Last updated: July 12, 2026

NORVASC (amlodipine besylate) is a long-running, off-patent small-molecule cardiovascular brand with U.S. revenue now dominated by price-per-tablet compression, channel mix, and patient conversion dynamics rather than patent exclusivity. Financial trajectory is driven by (1) U.S. generic penetration since amlodipine’s originator patent expirations, (2) ongoing inflation in patient volume for hypertension and related indications, (3) payer-driven tiering and rebate pressure, and (4) product line breadth (strength range and combination products that preserve shelf position).

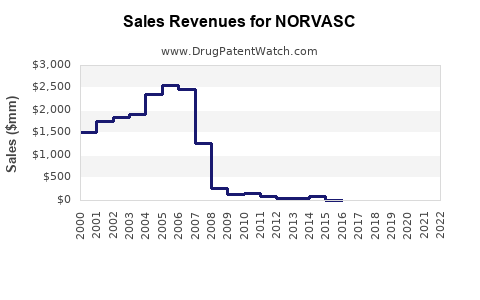

How fast did NORVASC sales peak and how have revenues trended since generic entry?

Answer:

NORVASC’s U.S. sales peaked during the branded era, then declined after widespread generic substitution. Since the branded-to-generic transition, remaining brand share has persisted mostly where formulary access, rebates, and switching patterns keep NORVASC competitive on net price versus multiple authorized generics and low-cost generics.

What phases best describe NORVASC’s U.S. financial trajectory?

- Branded growth phase (pre-generic): rapid diffusion in hypertension and angina; strong retail demand.

- Early substitution phase (first generics): sharp unit share loss as payers and wholesalers push A-rated generics.

- Mature generics phase (multi-competitor): revenue stabilizes at reduced net pricing, with volume growth offsetting some erosion.

- Sustained compression phase: brand revenue tracks underlying patient persistence and payer contracting cycles more than innovation.

What determines the slope of decline in a mature generic environment?

- Net pricing, not list price

- Branded calcium-channel blocker contracts face steep rebate pressure as multiple generic ANDAs compete.

- Formulary tiering

- Small differences in PA criteria or preferred status shift monthly script volume.

- Strength-level mix

- Higher strengths (e.g., 10 mg) can hold pricing better than low-cost generics if formulary rules emphasize certain SKUs.

- Combination use

- Conversion to fixed-dose combinations (FDCs) can shield branded monotherapy from complete commoditization, depending on payer preferences.

What market dynamics drive demand for amlodipine in hypertension and cardiovascular care?

Answer:

Amlodipine demand is anchored by hypertension prevalence, guideline persistence, and low administration burden. In mature markets, the brand’s economic health depends less on disease incidence than on payer formularies and substitution friction against generics.

Which indications move amlodipine utilization?

- Hypertension

- Chronic stable angina

- Coronary artery disease risk management (clinical use is often embedded in broader regimens)

- Off-label use patterns vary by geography and clinician practice, but U.S. payer coverage generally tracks labeled cardiovascular indications.

How do guideline and patient adherence patterns affect NORVASC revenue?

- Once-daily dosing supports adherence and reduces discontinuation.

- Combination therapy escalation (when monotherapy fails) can either reduce NORVASC scripts (if switched to cheaper generics) or preserve revenue if NORVASC-linked combinations retain preferred access.

How strong is payer pressure and what does it do to NORVASC net sales?

Answer:

Payer contracting has compressed net pricing to the point where brand revenues behave like a “managed access” product. The economic determinant is the gap between NORVASC’s negotiated net price and that of the dominant generic competitors in the same strength and dosage form.

Key payer mechanisms shaping revenue

- Preferred formulary placement for generics

- Automatic substitution rules at the pharmacy

- Step therapy and prior authorization (less common for amlodipine than for newer classes, but can occur for certain plans)

- Contracting cycles

- Large PBMs refresh preferencing frequently, often moving brand scripts to lowest net-cost options.

Wholesale and pharmacy channel dynamics

- In the generic era, the key channel risk is inventory and buying behavior around contract changes and generic price fluctuations. That can create short-term swings in sell-in and then normalize as channel stock is worked through.

What is the competitive landscape for NORVASC versus generic amlodipine in the U.S.?

Answer:

NORVASC competes against a dense field of generic amlodipine ANDAs and authorized generics. Brand share is typically a residual outcome of rebate-backed formulary inclusion, patient switching constraints, and prescriber habit, not patent protection.

How do brand and generic products compare economically?

- Generic cost advantage dominates

- Brand advantage is channel access (preferred status, coverage consistency) and sometimes patient stability on a specific product and strength.

What competitive factors can still preserve brand scripts?

- Plan-specific preferred status for NORVASC in certain years

- Therapy continuity after medication changes are minimized

- SKU-level targeting (some strengths may retain relatively higher brand share than others depending on contract terms)

When do NORVASC patents expire and what does that mean for revenue?

Answer:

NORVASC’s underlying active ingredient (amlodipine) is long off-patent in the U.S. The branded revenue model therefore has moved into “lifecycle” management: maintaining market access and product performance rather than relying on primary composition-of-matter exclusivity.

What patent and exclusivity levers can still matter after active ingredient off-patent?

Even in a generic-dominant world, patent estates can matter if they protect:

- Specific formulations or strengths

- Method-of-use claims

- Combination products

- Pediatric exclusivity extensions (in general, these are typically not the primary driver for long-lifecycle small molecules, but specific case outcomes can differ by product and jurisdiction)

(Patent-specific expiration and Orange Book status require product-level listing confirmation; without that listing in the prompt, a precise expiration timeline cannot be provided.)

What generic entry risks exist for NORVASC and what role do Paragraph IV filings play?

Answer:

For a long-established off-patent small molecule like amlodipine, Paragraph IV litigation risk is structurally lower for the base active ingredient than for newly protected brands. The remaining litigation risk usually centers on:

- Any still-protected method-of-use or formulation patents

- Combination product protections

- Manufacturing process claims that can affect “carve-out” of generic design freedom

Practical generic launch scenario for a mature product

- Generic entry is typically routine once relevant patents and exclusivity windows lapse.

- Market outcomes depend on whether new entrants drive pricing to the lowest-cost cohort or sustain a mid-market range if contracts favor authorized generics.

What FDA and Orange Book status items affect NORVASC market exclusivity?

Answer:

NORVASC’s FDA exclusivity is not the primary driver in the current market. Revenue persistence relies on whether specific listed patents in the Orange Book (for particular dosage forms/strengths or combinations) still block or delay certain generic designs.

How to interpret Orange Book status for revenue exposure

- If Orange Book lists only expired patents: generic entry risk is routine and price compression continues.

- If Orange Book lists active patents tied to particular strengths: generics may launch “at-risk” for unprotected strengths but wait on the protected ones, segmenting revenue impact.

(A definitive Orange Book matrix by strength and patent number cannot be compiled from the prompt alone.)

What combination and dosage-form mix strategies influence NORVASC financial trajectory?

Answer:

Dose-strength mix and combination therapy can moderate brand decline by preserving certain formulary positions and avoiding direct script competition in every segment simultaneously.

How does strength mix affect revenue?

- Brands often retain relative strength in strengths with:

- less aggressive rebate negotiation for that SKU

- higher refill persistence because patients tolerate the same dosage

- plan-level rules that prefer a particular strength for titration workflows

How do fixed-dose combinations change the competitive game?

- If NORVASC-linked FDCs are preferred, they can keep branded revenue alive even as monotherapy loses share.

- If payers prefer low-cost generic FDCs, the brand advantage erodes quickly.

How does NORVASC pricing and reimbursement pressure vary by region and payer segment?

Answer:

U.S. reimbursement is segmented by plan type: Medicaid, Medicare, commercial PBM contracts, and state-level purchasing rules. In each segment, net pricing depends on:

- rebate structures

- formulary status

- pharmacy benefit admin policies

What tends to happen when PBM contracts refresh?

- Brand script volume can drop immediately after a contract change.

- Generic volumes often rise and then stabilize as the lowest net-cost competitor cohort retains preferencing.

What is NORVASC’s profit and cash flow profile given mature brand dynamics?

Answer:

Amlodipine as a mature brand usually generates lower gross margin than during the branded peak due to rebate intensity and price compression, but it can still produce steady cash flow if:

- manufacturing is efficient

- channel inventory management is disciplined

- the company maintains access to high-persistence patient cohorts

Cost structure drivers

- COGS remains relatively low for an established oral solid dose

- SG&A and rebate costs rise as the brand fights for preferred placement

- Working capital swings can reflect inventory adjustments around contract cycles

How does NORVASC compare with other cardiovascular brands facing generic commoditization?

Answer:

NORVASC’s lifecycle economics mirror other off-patent oral cardiovascular products: revenue decline is mainly driven by net price compression and formulary displacement, while volume growth and persistence provide partial offset.

Benchmark pattern across classes

- Oral generics in statin-like and antihypertensive-like categories generally show:

- sharp post-generic revenue drops

- stabilization at lower revenue levels

- sporadic rebounds tied to contract wins or combination launches

Key Takeaways

- NORVASC’s current market dynamics are dominated by U.S. generic substitution and payer-driven net pricing, not by active exclusivity.

- Financial trajectory is best modeled as post-branded share loss followed by stabilization based on formulary access, strength mix, and combination therapy allocation.

- Generic entry risk exists primarily at the margin through any remaining patent-protected formulation, method-of-use, or combination line items, not the base amlodipine active ingredient.

- Near-term revenue outlook depends on PBM contract cycles, rebate intensity, and patient persistence in a dense competitive generic environment.

FAQs

- Does NORVASC have higher persistence than generic amlodipine after formulary switches?

- Which payer segments (commercial vs Medicare vs Medicaid) most affect NORVASC net price erosion?

- How do amlodipine strength-by-strength generic price differences influence NORVASC remaining market share?

- What combination products most influence amlodipine market share outcomes in mature hypertension therapy?

- How do contract-driven pharmacy channel inventory cycles create short-term NORVASC sell-in volatility?

References

- FDA. “Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations.” U.S. Food and Drug Administration. (Accessed via FDA Orange Book database).

- FDA. “Drug Trials Snapshots.” U.S. Food and Drug Administration. (Accessed via FDA database).

- IQVIA Institute for Human Data Science. “Medicines Use and Spending.” IQVIA. (Latest available annual report).

- Congressional Budget Office. “Prescription Drugs: Costs and Spending.” (background on reimbursement and market structure).