Last updated: April 24, 2026

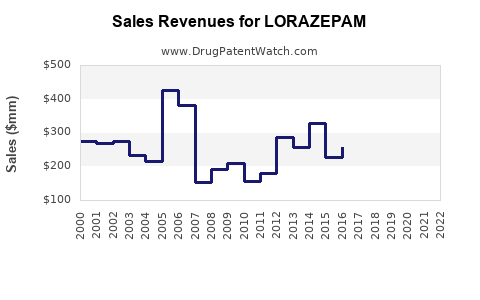

Lorazepam is a long-standing, generic-heavy benzodiazepine with stable but mature demand, pricing pressure from generics, and periodic substitution dynamics driven by formulary preferences, patent-to-generic transitions, and controlled-substance scheduling enforcement. The financial trajectory is characterized by (1) premium pricing during brand exclusivity, (2) steep revenue erosion after generic entry, (3) ongoing volume resilience, and (4) periodic margin pressure tied to reimbursement and competition in oral solid formats.

What is lorazepam’s market position and demand profile?

Lorazepam is widely used for anxiety disorders, short-term management of insomnia, and as premedication/sedation in clinical settings. In practice, demand is supported by chronic prescriber adoption, broad insurance coverage, and multi-source availability (tablets and concentrates).

Market position (commercial reality)

- Drug class: benzodiazepine anxiolytic, sedative

- Regulatory status: marketed as a controlled substance in the U.S. (schedule depends on jurisdiction and product category; lorazepam is typically Schedule IV in the U.S.)

- Competition structure: predominantly generic after brand exclusivity periods for earlier-origin products

- Procurement channel: retail pharmacy is the dominant distribution channel; hospital and institutional usage exists through oral and injectable supply chains

Demand drivers

- Clinical habit and switching costs: prescribers often maintain continuity on an effective benzodiazepine regimen when tolerability and dosing align.

- Formulary placement: generic lorazepam is commonly treated as a low-cost option, improving access but compressing net pricing.

- Controlled-substance compliance: dispensing limits, monitoring requirements, and payer utilization management can shift demand at the margin, but they rarely eliminate the drug class at population level.

Evidence of long-run drug utilization

- Lorazepam has a long history as an approved benzodiazepine in the U.S.; the label is distributed widely through generic manufacturers and consolidated branded label references. The FDA’s drug labeling and historical approval records support the drug’s established presence in the market. [1]

How do market dynamics shape pricing and share?

Lorazepam’s commercial dynamics are less about innovation and more about competition mechanics and payor contracting.

Generics and price compression

After a branded origin product loses exclusivity, generic entry drives:

- faster price declines versus branded-only eras,

- higher market share by lowest net price,

- margin dilution across manufacturers.

This is typical for small-molecule CNS drugs once multiple Abbreviated New Drug Applications (ANDAs) enter with comparable bioequivalence. FDA’s ANDA framework explains the generics pathway. [2]

Reimbursement and net price mechanics

In a mature generic market, “list price” is a poor indicator of realized revenue:

- net price depends on pharmacy benefit manager (PBM) contracting, rebates, and preferred status,

- state Medicaid formularies and federal covered programs tend to favor cost-effective multisource products.

Switching and treatment persistence

Benzodiazepines have high real-world persistence when patients tolerate dosing, but they also face discontinuation pressures:

- clinical practice often favors shorter-term use for new prescriptions,

- risk management around dependence and sedation can reduce new starts in some populations, shifting demand toward established patients.

This dynamic slows growth but supports volume stability, which matters because volume resilience is the principal defense against pricing erosion.

What is the financial trajectory from brand-era to generic-era?

Lorazepam’s financial trajectory follows the classic mature CNS pattern:

- Brand-era monetization

- Premium pricing supported by exclusivity and limited competition.

- Post-exclusivity erosion

- Revenue falls as generics take share.

- Volume stabilization

- Demand remains because the drug is embedded in clinical practice.

- Long-run margin pressure

- Net pricing declines and competition becomes a cost-and-contract battle.

Key structural characteristics of the trajectory

- Revenue volatility is low relative to oncology or specialty products because demand is driven by ongoing utilization rather than episodic approvals.

- Gross margin compresses as more manufacturers compete and PBMs push the formulary toward the lowest net price.

- Portfolio strategy tends to focus on supply reliability, manufacturing scale, and contract execution rather than differentiated clinical claims.

How do controlled-substance enforcement and risk management affect sales?

Lorazepam’s status as a controlled substance influences dispensing behavior and payer management:

- pharmacies face additional compliance controls,

- clinicians implement risk screening and monitoring,

- payers can require utilization management (step edits, quantity limits) in some plans.

These factors can reduce new patient initiation and can shift demand to alternative agents within the class. However, they do not typically eliminate the existing use base quickly due to established prescribing patterns and the drug’s therapeutic role.

What are the main competitive forces in lorazepam?

Multi-source generic manufacturing

Lorazepam’s competitive set includes multiple generic manufacturers and authorized labelers. Competitive outcomes depend on:

- supply continuity and plant capacity,

- ability to meet market demand without price concessions,

- contract performance with PBMs and large payers.

Therapeutic class substitution

Within benzodiazepines and across anxiolytics/sedatives, substitutions include:

- other benzodiazepines,

- non-benzodiazepine alternatives depending on indication and payer preferences.

Switching is constrained by dosing equivalence, clinician familiarity, and patient tolerability, which tends to protect volume but not pricing.

Short-term cycle effects

Even in mature products, pricing can fluctuate with:

- temporary supply disruptions,

- contract renewals,

- regional pharmacy purchasing shifts.

The U.S. drug supply and labeling ecosystem is shaped by FDA’s drug approval and postmarket compliance frameworks. [1][2]

Where do the strongest revenue pools typically sit?

For a mature generic like lorazepam, revenue is concentrated in:

- oral solid dose forms (tablets) where dispensing volumes are highest,

- short-stay institutional settings where sedative and premedication uses occur,

- patients already stabilized on a regimen where persistence dominates over switching.

Injectable formulations exist for certain indications and institutional protocols, but the dominant commercial engine in most markets remains tablets and commonly dispensed dosage strengths.

What timeline milestones matter for commercialization?

Lorazepam is not a “new” molecule, so the meaningful commercialization milestones are not brand approvals but rather:

- original regulatory approvals and label establishment,

- ongoing generic entry under ANDA pathways,

- periods where exclusivity or branded residual supply created temporary pricing support,

- changes in controlled-substance enforcement and labeling that affect prescribing behavior.

FDA’s drug labeling repository is a core reference point for approved indications, dosing, and labeling history. [1]

How does the lorazepam market compare with other benzodiazepines?

Lorazepam competes across:

- diazepam (longer half-life, different clinical fit),

- clonazepam (seizure overlap and anxiolytic indications),

- alprazolam (anxiety focus, different controlled substance dynamics),

- temazepam and others depending on sleep indications.

In mature markets, the differentiator is rarely efficacy because class effect drives prescribing; the differentiator is net price, availability, and formulary preference. That places lorazepam in a stable but price-capped position.

What does the financial trajectory imply for investors and R&D strategists?

For investors

- Expectation: steady demand with declining or flat margins.

- Risk: margin erosion from competitive generic pricing and PBM contracting.

- Upside: only arises through manufacturing scale, contract wins, or supply constraints that temporarily improve net pricing.

For R&D strategists

- Innovation thesis must be differentiated if the goal is to escape generic pricing.

- If pursuing new product development in the same clinical space, the commercial path must address either:

- differentiation that changes prescribing behavior enough to win formulary access at premium pricing, or

- a niche delivery format with a demonstrable access advantage.

Market outlook: what is likely to happen next?

Lorazepam is expected to remain a stable volume product in a generic-dominated landscape, with:

- continued downward pressure on net pricing,

- periodic contract-driven shifts in share among generic competitors,

- demand impacts tied to broader benzodiazepine prescribing trends and safety management policies.

No single structural change (such as a new monopoly) is typically available in a molecule this mature, so the financial path is mostly “micro-competitive” rather than “macro-innovative.”

Key Takeaways

- Lorazepam is a mature, generic-heavy benzodiazepine with stable demand supported by established clinical use and broad access.

- Financial performance is dominated by generics-driven net price compression and PBM/formulary contracting mechanics.

- Controlled-substance risk management influences new starts and utilization controls, limiting upside but supporting long-run volume resilience.

- Competitive advantage in this market tends to come from manufacturing reliability and contract execution, not product differentiation.

FAQs

1) Is lorazepam primarily a brand or generic market?

It is primarily a generic market, with competition among multiple ANDA-labeled manufacturers after origin-brand exclusivity periods. [2]

2) What drives lorazepam’s revenue in a mature lifecycle?

Realized revenue tracks with net pricing under payer contracting and volume persistence among existing patients. List price is less informative than PBM and plan-specific net economics.

3) How does controlled-substance regulation affect sales?

It can reduce new initiation rates and can trigger payer and dispensing controls, which generally limits growth but does not typically eliminate demand for stabilized patients.

4) What matters most competitively for generic lorazepam manufacturers?

Supply continuity, manufacturing scale, and contract placement with PBMs and major payers drive outcomes because clinical differentiation is limited.

5) Where does lorazepam typically generate most commercial value?

Oral tablet formulations usually generate the bulk of retail and outpatient volume; institutional use exists but is smaller relative to outpatient dispensing.

References

[1] U.S. Food and Drug Administration. Lorazepam prescribing information and drug labeling resources. https://www.fda.gov/drugs/drug-approvals-and-databases

[2] U.S. Food and Drug Administration. Abbreviated New Drug Application (ANDA) pathway and generic drug approval framework. https://www.fda.gov/drugs/abbreviated-new-drug-application-anda