Last updated: April 22, 2026

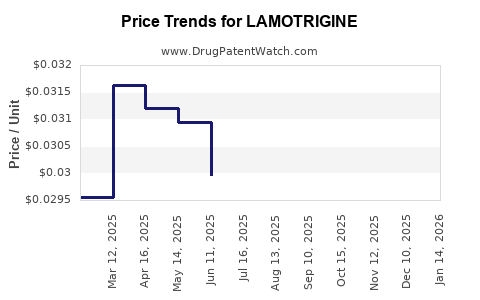

Lamotrigine is a long-established, small-molecule antiepileptic drug whose commercial trajectory is dominated by (1) broad generic penetration in major markets, (2) episodic payer and formulary pressure, and (3) off-patent portfolio dynamics across CNS brands in the US and EU. Financial performance is therefore less a function of innovation and more a function of pricing resets, tendering, and volume retention versus competing generic supply. Brand-level revenue exists, but overall market economics are primarily “price-volume,” with thin margins for wholesalers and sustained margin compression over time.

How has lamotrigine’s market structure evolved since it became generic?

Lamotrigine is widely available as generics globally. In the US, the originator is under brand-like commercialization historically, but the active market today is overwhelmingly generic. That structure drives several persistent market dynamics:

- Generic-led price competition: Once multiple abbreviated new drug applications (ANDAs) are approved, each subsequent entrant tends to reduce net pricing through competitive bidding, rebates, and payer contracting.

- Formulary status is a volume determinant: In US managed care, formulary tier placement and prior authorization rules determine prescription share more than brand differentiation.

- Switching behavior: Patients and prescribers can be sensitive to small changes in formulation and dosing delivery, which can slow switching in some settings. In practice, that creates short-run stability for incumbent generic SKUs, followed by further share dilution as additional manufacturers price aggressively.

US market implications (contracting and rebates)

Lamotrigine is typically treated as a core, off-patent CNS generic. In US channels, net revenue is strongly shaped by:

- rebate and discount structure between manufacturers, pharmacy benefit managers, and plans;

- utilization management (prior authorization, step therapy) when applicable;

- maintenance of supply and pharmacy reimbursement adequacy to prevent delistings.

EU market implications (tendering and national pricing)

Across Europe, where national reimbursement and tendering can be decisive:

- tendering in hospital and public procurement often yields rapid price resets;

- parallel trade (country arbitrage) can affect net realizations;

- substitution rules influence near-term brand/generic replacement speed.

What are the key demand drivers for lamotrigine today?

Demand for lamotrigine is anchored to two durable indications with long incidence tails: epilepsy and bipolar disorder maintenance (and related bipolar use patterns). The demand profile is stable relative to many niche CNS assets because:

- Epilepsy prevalence supports persistent treatment need across patient cohorts.

- Chronic maintenance use creates ongoing prescriptions rather than short courses.

- Dose titration requirements can slow abrupt discontinuation, supporting continued demand through therapeutic continuity.

Indication mix constraints

Lamotrigine is used as a chronic therapy. That affects financial trajectory:

- sales growth is not generally “new patient” driven; it is driven by retention, treatment adherence, and minor shifts in prescribing share versus alternatives.

- growth is more likely to come from population-level persistence and regional formulary dynamics than from major clinical switching events.

How do competitors and substitution affect pricing and margins?

Core competitive set

Lamotrigine competes against:

- Other antiepileptics (including newer agents and broad off-patent options in the same therapeutic class).

- Within-class switching based on tolerability, seizure control, and payer preferences.

- Generic substitution among lamotrigine manufacturers once approved.

Pricing mechanics

Because the molecule is off-patent, competitive pricing pressure tends to operate through three layers:

- Manufacturer list pricing resets quickly after additional generic approvals and market entrants.

- Net price falls further as contracting, rebates, and rebates clawbacks become more aggressive.

- Wholesaler and dispenser pricing pass-through is influenced by reimbursement rules, which can drive sudden utilization changes.

Margin trajectory

A generic-heavy market typically implies:

- lower manufacturer margins over time as competitive intensity rises;

- profit concentration among suppliers with robust scale, reliable supply, and strong contracting positions;

- higher volatility in earnings around manufacturing disruptions, supply constraints, and tender outcomes.

What does the financial trajectory typically look like for off-patent lamotrigine?

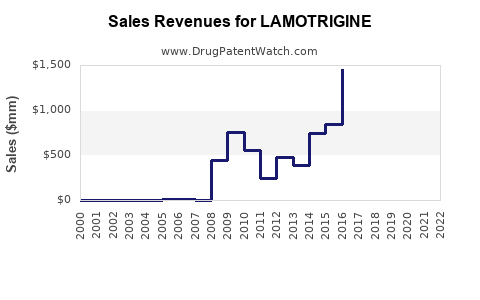

A typical lamotrigine financial trajectory in a generic-dominated era has these features:

- Early post-LOE period: sales stabilize or decline slowly as patients switch to generics.

- Mid-cycle: continued price compression with volume retention, often with flat-to-declining revenue but relatively stable units (or unit growth offset by lower price).

- Late cycle: deeper contracting and tendering leads to further net price compression; growth becomes limited to demographic and prescription growth plus share gains from formulary switches.

Net effect: revenue often trends down or plateaus in value terms even when patient volumes remain steady.

What market events can shift lamotrigine’s financial outcomes?

Lamotrigine’s commercial volatility tends to come from market mechanics rather than new clinical breakthroughs. The most consequential event types are:

- ANDA supply changes: new entrants or plant-level supply issues can swing net pricing and market share quickly.

- Formulary/tender outcomes: winning contracts for large purchasing bodies can increase volume, while losing them can cause sharp share drops.

- Regulatory and product quality incidents: recalls, compliance remediation, and manufacturing interruptions can reallocate demand temporarily toward alternative SKUs.

- Patent litigation outcomes affecting timing of competition: in the US, litigation around exclusivity and product-specific patents can alter entry timing and competitive intensity. (For lamotrigine, the core market is now well into generic competition.)

How large is the lamotrigine opportunity by segment and geography?

A granular segment-by-segment revenue map requires proprietary datasets and market reporting. What can be stated from available public sources is:

- The drug is widely marketed as generics and used broadly in epilepsy.

- Financial performance is largely a function of country reimbursement frameworks and US managed care contracting.

- The presence of multiple manufacturers reduces the likelihood of sustained brand-like price premiums, placing revenue sensitivity on pricing and volume.

Without access to a consistent public dataset providing segment-level sales, any attempt to quantify exact market dollars by region would be speculative.

What role do payer policies play in lamotrigine’s financial trajectory?

Payer policies are structurally important in generic CNS therapy. They influence both utilization and the financial path:

- Formulary tiering: when lamotrigine is placed on preferred tiers, share stability improves.

- Utilization management: prior authorization can slow switching and can affect persistence in marginal cases.

- Quantity limits and day supply rules: these can alter dispensing patterns and influence total scripts.

For off-patent generics, payer policy is less about “access denial” and more about controlling cost through contracting and preferred products.

What is the compliance and safety profile impact on commercial performance?

Lamotrigine carries a known risk profile, including severe skin reactions in susceptible patients. Commercial consequences, when they occur, generally show up as:

- prescribing caution leading to slower titration adherence or temporary prescriber preference shifts;

- product substitution impacts in specific subpopulations if prescribers change generic SKUs due to perceived tolerability differences.

In aggregate, the chronic demand base usually offsets most safety-driven disruptions, but in single markets it can still affect share.

What can investors and R&D planners take from lamotrigine’s market dynamics?

Lamotrigine is best viewed as a reference molecule for how an off-patent CNS product behaves:

- Commercial resilience comes from persistent indications and chronic use.

- Revenue is capped by generic price compression.

- Value shifts increasingly depend on supply scale, tender wins, and contracting strength rather than differentiation.

For R&D planning, the implication is that incremental clinical differentiation in off-patent classes must translate into payer-relevant outcomes to avoid being captured by generic economics. For investment planning, lamotrigine is more aligned with a manufacturing and commercial execution thesis than with a patent-duration thesis in the current era.

Key Takeaways

- Lamotrigine’s market is generic-dominated; pricing and revenue track primarily with contracting, tender outcomes, and generic entry intensity.

- Demand remains stable in epilepsy and bipolar maintenance due to chronic use, but value growth is limited by net price compression.

- Financial trajectory typically shows revenue plateauing or decline in value terms over time even when unit volumes hold up.

- Commercial volatility arises from supply, formulary shifts, and regulatory/product events, not from new product breakthroughs.

- Current commercialization dynamics support a view of lamotrigine as a price-volume market rather than a brand-growth market.

FAQs

-

Is lamotrigine still under patent protection in major markets?

Lamotrigine is widely available as generics globally, indicating that active exclusivity has largely expired in major markets, making the commercial environment dominated by ANDA competition.

-

What drives lamotrigine prescriptions most: new patient growth or continuation?

Continuation and persistence drive most of the demand in chronic epilepsy and bipolar maintenance use patterns, with share changes influenced by formulary and contracting.

-

Why do lamotrigine revenues often fall even when prescriptions remain stable?

Revenue is sensitive to net pricing. Generic competition typically reduces list price and further compresses net realized price through rebates and contracting.

-

What events most frequently cause short-term swings in lamotrigine sales?

Supply constraints, tender contract outcomes, delistings/relistings, and manufacturing incidents that reallocate demand across SKUs.

-

Does clinical differentiation matter for off-patent lamotrigine economics?

It matters, but only when it changes payer-relevant outcomes or shifts formularies. In practice, generic pricing pressure often limits how much clinical differentiation can translate into sustained premium revenue.

References

[1] FDA. (n.d.). Lamictal (lamotrigine) prescribing information. U.S. Food and Drug Administration. https://www.accessdata.fda.gov/

[2] FDA. (n.d.). Approved drug products with therapeutic equivalence evaluations (Orange Book): lamotrigine. U.S. Food and Drug Administration. https://www.accessdata.fda.gov/scripts/cder/daf/

[3] World Health Organization. (n.d.). ATC/DDD index. WHO Collaborating Centre for Drug Statistics Methodology. https://www.whocc.no/