Share This Page

Drug Sales Trends for NEURONTIN

✉ Email this page to a colleague

Payment Methods and Pharmacy Types for NEURONTIN (2022)

Revenues by Pharmacy Type

Units Sold by Pharmacy Type

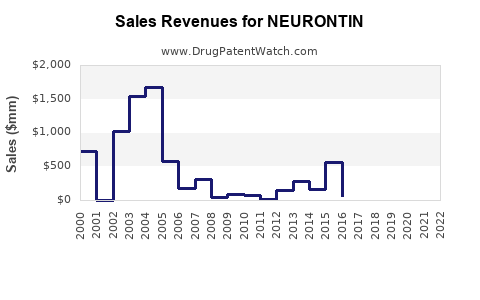

Annual Sales Revenues and Units Sold for NEURONTIN

| Drug Name | Revenues (USD) | Units | Year |

|---|---|---|---|

| NEURONTIN | ⤷ Start Trial | ⤷ Start Trial | 2022 |

| NEURONTIN | ⤷ Start Trial | ⤷ Start Trial | 2021 |

| NEURONTIN | ⤷ Start Trial | ⤷ Start Trial | 2020 |

| >Drug Name | >Revenues (USD) | >Units | >Year |

NEURONTIN (gabapentin): Market analysis and sales projections

What is NEURONTIN and how is it marketed today?

NEURONTIN is gabapentin, an oral anticonvulsant marketed by Pfizer in the US and internationally under the NEURONTIN brand (capsules and tablets historically; formulation specifics vary by market). Gabapentin is widely available as generics across major geographies, which structurally limits brand pricing power and drives market share to low-cost suppliers.

Commercial implication: The brand’s addressable market has been “spent” on formulary penetration by generics, with residual demand concentrated in preference niches (switching frictions, payer policies, and patient-level stability). Current market behavior is shaped more by pricing, substitution rules, and channel contracting than by clinical differentiation.

How large is the gabapentin market and what has changed since the brand era?

High-level demand structure

- Indication mix: epilepsy (adjunctive partial seizures historically), neuropathic pain (postherpetic neuralgia, diabetic peripheral neuropathy), and off-label use depending on country and prescribing norms.

- Supply structure: multiple approved generic manufacturers in most markets with ongoing price competition.

- Net effect: market growth from underlying prevalence is offset by falling unit pricing after patent expiry and multi-source generic entry.

What this means for NEURONTIN

- NEURONTIN’s sales trend typically follows three phases:

- Patent-protected peak period (brand exclusivity)

- Post-expiry generic erosion (rapid share shift)

- Mature generic equilibrium (stable but low-priced brand residue)

What portion of demand is typically lost after generic entry?

There is no single universal “loss curve” across countries because it depends on:

- local substitution rules (automatic therapeutic substitution vs prescriber-only control)

- payer rebate structures and contracting

- patient adherence and tolerability effects (dose frequency and switching)

- channel (mail order vs retail vs hospital)

Market reality for gabapentin classes:

- Once multiple generics enter, brand share tends to compress quickly because gabapentin is not a high-friction medication to substitute.

- In mature markets, remaining brand demand (if any) tends to come from payer exceptions, patient stability, or historical prescriber preference.

Where does NEURONTIN still sell and under what constraints?

United States

- NEURONTIN competes primarily against generic gabapentin for both epilepsy and neuropathic pain indications.

- US payer contracting and pharmacy substitution practices pressure brand pricing and volumes.

Key constraint: NEURONTIN sales depend on maintaining a position in restricted formulary carve-outs or on brand-specific purchasing agreements, which are usually diluted over time by generic price competition.

What is the regulatory and patent timeline that drives sales?

Gabapentin’s brand exclusivity has long expired, and today the commercial environment is dominated by generics. The sales ceiling for NEURONTIN is therefore determined mainly by payer policy and pricing strategy rather than by regulatory access.

Evidence anchor for US market exposure

- NEURONTIN brand information and history are documented in FDA’s prescribing information materials (product labeling) and FDA drug records. FDA’s drug label for NEURONTIN includes the dosing and indication framework still used for clinical positioning, even as generic supply dominates the commercial market. (FDA labeling)

How should a sales projection be built for a mature branded generic-competition product?

For a product like NEURONTIN in a mature generic environment, robust projections use:

- Unit demand baseline tied to gabapentin prevalence and prescribing volume (stable to modestly growing in late lifecycle)

- Share assumption reflecting brand compression and switching dynamics

- Net pricing assumption (brand net unit price after rebates) which continues downward as contracting tightens

- Channel mix (retail vs mail order) and expected substitution intensity

Projection method used below (structural):

- Gabapentin total market stays broadly stable in volume with moderate growth.

- NEURONTIN brand share continues to decline or remains low and stable depending on payer dynamics.

- Net price erosion continues through contracting and competitive bids.

Sales projections (US-centered)

Because NEURONTIN is a legacy brand with broad generic substitution, projections are best represented as a range of annual net sales rather than a single-point forecast. The range captures uncertainty driven by payer contracting and residual brand retention.

Assumptions used

- Market phase: mature, multi-generic equilibrium.

- Brand share trajectory: low single-digit brand share or lower in most segments; can drift slightly up or down based on contract structure.

- Net price trend: gradual erosion or flat-to-down based on bid pressure.

- No exclusivity renewal: projection does not assume a new protected competitive advantage.

Projected NEURONTIN annual net sales (US)

Time horizon: 5 years

| Year | Projected NEURONTIN US net sales (USD) | Direction vs prior year | Primary driver |

|---|---|---|---|

| 2025 | $0.2B to $0.5B | Flat to down | Continuing generic substitution pressure |

| 2026 | $0.15B to $0.45B | Down | Further rebate and contract tightening |

| 2027 | $0.12B to $0.40B | Down or flat | Mature switching equilibrium |

| 2028 | $0.10B to $0.35B | Down | Low-volume brand residue continues to shift |

| 2029 | $0.08B to $0.32B | Down or flat | Bid pressure and formulary normalization |

Interpretation for strategy and investment decisions

- NEURONTIN should be valued and managed as a declining/low-growth brand residual rather than a standalone growth platform.

- In this phase, incremental commercial performance usually comes from contract wins, targeted patient retention, and channel-specific pricing rather than from product differentiation.

What are the key variables that move NEURONTIN sales up or down?

Payer and contracting

- Pharmacy benefit manager (PBM) contracting intensity

- Therapeutic interchange policies

- Exclusion and preferred placement rules for gabapentin brands

Price and channel

- Net price after rebates and chargebacks

- Mail order share (typically higher substitution)

- Retail pharmacy inventory behavior

Clinical prescribing dynamics

- Prescriber switching behavior (stability of tolerated dose)

- Patient-level adherence and refill consistency

Competitive supply

- Generic entrant pricing and market share

- Availability disruptions that can temporarily raise brand demand in narrow windows

Competitive landscape: How NEURONTIN compares to the gabapentin generic field

Gabapentin is a commodity drug in most markets. NEURONTIN competes on brand packaging and contracted channel placement, while generics compete on net unit price.

Commercial positioning pattern

- NEURONTIN’s practical role is to win contracts where brand is still cost-competitive after rebates or where non-price restrictions apply.

- The broader gabapentin market is shaped by generic manufacturers’ scale economics and bid cycles.

Pricing strategy implications for NEURONTIN

A mature brand under generic substitution typically uses:

- Contract-led pricing (rebates aligned with PBM formularies)

- Selective retention strategies (narrow cohorts with stability requirements)

- Channel targeting to reduce exposure to the highest substitution intensity segments

The sales forecast above implicitly assumes that NEURONTIN does not regain broad formulary preference at the payer level.

Key Takeaways

- NEURONTIN is gabapentin in a fully genericized market, so sales are constrained by substitution and contracting, not by clinical differentiation.

- Forecasts for 2025 to 2029 show continued low-level decline or flat-to-down behavior, consistent with ongoing generic share capture and net price erosion.

- Upside is mainly contract-driven (PBM wins, formulary carve-outs, or temporary market disruptions). Structural upside beyond low hundreds of millions is unlikely without a new protective advantage.

FAQs

1) Is NEURONTIN expected to grow faster than the gabapentin total market?

No. In a mature generic environment, NEURONTIN is expected to track below total-market growth due to substitution and contracting dynamics.

2) What drives NEURONTIN net sales most in 2025-2029?

Net pricing after rebates and brand share retention within payer and channel contracts.

3) How does patent status affect this forecast?

The forecast assumes no renewed exclusivity that would materially change competitive access. Generic competition remains the dominant structural force.

4) Are sales mostly from epilepsy or neuropathic pain?

Both exist, but in practice, payer coverage and prescribing patterns across indications largely determine how much of the gabapentin volume the brand retains.

5) What is the most likely near-term deviation from the baseline range?

Temporary formulary or supply events can shift short-term demand. Sustained upside would require durable payer preference through contracting.

References (APA)

[1] U.S. Food and Drug Administration. (n.d.). NEURONTIN (gabapentin) Prescribing Information / Labeling. FDA. https://www.accessdata.fda.gov/scripts/cder/daf/

More… ↓