associated with chronic kidney disease. The original product was developed by Abbott Laboratories, whose pharmaceutical operations later became part of AbbVie.[1][2]

| Regulatory item |

Status |

| Active ingredient |

Paricalcitol |

| Drug class |

Vitamin D receptor agonist |

| Primary indication |

Secondary hyperparathyroidism associated with chronic kidney disease |

| Original U.S. brand |

Zemplar |

| Original sponsor |

Abbott Laboratories |

| Current market structure |

Generic and legacy branded products |

| Key dosage forms |

Injection and capsules |

| Primary care setting |

Dialysis centers, nephrology clinics, outpatient renal care |

| Biosimilar pathway |

Not applicable; paricalcitol is a small-molecule drug |

| FDA generic pathway |

Abbreviated New Drug Application, or ANDA |

The FDA label warns that paricalcitol can cause hypercalcemia and hyperphosphatemia. Monitoring serum calcium, phosphorus and parathyroid hormone remains central to treatment.[1]

When did paricalcitol lose market exclusivity?

Paricalcitol lost meaningful U.S. exclusivity years ago. The original composition and formulation patent estate has expired, and generic products are available for both injectable and oral presentations.

The exact commercial launch date for each generic varies by manufacturer and dosage form. Generic availability has been established for years, with multiple approved products listed in FDA databases and product-label repositories.[3][4]

| Exclusivity category |

Current position |

| New chemical entity exclusivity |

Expired |

| Original brand patent protection |

Expired |

| Orphan-drug exclusivity |

Not applicable |

| Pediatric exclusivity |

No current blocking protection |

| Generic competition |

Established |

| Current commercial barrier |

Manufacturing, distribution and contracting rather than patent exclusivity |

Paricalcitol therefore has no credible patent-based route to a new branded monopoly in the United States. Any remaining commercial differentiation depends on supply reliability, sterile-manufacturing capacity, formulation convenience, contracting access and regulatory compliance.

What patents protect paricalcitol?

The original Zemplar patent estate covered paricalcitol and related vitamin D analog chemistry, pharmaceutical compositions and methods of use. Those rights are no longer commercially blocking in the United States.

The relevant patent categories historically included:

Composition-of-matter patents

Early patents covered vitamin D analog structures and compounds with activity at the vitamin D receptor. These patents established the foundational protection for paricalcitol but have expired.

Formulation patents

Additional protection covered injectable and oral dosage forms, excipient systems, concentrations and administration approaches. These rights also no longer provide meaningful exclusion against standard generic paricalcitol products.

Method-of-use patents

The clinical use of paricalcitol to treat secondary hyperparathyroidism in chronic kidney disease was part of the original branded regulatory and patent strategy. Method-of-use protection has expired or ceased to be commercially relevant for standard indications.

Manufacturing and process protection

Process patents may have covered synthesis, purification or formulation operations. Such patents can remain relevant to manufacturing efficiency, but they do not create a broad market barrier where alternative non-infringing processes are available.

The strongest remaining intellectual-property barriers are practical rather than legal. Sterile injectable production, validated analytical methods, regulatory filing requirements and consistent supply are more important than patent exclusivity.

What is the Orange Book status of paricalcitol?

The FDA Orange Book historically listed Zemplar products and related patents. Orange Book significance has declined as the original patent estate expired and ANDA-approved products became established.

For generic applicants, the main regulatory issues were historically:

- Patent certification under Paragraph I, II, III or IV.

- Label consistency with the reference-listed drug.

- Bioequivalence for oral products.

- Injectable-product quality and pharmaceutical equivalence.

- Compliance with current good manufacturing practice requirements.

Because paricalcitol is an old small-molecule product with expired primary exclusivity, current Orange Book listings do not create a material barrier to generic entry. A manufacturer seeking to launch a new product would still need to evaluate any remaining listed patents, regulatory exclusivity and product-specific requirements at the time of filing.

Which companies manufacture or compete with paricalcitol?

Competition exists across branded remnants, generic pharmaceutical manufacturers and substitute therapies. Generic availability is typically distributed among manufacturers that supply hospital, dialysis and specialty-pharmacy channels.

Potential commercial competitors include companies with FDA-approved paricalcitol products listed in FDA or DailyMed records. Product availability can vary by strength, presentation, supplier and time period.[3][4]

The competitive landscape also includes pharmacologic substitutes:

| Therapy |

Role in renal care |

Competitive effect on paricalcitol |

| Paricalcitol |

Vitamin D receptor agonist |

Base product under analysis |

| Calcitriol |

Active vitamin D therapy |

Lower-cost clinical substitute |

| Doxercalciferol |

Vitamin D analog |

Competes in secondary hyperparathyroidism |

| Cinacalcet |

Oral calcimimetic |

Reduces reliance on vitamin D analogs in some patients |

| Etelcalcetide |

Injectable calcimimetic |

Important dialysis-center substitute |

| Nutritional vitamin D |

Vitamin D supplementation |

Used in selected patients, usually not a full substitute for active analog therapy |

Calcimimetics exert the greatest strategic pressure because they lower parathyroid hormone through a different mechanism and can be integrated into dialysis protocols. Treatment selection depends on calcium and phosphate levels, disease severity, tolerability, reimbursement and local practice.

How strong is the paricalcitol patent estate?

The current patent estate is weak from a commercial-exclusivity perspective.

| Patent-strength factor |

Assessment |

| Composition protection |

Expired |

| Core method-of-use protection |

Expired or non-blocking |

| Formulation protection |

Expired or narrow |

| Generic entry exposure |

High |

| Litigation leverage |

Low |

| Manufacturing know-how value |

Moderate |

| Regulatory complexity |

Moderate for injection, lower for established oral products |

| Repricing ability |

Low |

Paricalcitol has a stronger operational moat in sterile manufacturing than in intellectual property. Injectable products require controlled production, validated sterilization and quality systems. A manufacturing failure can affect supply, but the barrier is not equivalent to an enforceable patent monopoly.

What generic entry risks exist for Zemplar?

Generic entry risk is effectively realized rather than prospective. Zemplar faces:

- Price erosion from multiple generic suppliers.

- Loss of formulary preference.

- Substitution by hospital and dialysis-center purchasing departments.

- Contracting pressure from large renal-care providers.

- Switching to cinacalcet or etelcalcetide.

- Reduced physician sensitivity to brand differentiation.

- Supply interruptions that can shift market share between manufacturers.

The injectable market may experience less immediate supplier competition than oral capsules because sterile manufacturing is more complex. That can support temporary price stability during shortages. It does not restore the historical branded economics.

Has paricalcitol faced Paragraph IV challenges or patent litigation?

Paricalcitol’s principal generic challenge period occurred after the original brand protections became vulnerable. Paragraph IV litigation is not a material current market issue because the core patent estate has expired and generic products are established.

The available public record does not identify an active, market-blocking U.S. patent dispute that could restore Zemplar exclusivity. Earlier ANDA-related disputes, if any, would have been resolved through patent expiration, settlement, dismissal or generic launch.

What settlement agreements affected paricalcitol?

No widely reported current settlement agreement appears to control U.S. paricalcitol competition. Any historical agreement would need to be assessed against the specific patent, dosage form, applicant and launch date. Such agreements no longer appear to create a broad barrier to generic supply.

How has the financial trajectory of paricalcitol evolved?

Paricalcitol’s financial trajectory follows the standard lifecycle of an older specialty drug:

Launch and growth phase

Zemplar entered a market with a large and recurring dialysis population. Demand benefited from chronic treatment, physician familiarity and use in dialysis centers. Injectable administration created a channel tied to supervised renal care.

Mature branded phase

During the branded period, revenue was supported by repeat use and the clinical need to manage secondary hyperparathyroidism. Sales were exposed to nephrology prescribing patterns, dialysis-center contracts and reimbursement changes.

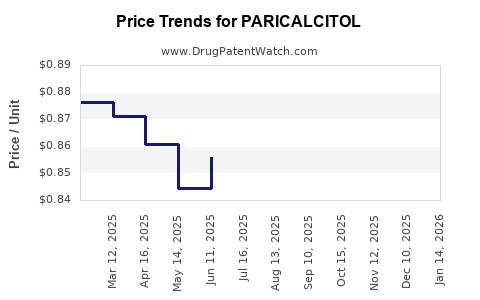

Generic erosion phase

After patent expiration, generic competition reduced average selling prices. Revenue shifted from branded economics to aggregate market volume. The injectable presentation likely retained more operational value than capsules because of administration requirements and purchasing complexity.

Current mature phase

Paricalcitol is now a low-growth, price-sensitive product. The market can still generate stable unit demand because chronic kidney disease and dialysis are recurring conditions. Revenue growth is limited by:

- Generic price deflation.

- Greater use of calcimimetics.

- Dialysis-provider purchasing power.

- Treatment guideline changes.

- Competitive availability of calcitriol and doxercalciferol.

- Lack of meaningful product differentiation.

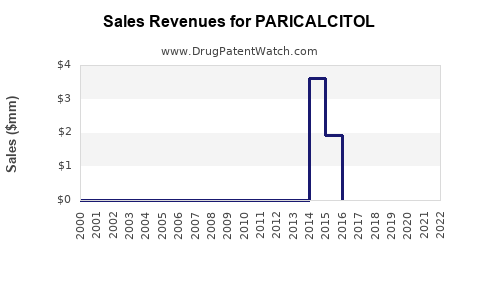

Abbott and AbbVie financial disclosures have not established a current, separately reported paricalcitol revenue stream that would support a reliable standalone valuation. The drug should therefore be analyzed as part of a mature renal-care portfolio rather than as a significant independent growth asset.[2][5]

What is the revenue exposure for manufacturers?

Revenue exposure is asymmetric.

Brand owner exposure

The original brand owner has low current exposure because patent protection has expired and generic substitution is established. Any remaining branded revenue is likely limited by formulary displacement and contracting pressure.

Generic manufacturer exposure

Generic suppliers face lower per-unit revenue but can benefit from recurring demand. Their financial exposure is primarily operational:

- API availability.

- Sterile-fill capacity.

- Quality compliance.

- Supply contracts.

- Competitive pricing.

- Product recalls or shortages.

Dialysis-provider exposure

Dialysis providers may influence product selection through formularies and purchasing contracts. Their economic incentives can favor lower-cost generic vitamin D analogs, but they may also use calcimimetics depending on reimbursement and treatment protocols.

Investor relevance

Paricalcitol is unlikely to be a material growth catalyst for a large pharmaceutical company. It can contribute predictable cash flow in a generic portfolio, but its valuation depends on volume retention and manufacturing efficiency rather than on exclusivity expansion.

How does paricalcitol compare with cinacalcet and etelcalcetide?

Paricalcitol and calcimimetics address secondary hyperparathyroidism through different mechanisms.

| Attribute |

Paricalcitol |

Cinacalcet |

Etelcalcetide |

| Drug class |

Vitamin D receptor agonist |

Oral calcimimetic |

Injectable calcimimetic |

| Main setting |

CKD, including dialysis |

CKD with secondary hyperparathyroidism |

Hemodialysis |

| Administration |

Injection or oral capsule |

Oral |

Intravenous after hemodialysis |

| Key monitoring |

Calcium, phosphate, PTH |

Calcium, PTH, gastrointestinal tolerability |

Calcium, PTH |

| Patent position |

Mature and expired |

Mature; generic competition established |

Later-generation product with more recent commercial history |

| Competitive role |

Vitamin D analog option |

Direct pharmacologic substitute |

Direct dialysis-center substitute |

Paricalcitol may be favored when clinicians seek PTH control with a vitamin D analog and calcium or phosphate management permits its use. Calcimimetics may be favored when hypercalcemia or hyperphosphatemia limits vitamin D therapy. Treatment is often individualized rather than determined by a single class-wide preference.[6]

What manufacturing and intellectual-property barriers remain?

The main barriers are regulatory and operational.

Injectable manufacturing

Paricalcitol injection requires sterile production, container-closure integrity, validated process controls and reliable supply of pharmaceutical-grade active ingredient. These requirements can reduce the number of credible suppliers.

Oral manufacturing

Capsules are easier to manufacture than sterile injections, but generic suppliers still need to demonstrate pharmaceutical equivalence, bioequivalence and consistent content uniformity.

API sourcing

API availability affects cost and continuity. A supplier with redundant API sources and established regulatory documentation has an advantage over a low-cost but fragile competitor.

Regulatory maintenance

Manufacturers must maintain approved labeling, pharmacovigilance systems, product quality and FDA compliance. These obligations support incumbent generic suppliers but do not create durable exclusivity.

What is the geographic coverage of paricalcitol?

Paricalcitol has been marketed in the United States and other jurisdictions under the Zemplar name or generic names. Market access varies by country because approval status, reimbursement, dialysis organization, patent history and generic substitution rules differ.

The United States is the most important reference market for patent and FDA analysis. European and other markets may have different brand histories and national reimbursement dynamics. In most mature markets, the commercial pattern is similar: recurring renal-care demand, generic competition and limited opportunity for premium pricing.

What are the likely generic launch scenarios?

The most likely U.S. scenarios are:

Base case

Multiple generic suppliers remain active. Prices continue to decline gradually, while unit demand remains relatively stable because dialysis patients require long-term mineral-bone disorder management.

Supply-constrained case

A manufacturer exits or experiences a quality issue. Injectable supply tightens temporarily, allowing remaining suppliers to improve pricing and gain share. The effect is operational, not patent-driven.

Substitution case

Greater use of cinacalcet or etelcalcetide reduces paricalcitol volume. The impact is strongest in dialysis protocols that prioritize calcimimetics for patients with difficult calcium or phosphate profiles.

Portfolio-stability case

Paricalcitol remains a dependable low-growth product within a generic renal portfolio. Manufacturers with efficient sterile operations and strong dialysis contracts retain the best economics.

Key Takeaways

- Paricalcitol is a mature vitamin D receptor agonist for secondary hyperparathyroidism in chronic kidney disease.

- Zemplar’s original U.S. patent and exclusivity position has expired.

- Generic competition is established for injectable and oral products.

- The market has recurring clinical demand but limited pricing power.

- Sterile manufacturing and supply reliability are more important than patent protection.

- Cinacalcet and etelcalcetide are the principal pharmacologic competitors.

- Current branded revenue is unlikely to be material or separately disclosed by the original sponsor.

- Paragraph IV litigation and settlement agreements do not appear to create a current market-blocking issue.

- Generic manufacturers can generate stable but low-growth revenue through dialysis and renal-care channels.

- The principal risks are price erosion, substitution, supplier exits, quality events and reimbursement changes.

FAQs

Is paricalcitol still commercially relevant?

Yes. It remains relevant because secondary hyperparathyroidism is common in advanced chronic kidney disease and dialysis populations. Its commercial value is limited by generic pricing and competition from calcimimetics.

Is Zemplar still protected by patents?

No meaningful U.S. patent protection remains for the original paricalcitol product. The commercial market is open to established generic competition.

Is paricalcitol a biologic or biosimilar product?

No. Paricalcitol is a synthetic small-molecule drug. Generic approval is generally pursued through the ANDA pathway rather than the biosimilar pathway.

Which paricalcitol formulation has the strongest commercial position?

The injectable formulation may have greater supply-chain value because sterile manufacturing is more complex and dialysis-center purchasing is concentrated. The oral capsule is easier to substitute and manufacture.

Can a new paricalcitol product obtain premium pricing?

A standard paricalcitol product is unlikely to support premium pricing. A premium strategy would require a meaningful delivery, dosing, adherence or safety advantage supported by FDA approval and differentiated clinical evidence.

References

-

U.S. Food and Drug Administration. (2023). Zemplar (paricalcitol) injection and capsules prescribing information. FDA.

-

Abbott Laboratories. (2012). Annual report. Abbott Laboratories.

-

U.S. Food and Drug Administration. (2024). Approved drug products with therapeutic equivalence evaluations: Orange Book. FDA.

-

National Library of Medicine. (2024). DailyMed: Paricalcitol drug labels. U.S. National Library of Medicine.

-

AbbVie Inc. (2024). Annual report. AbbVie Inc.

-

Kidney Disease: Improving Global Outcomes. (2017). KDIGO 2017 clinical practice guideline update for the diagnosis, evaluation, prevention, and treatment of chronic kidney disease-mineral and bone disorder. Kidney International Supplements, 7(1), 1-59.