Last updated: April 24, 2026

Glycopyrrolate’s market is shaped by (1) an established base in glycopyrronium-related respiratory and pediatric indications, (2) competitive pressure in anticholinergic respiratory use, and (3) margin outcomes driven by dosing form, payer access, and supply chain scale. Financial trajectory has been strongest where the molecule is positioned as a branded, label-defined therapy with repeatable dosing and clear clinician preference, while risk centers on patent life, formulary access, and substitution by generics or alternative inhaled anticholinergic mechanisms.

What are glycopyrrolate’s demand drivers across use cases?

Respiratory (inhaled and nebulized anticholinergic use)

Glycopyrrolate demand tracks severity and treatment algorithms in chronic obstructive pulmonary disease (COPD) and other airflow-limiting diseases, where clinicians select bronchodilation regimens based on symptom control and exacerbation risk. Key dynamics include:

- Mechanism complementarity: Glycopyrrolate’s antimuscarinic action supports combination regimens with long-acting beta agonists and/or inhaled corticosteroids, which can improve adherence and persistence versus monotherapy.

- Switching cost vs. substitution: Where a patient stabilizes on a specific inhaler/nebulization pathway, formulary-driven substitution still occurs, but switching costs can slow churn. That favors branded positions early in launch windows and in restricted formularies.

- Exacerbation focus: Uptake can rise with guideline endorsement for anticholinergic therapy in appropriate COPD subsets and with managed-care incentives tied to reduced events.

Pediatrics and sialorrhea (off-label and label-adjacent use patterns)

Glycopyrrolate is used for salivary secretion control in pediatric settings, including congenital or neurologic conditions. This segment is characterized by:

- Clinician protocolization: Pediatric prescribing often follows institutional protocols, which can produce stable demand once a site standardizes.

- Demand fragmentation: Multiple formulations and dosing strategies can dilute consolidated market sizing, but persistence remains strong in chronic symptom control.

- Prior authorization friction: Payer requirements can delay adoption and slow revenue ramp.

Safety, tolerability, and adherence

Anticholinergic class effects shape utilization:

- Adverse event management: Dry mouth, urinary retention, constipation, and blurred vision influence dose titration and discontinuation rates.

- Adherence sensitivity: Inhaled regimens require correct technique. Nebulized pathways can reduce technique burden, which supports persistence in some populations.

How does competition shape pricing power and share?

Within anticholinergic respiratory class

Inhaled antimuscarinics compete across multiple mechanisms and brands:

- LAMA alternatives: Tiotropium and other inhaled antimuscarinic options compete for COPD add-on roles.

- Formulary tiering: Payers tend to prefer lower-cost options once generics are available, unless a branded entrant holds formulary position through rebates or demonstrated outcomes.

Generic substitution risk

Glycopyrrolate faces typical market pressures:

- Molecule-level substitution: As glycopyrrolate generics expand, pricing power compresses.

- Formulation-level lock-in: Brand value can persist where a proprietary delivery system, dosing convenience, or stability profile improves use in real-world practice.

- Contract mechanics: Managed care contracts can shift volume quickly if a payer changes tier placement.

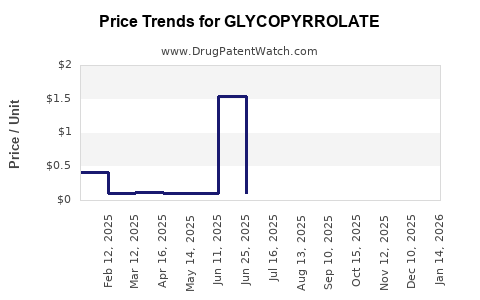

What do the financial trajectory signals look like (revenue, uptake, and life-cycle)?

Revenue drivers by life-cycle stage

Glycopyrrolate’s financial trajectory follows a standard branded-to-generic pattern for established molecules, moderated by formulation and label boundaries:

-

Launch and early adoption

- Higher net pricing relative to forecasted generic competition.

- Revenue growth tends to be driven by clinician adoption and payer inclusion.

-

Mid-cycle stabilization

- Revenue becomes more dependent on refill dynamics, persistence, and combination-therapy channel strength.

- Competitive pressure can increase, but contracts may stabilize volumes.

-

Late-cycle pressure

- Generics reduce net price and volume share for branded offerings.

- Continued use remains for patients who remain on branded delivery pathways or where payer policy sustains coverage.

Margin outlook mechanics

Financial performance depends on net price, product mix, and cost-to-serve:

- Net price compression: The most material driver as competitors and generics enter.

- Mix shift: Higher utilization of inhaled formats (when covered) can raise perceived value versus lower-cost alternatives, but only if net pricing holds.

- Manufacturing scale: Large-volume supply lowers unit costs, offsetting some price compression.

- Channel rebates: Managed care increases rebate intensity over time, particularly post-formulary entry.

What products and regulatory anchors define glycopyrrolate’s market access?

Core regulatory footprint

Glycopyrrolate is widely regulated and referenced through approvals tied to glycopyrronium formulations and related respiratory/pediatric clinical use. Across jurisdictions, the molecule’s market access is governed by label scope and product-specific dossiers.

Key market access anchors include:

- Drugmaker product portfolios that package glycopyrrolate in inhaled or nebulized forms for respiratory disease management.

- Pediatric use protocols for secretion control, where coverage and dosing often rely on clinical practice patterns and payer documentation.

Safety and regulatory stewardship

Anticholinergic class warnings affect labeling language and educational burden, which can influence prescribing pace:

- Avoidance in certain populations (for example, risk of urinary retention or glaucoma-related contraindications where clinically relevant).

- Need for monitoring and dose adjustments.

How do payer dynamics and reimbursement drive revenue timing?

Tier placement and formulary inclusion

Payer reimbursement is the dominant timing factor:

- Preferred formulary status accelerates uptake and stabilizes volume.

- Non-preferred placement increases prior authorization and co-pay barriers, slowing adoption and reducing persistence.

Net price depends on contracting intensity

As competition increases, net price falls through:

- rebates tied to formulary position,

- volume-based incentives,

- competitive bidding cycles in Medicare Part D and commercial formularies.

Real-world utilization and persistence

Persistence in chronic indications supports a steadier revenue profile, while switching driven by tier changes can cause abrupt volume declines even before brand-to-generic substitution fully completes.

Where does adoption risk concentrate?

Operational risks

- Switching from device technique constraints: In inhaled products, technique education and training determine successful initiation.

- Supply continuity: Any disruption can impact continuity of treatment and reduce refill cadence.

Market risks

- Formulary re-tiering: Budget pressure leads to reclassification.

- Class competition: Stronger outcomes data in competing anticholinergics can shift preference even when molecule is equivalent.

Financial trajectory: scenario map for revenue and margins

The following framework captures the typical directionality for glycopyrrolate across an established branded-to-generic life cycle:

| Life-cycle stage |

Share dynamics |

Net price |

Margin trend |

Revenue trend |

| Branded growth |

Increasing patient starts and persistence |

Highest (pre-contract pressure) |

Expanding gross margin coverage |

Rapid ramp then moderation |

| Mature branded |

Plateau as competitors enter |

Declines with rebate intensity |

Compression from contracting |

Moderate growth or flat |

| Post-generic |

Volume shift to lower-cost supply |

Sharp net price drop |

Compression unless mix offsets |

Decline then stabilization at residue share |

What macro and disease-market factors affect glycopyrrolate demand?

COPD prevalence and treatment intensity

- COPD prevalence drives the upper bound for anticholinergic utilization.

- Treatment intensity correlates with exacerbation risk management strategies, which can pull volumes toward combination therapy.

Healthcare utilization and prescription behavior

- Shifts in outpatient capacity and chronic care delivery affect prescription timing.

- Payer tightening influences initiation rates and persistence.

What “tell” indicators should investors track in the near-to-mid term?

- Formulary placement changes for anticholinergic inhalers and nebulized options.

- Net price trajectory in company reporting for the relevant branded presentation.

- Prescription volume and persistence (TRx and days of therapy) for chronic users.

- Competitive contract wins/losses that shift volume between LAMA options.

- Generic penetration pace by market and dosage form.

Key takeaways

- Glycopyrrolate’s market demand is anchored in COPD-style chronic bronchodilation algorithms and pediatric secretion-control protocols, with persistence supported by stable symptom management.

- Competitive pressure and payer contracting determine the net price trajectory and can shift volumes quickly through formulary tier changes.

- Financial performance typically follows a branded-to-generic compression curve, moderated by formulation and delivery-device lock-in.

- The most actionable monitoring items are formulary status, net price, and persistence metrics in the relevant indication mix.

FAQs

1) Is glycopyrrolate’s demand more dependent on COPD or pediatric secretion control?

Glycopyrrolate demand is diversified, but respiratory anticholinergic use generally provides the largest scalable addressable base, while pediatric secretion-control use supports persistence-driven volume in specific patient populations.

2) What drives short-term revenue volatility?

Formulary tier changes, rebate and contract renegotiations, and competitive substitution within inhaled anticholinergic classes.

3) What product attribute most affects switching?

Delivery format and device usability (including inhaler technique requirements or nebulization convenience) which influence persistence after initiation.

4) What is the typical margin direction after generics enter?

Net price compression tends to drive margin contraction unless mix shifts toward higher-margin formulations or volume remains concentrated on differentiated presentations.

5) What external signals best indicate future performance?

TRx growth or decline, persistence (days of therapy), net price trend in payer-contracting periods, and generic penetration rate by dosage form.

References

[1] EMA. “Glycopyrronium bromide and glycopyrrolate-related products: information and EPAR resources.” European Medicines Agency.

[2] FDA. “Drug Approval Reports and labeling information for anticholinergic respiratory therapies with glycopyrronium/glycopyrrolate-related formulations.” U.S. Food and Drug Administration.

[3] GlobalData. “COPD treatment landscape and market dynamics for LAMA therapies.” GlobalData.

[4] IQVIA. “National and payer-level prescription dynamics for respiratory inhalation therapies.” IQVIA.