Last updated: April 23, 2026

MILOPHENE: Market Dynamics and Financial Trajectory

What is MILOPHENE and what market is it in?

MILOPHENE is a brand name for mitotane (o,p’-DDD), an adrenocortical carcinoma (ACC) therapy. The drug is positioned in oncology, but commercially it is constrained by the narrow ACC population and by the realities of generic and specialty supply. Its market dynamics are driven less by broad payer pull-through and more by: (1) oncology center prescribing patterns, (2) specialty pharmacy access, and (3) supply continuity in a mature, older molecule category.

Regulatory footprint

- Indication (US): Adjuvant treatment after surgery for ACC in adults (label history varies by revision cycle), and treatment of advanced ACC where applicable by label.

- Regimen profile: Chronic dosing with therapeutic drug monitoring (TDM), which raises retention and switching barriers but also increases provider friction at the point of care.

How does the drug’s demand profile behave?

MILOPHENE’s demand is structurally inelastic: ACC incidence is limited, and therapy is typically used under specialized supervision with TDM. That combination tends to produce:

- Stable baseline volume tied to new patient flow rather than broad epidemiology.

- Lumpy purchasing around treatment starts and supply replenishment for specialty channels.

- Lower brand competition risk versus high-incidence oncology assets, but higher supply and discontinuation risk because older molecules can be deprioritized or cycled through manufacturing capacity.

Where does pricing power come from?

Pricing power for mitotane brands is constrained by:

- Specialty/generic pressure: mitotane is widely available in many markets as older generics or equivalents, which compresses achievable net price.

- Provider-led switching: TDM requirements lower tolerance for product variability and can slow switching, but once equivalence is accepted, payers do not sustain premium pricing for long.

Net effect: the revenue trajectory is typically dominated by net-to-gross erosion and channel mix rather than by demand growth.

What market dynamics drive revenue for MILOPHENE?

1) ACC epidemiology sets the ceiling

ACC remains a rare cancer. That makes revenue growth contingent on:

- treatment penetration (adjuvant vs metastatic use),

- regional prescribing behavior, and

- product availability (avoiding shortages that interrupt therapy).

This creates a market where top-line momentum is capped unless there is a step-change in clinical practice.

2) Specialty channel economics determine net revenue

MILOPHENE’s revenue is largely realized through:

- hospital and specialty pharmacy workflows,

- payer authorization rules for ACC therapies,

- contracting and rebate structures that can materially reduce net price.

If supply remains steady and the drug maintains formulary positions in ACC care pathways, revenue stays stable. If supply deteriorates or contracts worsen, revenue can drop quickly because ACC patients do not have substitute time.

3) Supply continuity can swing quarterly sales

Mitotane supply can be affected by manufacturing continuity and compounding/packaging constraints that are common for older oncology molecules. For brand performance, the key commercial variable is:

- whether customers experience backorders or lead-time increases, which forces holds on new starts and can displace patients temporarily.

4) Clinical monitoring reduces switching but does not prevent erosion

TDM and dose titration reduce the speed at which clinicians switch products, protecting utilization once established. But it does not stop:

- payer reimbursement pressure,

- conversion to lower-priced equivalents, or

- formulary redesign by health systems seeking cost control.

Financial trajectory: what pattern does revenue follow?

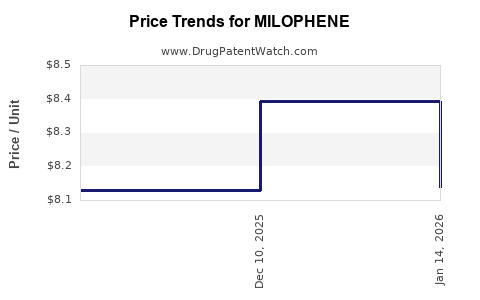

MILOPHENE’s financial trajectory is typically characterized by late-life stability with pricing compression, not high-growth expansion. The expected trajectory in a mature mitotane market is:

- Early brand phase: higher net price, tighter supply stability, payer acceptance lag.

- Mid-life: gradual net price compression from contracting and equivalent competition.

- Late phase: revenue becomes volume-stable but net revenue follows pricing and contract renegotiation cycles, with periodic disruptions tied to supply.

For investors and planners, the practical takeaway is that growth is unlikely to come from new indications or scale economics; it comes from contract win-loss, supply reliability, and incremental penetration in specialty networks.

How sensitive is MILOPHENE financial performance to payer and contracting cycles?

Mitotane’s revenue is sensitive to payer dynamics because:

- ACC is rare, so formulary placements determine share.

- Contracting changes can shift patients between available equivalents.

- Specialty pharmacy procurement and prior authorization rules influence uptake speed.

The financial sensitivity shows up as:

- modest changes in utilization producing disproportionate swings in net revenue if net price moves at the same time, or

- stable utilization masking underlying net-to-gross deterioration.

What are the main competitive forces?

Direct competition

- Other mitotane formulations/equivalents in the same therapeutic category.

Indirect competition

- alternative ACC management strategies (surgery timing, systemic oncology regimens, or clinical pathways that delay mitotane)

- emerging ACC research does not replace mitotane quickly in routine practice, but it can influence center preferences over time.

Net: MILOPHENE competes mainly on availability and reimbursement, not on differentiated clinical efficacy.

What does this imply for near-term revenue risk?

The core near-term risks for MILOPHENE revenue are:

- pricing compression driven by contracting and equivalent availability,

- supply interruption affecting treatment starts,

- formulary changes in high-volume oncology systems.

The mitigating factors are:

- TDM-based practice patterns that reduce frequent switching, and

- specialty physician retention when a product meets monitoring and dosing continuity needs.

Key Takeaways

- MILOPHENE (mitotane) is an ACC-only oncology therapy with an inelastic, rare-disease demand profile, so revenue growth depends on penetration and access more than market expansion.

- The drug’s financial trajectory is typically stable volume with net price compression, driven by payer contracting and equivalence competition.

- The biggest short-cycle driver of financial outcomes is supply continuity in specialty channels, since ACC treatment starts are difficult to interrupt.

- Near-term performance risk concentrates in pricing and supply, not in clinical obsolescence.

FAQs

-

Is MILOPHENE expected to grow like a high-incidence oncology drug?

No. ACC incidence limits ceiling growth; performance hinges on access, contracting, and supply continuity.

-

Does therapeutic drug monitoring protect MILOPHENE revenue?

It slows switching and can support retention, but it does not prevent net price erosion from payer contracting and equivalents.

-

What drives quarter-to-quarter volatility for MILOPHENE?

Specialty channel ordering, contracting shifts, and any supply or lead-time disruption.

-

Where is the main competitive pressure for MILOPHENE?

Mitotane equivalents and formulations that compress net pricing through formulary and contracting.

-

What is the most important metric for MILOPHENE commercial planning?

Net revenue performance after contracting (net-to-gross) combined with service-level reliability in specialty distribution.

References

[1] U.S. Food and Drug Administration. Drug Label (mitotane-containing product information; label revisions and indication language).

[2] National Cancer Institute. Adrenocortical Carcinoma (ACC) overview and treatment context.

[3] FDA Orange Book. Mitotane listings and approved drug products/therapeutic equivalents.