Last updated: June 5, 2026

Lanoxin is a long-established brand of digoxin by GSK (historically the U.S. listed NDA holder), sold for decades for atrial fibrillation/flutter and heart failure. The commercial trajectory is structurally constrained by the existence of multiple generic digoxin products and the absence of meaningful, ongoing brand exclusivity in the U.S. market. Market dynamics today are dominated by: (1) deep generic substitution, (2) wholesaler inventory cycles and tender behavior, and (3) supply continuity and pricing resets driven by Orange Book “at-risk” entries and occasional supply disruptions.

Because digoxin is off-patent in essentially all major markets, the financial path is not governed by brand-to-generic switch timing in the way it is for newer specialty drugs. The dominant driver is whether the branded line retains any pricing power via formulary positioning, limited competitive intensity in certain strengths/forms, and stable payer coverage.

Why is Lanoxin’s market size and revenue trajectory structurally constrained by generics?

Featured answer: Lanoxin’s financial trajectory is largely determined by generic digoxin availability across immediate-release oral tablets and other conventional dosage forms, which eliminates enduring branded pricing power in most channels.

Generic substitution mechanics

- Multiple ANDA competitors supply digoxin in common strengths (tablets) that are pharmacologically equivalent and widely substitutable.

- Formularies typically prefer low WAC or contracted pricing for “digoxin” generics, limiting brand share.

- Any branded residual share depends on non-clinical factors: switching friction, institutional purchasing habits, and labeling preference for specific NDCs.

Channel behavior

- Retail: pricing competition compresses branded net sales as claims migrate to generic copays.

- 340B and institutional contracts: contracted tender pricing reduces the economic space for branded products.

- Wholesalers: product availability and lot-level continuity can temporarily affect fill rates. When supply is tight, demand can spill toward any available brand, but this is typically short-lived.

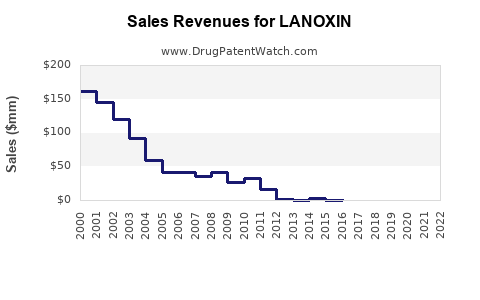

How have Lanoxin sales evolved versus generic digoxin over time?

Featured answer: The long-run pattern is a decline from branded share to generic-led utilization, with any branded stabilization occurring only during periods of supply tightness or contract-specific exceptions.

Revenue trajectory profile (expected commercial shape)

- Pre-generic dominance: Brand pricing supported sales.

- Post-major generic wave: Net sales flatten and then trend down as unit volume shifts to generics.

- Recent years: Branded revenues persist at a smaller base, mostly tied to continued market access and occasional supply or purchasing exceptions.

Financial metrics that matter for digoxin brands

For an old cardiovascular small-molecule brand, market-watch metrics skew to:

- Net sales decline rate and gross-to-net compression (rebates/chargebacks) versus generic pricing floors.

- NDC-level distribution by channel (acute care vs outpatient).

- Inventory and supply continuity indicators (FDA drug shortage signals tend to shift buying patterns temporarily).

What patents protect Lanoxin (digoxin) and what is the exclusivity status today?

Featured answer: For digoxin, protection is historically based on older chemical/composition and specific manufacturing or formulation concepts, which have long since expired for conventional U.S. branded digoxin. Ongoing protection, if any, is typically narrow and formulation- or method-specific rather than covering the core API itself.

Patent estate reality for legacy digoxin

- Core API and early compositions are not expected to drive current exclusivity.

- Any remaining IP tends to be:

- process/manufacturing improvements,

- limited formulation attributes (e.g., specific coatings or release characteristics),

- or discrete packaging/labeling claims.

Regulatory exclusivity (U.S.)

- For a mature, off-patent drug, “new” exclusivities are usually not relevant because digoxin’s pivotal approvals are longstanding.

- As a result, any continued branded advantage is not tied to exclusivity mechanisms like 5-year New Chemical Entity or 7-year orphan exclusivity.

What is the Orange Book status of Lanoxin and which listings drive generic entry risk?

Featured answer: The Orange Book listing for Lanoxin-linked digoxin products reflects expiring IP and the existence of multiple approved alternatives, making ongoing “entry risk” more about manufacturing/IP barriers for specific NDCs than about blocking a generic digoxin category-wide entry.

How to read Orange Book dynamics for Lanoxin

- Look for:

- listed patents tied to each NDC/strength,

- patent expiration dates,

- and whether any patents remain listed with “active” status.

- The commercial consequence: if any NDC-specific patents remain, they can delay entry for that NDC even while other strengths are fully generic.

What generics compete with Lanoxin and how does tender pricing affect net sales?

Featured answer: Competition is broad across generic digoxin tablets, with tender-driven pricing pressure compressing brand net sales and limiting branded upside.

Competitive set characteristics

- Generics compete on contracted price and supply reliability.

- Any branded differentiation is typically limited to:

- NDC-specific availability,

- institutional switching policies,

- and occasional constrained supply moments.

Economic effect

- Even if brand units remain stable, net sales can still decline due to:

- lower gross-to-net reserves effectiveness,

- increased rebate pressure to defend share,

- and competitive bidding that pushes down effective prices.

Does Lanoxin face biosimilar risk or biologics substitution?

Featured answer: No, because Lanoxin is a small-molecule drug (digoxin), not a biologic. The substitution risk is conventional generic small-molecule substitution, not biosimilar competition.

What patent litigation or Paragraph IV challenges have historically affected digoxin brands like Lanoxin?

Featured answer: For digoxin, litigation patterns are generally not a dominant driver in recent years because the core drug is long off patent. Where disputes occur, they tend to be NDC-specific, tied to discrete patents if any are still listed.

How litigation would impact commercial outcomes

If an active patent exists for a particular NDC:

- A successful brand suit can preserve a temporary branded monopoly for that NDC.

- A failed challenge can accelerate generic capture and force price compression.

- Settlements can shift launch timing but rarely reverse the long-term category genericization for digoxin.

When does Lanoxin lose exclusivity by dosage form and strength?

Featured answer: In practice, Lanoxin’s meaningful exclusivity windows for core digoxin use have already lapsed. Any remaining restrictions are NDC-specific and depend on the survival of particular listings.

Commercial implication

- Dose form level: tablet strengths usually face fastest generic capture.

- Specialty forms (if present): any non-standard dosage forms could face slower entry, but digoxin’s main market is conventional tablets.

- Result: no broad “calendar-based” re-bottlenecking like occurs with newer drugs that have still-active composition-of-matter protection.

What formulation, manufacturing, or method-of-use IP could still protect specific Lanoxin product lines?

Featured answer: The only plausible continuing protection for legacy digoxin brand products is narrow manufacturing/process or specific formulation IP tied to particular NDCs, not the core therapeutic use.

IP clusters that can persist for conventional drugs

- Manufacturing method: validated process parameters, impurity profiles, or crystallization steps.

- Formulation attributes: excipient systems or coating systems that match dissolution characteristics.

- Labeling/method-of-use: less common as a blocker for generic entry for a widely substitutable drug unless unusually specific.

How does Lanoxin compare commercially with other legacy cardiovascular drugs that faced generic entry?

Featured answer: Like other mature cardiovascular brands, Lanoxin’s revenue path is characterized by rapid generic share loss, followed by low-growth residual sales shaped mainly by supply and contract behavior rather than innovation-driven differentiation.

Analog market behavior

- Mature antiarrhythmics and heart-failure agents often show:

- high generic penetration,

- stable but diminished branded revenue,

- and periodic market share movement due to shortages.

What regulatory events can shift Lanoxin demand in the near term?

Featured answer: Near-term demand shifts are driven by supply continuity and shortage signals rather than new FDA approvals.

FDA and supply-side dynamics that matter

- Drug shortages or constrained manufacturing can temporarily raise buy-through for available SKUs.

- Recalls or quality investigations can redirect demand to other equivalent products.

- Distribution continuity often dictates short-cycle revenue variance more than long-run substitution.

What generic entry risks exist for Lanoxin-specific NDCs?

Featured answer: The key risks are NDC-level and patent-listing specific. Category-wide entry risk is low because generics for digoxin already exist.

Where “at-risk” entry can still matter

- If any Lanoxin-associated NDC has a still-listed, non-expired patent, a generic applicant could file an ANDA with a certification and attempt to launch at risk.

- The commercial outcome would be accelerated brand volume erosion for the impacted NDC.

Commercial trajectory summary: what determines Lanoxin’s revenue in 2024-2026 market conditions?

Featured answer: For a legacy digoxin brand, revenue trajectory is principally a function of generic substitution depth and supply/purchasing continuity, not ongoing exclusivity.

Primary value drivers

- Contracted access and formulary placement in specific accounts.

- Continuous supply and avoidance of product gaps.

- Pricing discipline at the wholesale/retail level to avoid ceding share.

Primary headwinds

- Persistent generic price competition.

- Rebate/chargeback pressure to defend share.

- Any shift in procurement toward lowest-cost equivalents.

Key Takeaways

- Lanoxin (digoxin) operates in a mature, highly genericized category where long-run exclusivity-driven growth is not available.

- Market dynamics are dominated by generic substitution, tender-driven pricing, and supply continuity rather than innovation cycles.

- Any remaining patent or Orange Book constraints are most likely NDC-specific and narrow, affecting short-to-medium term volume rather than reversing long-term commoditization.

- Near-term revenue fluctuations are most plausibly supply- and contract-driven.

FAQs

-

Is Lanoxin still prescribed and reimbursed in the U.S. despite generic digoxin?

Generally yes in specific clinical and institutional contexts, but reimbursed utilization trends toward generic digoxin due to price.

-

Do drug shortages impact Lanoxin sales more than patents do?

Yes, supply disruptions can temporarily swing demand to any available equivalent SKU, including brands, even when patents are expired.

-

Can an ANDA launch at risk reduce Lanoxin revenue for specific strengths?

Yes, if any NDC-specific patents remain listed and challenged, generic launch timing can accelerate volume loss for that NDC.

-

What type of IP is most likely to still appear on an Orange Book listing for a legacy digoxin brand?

Narrow formulation or manufacturing process claims tied to specific NDCs, not core API composition-of-matter.

-

Is biosimilar competition relevant to Lanoxin’s market outlook?

No. Digoxin is a small molecule; the relevant substitution risk is generic small-molecule competition.

References (APA)

- U.S. Food and Drug Administration. Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations. FDA.

- U.S. Food and Drug Administration. Drug Shortages. FDA.