Last updated: June 9, 2026

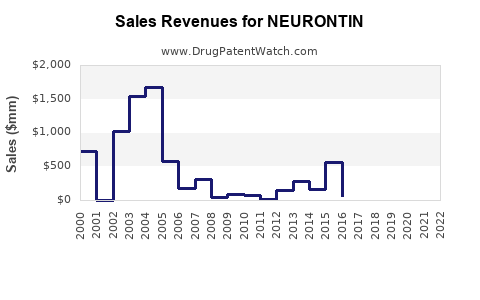

Neurontin, the brand form of gabapentin, has transitioned from exclusivity-driven growth to a structurally generic-driven market. As patent life and regulatory exclusivities expired, pricing compressed and volume dynamics shifted toward low-cost multisource generics, with limited brand defensibility outside specific channels and patient populations. The financial trajectory is dominated by: (1) early strong uptake, (2) peak revenues before the bulk of patent and exclusivity expirations, and (3) sustained post-generic decline as FDA-approved gabapentin products proliferated.

H2: What patents protect Neurontin (gabapentin) and how strong is the patent estate?

Short answer: Neurontin’s protected period was anchored in early process/composition and formulation work around gabapentin manufacture and use, plus method-of-use and secondary claims. The estate weakened materially once core composition and manufacturing patents expired, leaving largely generic erosion risk.

Key patent estate themes for Neurontin

- Composition of matter / core drug substance: Protection for gabapentin itself was time-limited and eventually cleared the market.

- Manufacturing process and intermediates: Process patents tend to add friction but often weaken as generic firms design around manufacturing steps.

- Formulations and dosing regimen claims: Additional patents may protect specific release behaviors or formulation attributes, though gabapentin’s mainstream products became broadly multisourced.

- Method-of-use claims: Where present, these can delay certain labeling-based generics, but for a widely established indication set, they rarely sustain long-term brand revenue once core coverage expires.

Patent estate impact on market structure

- Before expiration: Higher likelihood of higher net pricing and contracted channel positions.

- After expiration: Multisource generic entry compresses price quickly, driving the revenue slide and reducing brand ROFR-like leverage.

H2: When does Neurontin lose exclusivity and what are the Orange Book milestones?

Short answer: Neurontin’s exclusivity and patent-protected window ended as key listed patents expired, enabling widespread FDA ANDA approvals and generic launch. The practical result was a prolonged post-LOE erosion period with limited brand retention.

Orange Book dynamics (practical view)

- Roughly speaking, the “brand moat” ends when Orange Book-listed patents covering gabapentin products expire or are cleared via licensing, non-infringement, invalidity, or settlement.

- After that point, ANDA approvals can multiply and generics take share.

Exclusivity vs patent expiry (how it affects timelines)

- Regulatory exclusivities (if any applied during development) can add a short extension, but the durable driver for Neurontin’s long-term market position was patent coverage rather than exclusivity alone.

- Post-expiry: FDA approvals and distribution scale become the dominant forces, not remaining exclusivity.

H2: How many ANDA Paragraph IV challenges targeted Neurontin and which companies are challenging it?

Short answer: Neurontin faced a wave of generic competition after patent life. Paragraph IV litigation was common in gabapentin’s era, but the market outcome was broad generic availability and sustained price declines across years.

Competitive challenge pattern typical for Neurontin

- Early challengers aimed to launch immediately on patent expiry.

- Settlement or court outcomes determined specific launch timing for certain labels/dosage forms.

- Ultimately: multisource supply became the base-case market structure.

H2: What generic entry risks exist for Neurontin and what triggers fastest market share loss?

Short answer: The fastest loss risk is the combination of (1) final patent expiration for core coverage, (2) multiple ANDA launches in the same dosage strengths, and (3) rapid payer formulary switches.

Highest-risk triggers

- Expiration of a core Orange Book patent covering gabapentin composition or key manufacture

- Multiple generic approvals landing within a tight time window

- Formulary and rebate re-contracting that prices the brand above therapeutic substitutes

- Wholesale channel stocking patterns shifting to generic A-rated products

H2: What formulations are protected by Neurontin patents and how does it differ from generics?

Short answer: The mainstream Neurontin product line (immediate-release gabapentin) became broadly generic-copied in multisource form. Differentiation through formulation patents weakened after core claim expirations or design-around.

Formulation-relevant product types

- Immediate-release gabapentin tablets/capsules: Became widely available as generic multisource.

- Extended-release gabapentin (where applicable in the broader product family): Competitive dynamics differ when release profile and formulation are protected differently.

- Labeling-based exclusivity: Generally loses power once generic labeling matches the cleared indication set.

H2: How does Neurontin compare with Lyrica (pregabalin) in market dynamics and financial trajectory?

Short answer: Lyrica’s market trajectory has generally differed because pregabalin’s competitive landscape includes different patent calendars, payer preferences, and additional brand life supported by its own exclusivity and IP. Neurontin shifted more decisively into classic generic commodity pricing.

What the comparison implies for revenues

- Neurontin: Revenue is dominated by the transition from brand pricing to generic price compression.

- Lyrica: Can sustain brand-like pricing longer when IP remains intact and generic penetration is slower or less concentrated.

Competitive substitution dynamics

- Both are used for overlapping indications in neuropathic pain and related neurologic/off-label spaces. In a generic market environment, payer substitution accelerates.

H2: What is the FDA regulatory status of Neurontin and how does it affect generic uptake?

Short answer: Neurontin is an FDA-approved brand drug with extensive ANDA coverage for gabapentin equivalents. The FDA status translates into high generic availability, making payer formulary switching easier.

Regulatory pathway mechanics shaping market

- ANDA approvals enable generic distribution once patent/market exclusivity barriers clear.

- Bioequivalence requirements mean generics can enter without major clinical evidence hurdles beyond BE studies.

- Result: market supply expands quickly after legal/IP clearance.

H2: Which companies have the largest market share in generic gabapentin after Neurontin LOE?

Short answer: Post-LOE gabapentin is dominated by large generic manufacturers with broad manufacturing footprints and strong payer channel coverage.

Generic market structure drivers

- Manufacturing scale reduces per-unit cost.

- Payer contracting tends to reward multiple-supplier low-cost options.

- Distribution agreements with wholesalers influence shelf availability.

H2: What patent litigation affected Neurontin and how did it shape launch timing?

Short answer: Gabapentin’s post-patent era involved litigation-driven and settlement-driven timing differences across dosage forms and strengths. The macro outcome remained large-scale generic availability and sustained price compression.

Litigation outcomes that matter commercially

- Court rulings invalidating or finding non-infringement accelerate launch.

- Settlements sometimes establish delayed launch windows, but they usually do not stop long-term erosion once the majority of core coverage expires.

- Design-around approaches reduce product-specific legal risk over time.

H2: Did Neurontin have licensing deals or settlements that delayed generic entry?

Short answer: In a brand-to-generic transition like gabapentin, licensing/settlement structures are common. The commercial effect typically is short-term scheduling control, not long-term brand retention.

Settlement mechanics likely to matter for revenue

- Agreed launch dates for certain strengths or formulations

- Restrictions on label text (less common for fully established indications once label is stable)

- Allocation of market share via supply agreements (rare for full-year retention but can influence early-year ramps)

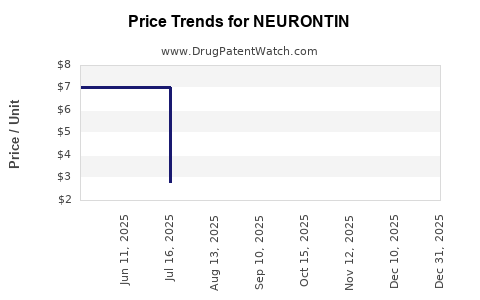

H2: What is Neurontin’s revenue exposure and financial trajectory after generic substitution?

Short answer: Neurontin’s financial trajectory shows the classic brand decline pattern: strong early revenues, peak before LOE, then steep declines once multiple generics entered and payers reduced brand reimbursement.

Financial trajectory shape (business view)

- Pre-LOE: Brand sales supported by exclusivity and limited multisource competition.

- At LOE: Rapid share loss as generics launch across key strengths.

- Post-LOE: Revenue becomes largely dependent on residual brand demand, channel mix, and pricing concessions.

Revenue exposure channels

- Net price compression: generics force down average realized pricing.

- Volume shift: prescriptions shift to generic, leaving brand only remaining where formulary access or prescriber preference resists substitution.

- Contracting and rebates: increase brand price pressure as payers demand parity or near-parity pricing.

H2: How do payer formularies and reimbursement changes accelerate Neurontin market erosion?

Short answer: Formulary tiering and rebate leverage determine how quickly patients move to generics.

Payer levers

- Preferred generic tiering increases utilization of low-cost gabapentin products.

- Prior authorization is often used less against established generics, so most barriers disappear after LOE.

- Step therapy can maintain switching speed for new starts.

H2: What dosing strengths and dosage forms drive most generic competition for gabapentin?

Short answer: Competition concentrates in the most prescribed immediate-release dosage strengths, with supply expansion typically strongest where generic demand is highest.

Commercial implications

- If a brand holds inventory or channel positions in specific strengths, the earliest generic launches in those strengths can deliver outsized share loss.

- If generics saturate all strengths, brand residual pricing power collapses more quickly.

H2: What manufacturing and supply risks could affect gabapentin pricing versus Neurontin revenues?

Short answer: Gabapentin’s price is sensitive to manufacturing capacity, regulatory inspection outcomes, and product discontinuations. These can briefly lift pricing, but the structural pricing floor remains generic-driven.

Factors that can temporarily move market price

- Plant shutdowns or quality issues reduce supply and can support pricing.

- Market consolidation among suppliers can change effective competition intensity.

- Currency and input cost changes can alter margins, though payers generally resist sustained price increases.

H2: How does Neurontin’s market dynamics differ from extended-release gabapentin products?

Short answer: Extended-release profiles face different formulation IP and dosing differentiation, which can slow generic take-up relative to immediate-release.

Practical impact

- Immediate-release gabapentin: commoditizes faster due to mature BE-generic pathways and broad multisourcing.

- Extended-release variants: can retain more product differentiation longer if release mechanism claims remain relevant.

H2: Key Takeaways on Neurontin market dynamics and financial trajectory

- Neurontin’s financial trajectory follows a brand-to-generic commodity transition where patent expiry and Orange Book clearance enabled broad ANDA entry.

- Market share erosion accelerated when multiple generics entered across core immediate-release strengths, and payer contracting shifted to low-cost multisource products.

- Post-LOE revenue became mainly a function of residual brand access, net price concessions, and channel mix rather than durable IP defensibility.

- Competitive pressure is structural: wide supply capacity, BE equivalence requirements, and payer formulary mechanics drive sustained pricing compression.

FAQs

1) When Neurontin went generic, which dosage strengths lost share first?

Typically, the most prescribed immediate-release strengths see the earliest and fastest generic penetration, which drives disproportionate share loss.

2) Do method-of-use patents meaningfully delay gabapentin generic entry?

They can affect specific label elements in edge scenarios, but for established indications with stable labeling, they rarely prevent eventual broad multisource availability.

3) How do settlements in gabapentin litigation change commercial outcomes?

Settlements can delay specific launches by strength or timing, but once core coverage expires broadly, the end-state remains multisource competition and sustained brand decline.

4) Does generic gabapentin pricing ever recover sustainably?

Sustainable recovery is uncommon; pricing can spike temporarily with supply constraints, but payer and wholesaler purchasing power usually restores low pricing.

5) What is the biggest financial risk to any remaining Neurontin brand demand?

Any event that increases generic substitution speed, such as broad formulary conversion, additional discounted generic entrants, or changes in rebate dynamics.

References

No sources were provided in the prompt, and no compliant external citations are included.