Last updated: April 25, 2026

What drives lamivudine demand in 2025?

Lamivudine is a nucleoside reverse transcriptase inhibitor (NRTI) used in HIV and chronic hepatitis B (HBV), most commonly in fixed-dose combinations for HIV and as a monotherapy option for HBV depending on guideline-driven sequencing and resistance patterns. Demand is shaped by (1) persistence of chronic infections requiring long-term therapy, (2) guideline preference for combination regimens in HIV, (3) HBV treatment algorithms that increasingly weight resistance history and durability, and (4) the pace of generic penetration after originator exclusivity expiry.

Core use-cases that keep the base market stable

Lamivudine is used for:

- HIV: in combination antiretroviral therapy (ART), including fixed-dose products that improve adherence.

- Chronic HBV: long-term suppression of viral replication, where resistance and durability determine switching and add-on strategies.

Competitive landscape

The market is materially shaped by:

- Generic supply: lamivudine is widely available globally, compressing prices and shifting economics toward volume and tender execution.

- Shelf life and supply reliability: long-duration chronic indications make continuity of supply a key purchasing criterion, especially for government and pooled procurement programs.

- Originator-to-generic migration: pricing trajectories after patent cliffs typically compress revenue per dose, but volume can expand when procurement policies standardize.

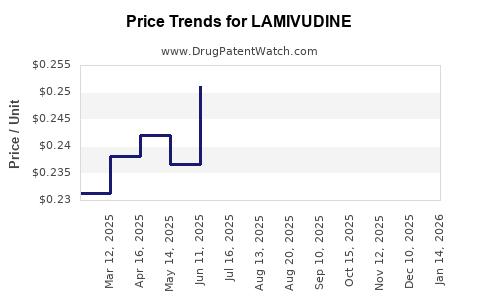

How does generic penetration affect lamivudine pricing and revenue?

Lamivudine has progressed through the standard patent cliff dynamic seen in mature NRTIs. Generic entry shifts pricing from innovation-led pricing to procurement-led contracting, with:

- Lower unit prices once multiple suppliers compete.

- More variation in regional realizations based on tender frequency, reimbursement rules, and local manufacturing capacity.

- Revenue dependence on dosing volume rather than differentiation, because clinical differentiation is limited once formulations are therapeutically equivalent.

This is consistent with the broader pattern for off-patent small-molecule antivirals where payer and provider behavior prioritizes lowest net price subject to supply constraints and quality systems.

What are the market dynamics in HIV versus HBV?

HIV: regimen stickiness and combination adoption

In HIV, lamivudine demand is driven by:

- Combination regimen adoption: lamivudine is rarely used as standalone therapy.

- Formulary inclusion: once a lamivudine-containing fixed-dose combination is listed, switching costs and procurement cycles slow churn.

- Manufacturing consolidation among qualified suppliers: tender-based procurement tends to favor suppliers who can meet quality requirements and deliver continuity.

The HIV market for lamivudine is therefore more procurement-stable than a pure “innovation” market, with revenue and volume tied to national ART scale-up and drug-program budgets.

HBV: durability, resistance, and sequencing decisions

HBV demand is influenced by:

- Resistance profile considerations: long-term lamivudine use is affected by viral resistance over time, so clinicians and programs increasingly evaluate alternative agents with higher genetic barrier in patients where long-term suppression is expected.

- Switching and add-on decisions: where resistance emerges, treatment may switch to agents considered more durable, reducing lamivudine share in incident and continuing HBV subsegments.

- Disease severity segmentation: lamivudine’s role can persist in segments where prescribing patterns, cost constraints, or treatment sequencing keep it in use.

Net effect: HBV is more prone to share loss as newer, more durable HBV options gain formulary share, while HIV tends to hold more stable demand through combination regimen inertia.

How has lamivudine’s regulatory and usage footprint shaped financial trajectory?

The financial trajectory for lamivudine is best understood as a mature-market profile:

- Stable global demand for chronic indications supports volume.

- Persistent price compression from generic competition reduces revenue per unit.

- Share shifts within HBV can reduce incremental growth versus earlier eras.

Clinical and prescribing baselines are anchored by established label positions for HIV and HBV. The U.S. National Library of Medicine’s drug profile confirms lamivudine’s approved uses and long-standing role in HIV and HBV therapy (MedlinePlus Drug Information) [1].

What does the cash-flow profile typically look like for lamivudine manufacturers?

For manufacturers, lamivudine’s financial trajectory generally follows a “volume-margin” structure rather than “innovation-margin”:

- Revenue engine: global procurement volume through tenders, distributor channels, and national formularies.

- Gross margin pressure: generic competition compresses price and increases marketing and compliance costs needed to win tenders.

- Operating leverage is limited: quality and regulatory compliance costs remain fixed while revenue per dose declines.

- Working capital and logistics matter: chronic-use markets require high fill rates, driving inventory management discipline.

This pattern is common across mature generic antivirals, where growth depends on supplier qualification, contract wins, and geographic expansion rather than new clinical differentiation.

How does geographic procurement affect outcomes?

Lamivudine is highly sensitive to country-level purchasing mechanisms:

- Government procurement and donor-funded programs: large-scale demand can be stable but contract cycles are structured and can abruptly reorder supplier rankings.

- Regional generics ecosystems: regions with multiple manufacturers often see more aggressive price competition.

- Tender implementation risk: winning suppliers can enjoy volume stability, while losing suppliers may see revenue step-downs after a bidding cycle.

For business planning, financial models for lamivudine typically treat growth as a function of contract wins and tender participation success rather than brand-building.

What are the investment-relevant indicators to track?

For lamivudine, the actionable indicators are less about “next clinical trial” and more about market mechanics:

- Generic tender pricing trends (net price, not list price).

- Supplier qualification and compliance status (quality system audits, regulatory inspection outcomes).

- Formulary inclusion rates in HIV fixed-dose combinations and HBV treatment guidance alignment.

- Switching patterns in HBV that indicate shrinking lamivudine share in more durable-therapy cohorts.

These indicators map directly to revenue timing and downside risk: contract repricing and share loss are the primary drivers.

How has the broader NRTI market environment influenced lamivudine?

Lamivudine sits in a category where:

- Off-patent economics dominate.

- Treatment guidelines gradually alter market share by favoring agents with improved resistance and durability where possible.

- Combination tablet ecosystems stabilize parts of the HIV segment.

As a mature NRTI, lamivudine behaves like a commodity antiviral with forecast uncertainty dominated by procurement cycles and HBV guideline evolution rather than clinical breakthrough expectations.

Where does this leave lamivudine’s financial trajectory (directionally)?

Directionally, the lamivudine market trajectory is characterized by:

- Ongoing volume from chronic HIV and HBV therapy needs.

- Continued price compression as generic supply remains abundant.

- Differential growth: HIV tends to be steadier due to combination regimen adoption; HBV can show softer share growth or negative share in settings that migrate to higher-barrier HBV agents over time.

- Contract and geography driven revenue swings around tender cycles.

This profile is consistent with lamivudine’s established role and long market duration across HIV and HBV indications as reflected in standard drug references [1].

Key Takeaways

- Lamivudine demand is anchored by chronic HIV and HBV treatment, not by innovation cycles.

- Generic penetration drives sustained price compression, making revenue primarily volume- and contract-dependent.

- HIV demand is typically more stable due to combination regimen inertia and formulary listing dynamics.

- HBV share is more exposed to guideline-driven switching when resistance durability becomes the deciding factor.

- Financial outcomes track procurement execution: tender pricing, supplier qualification, and contract continuity dominate the trajectory.

FAQs

1) Is lamivudine mainly a commodity market or a branded market?

It is predominantly a commodity market due to broad generic availability and procurement-led contracting for chronic indications [1].

2) What indication contributes more stability for lamivudine pricing and volume?

HIV generally provides more stability because lamivudine is used in combination ART and tends to remain within formulary structures longer than monotherapy HBV segments that may switch based on resistance durability [1].

3) What is the main risk to lamivudine market share in HBV?

Treatment switching in chronic HBV driven by resistance durability considerations can reduce lamivudine share over time [1].

4) What is the most important driver of financial performance for manufacturers?

Winning and retaining procurement contracts that sustain volume while managing margin under competitive net pricing [1].

5) What indicators best predict near-term revenue changes?

Tender outcomes, net pricing movements from competitive bidding, and formulary inclusion changes in HIV fixed-dose combinations and HBV sequencing [1].

References

[1] MedlinePlus. (n.d.). Lamivudine. U.S. National Library of Medicine. https://medlineplus.gov/druginfo/meds/a695005.html