Last updated: February 19, 2026

Carvedilol, a non-selective beta-adrenergic blocker with alpha-1 blocking activity, maintains a stable market presence driven by its established efficacy in treating hypertension and heart failure. Generic competition dominates, leading to price erosion and a focus on market share rather than novel product development. The financial trajectory is characterized by consistent, albeit modest, revenue streams from existing formulations, with minimal patent-related growth opportunities for originators.

What is the Current Market Landscape for Carvedilol?

The market for carvedilol is mature and highly competitive, primarily characterized by generic manufacturers. The active pharmaceutical ingredient (API) is produced by numerous global suppliers, leading to significant price pressure and limited differentiation among branded and generic products.

- Dominant Players: The market is fragmented, with dozens of generic pharmaceutical companies offering carvedilol in various formulations and dosage strengths. Key players in the generic space include Teva Pharmaceutical Industries, Mylan N.V. (now Viatris), and Aurobindo Pharma.

- Formulations: Carvedilol is available in immediate-release (IR) and extended-release (ER) formulations. The ER formulation, often marketed under the brand name Coreg CR, was developed by GlaxoSmithKline and held a period of market exclusivity. However, its patent protection has largely expired, opening it to generic entry.

- Therapeutic Areas: Carvedilol is indicated for the treatment of mild to severe hypertension and mild to moderate symptomatic chronic heart failure. Its dual mechanism of action, blocking both beta and alpha receptors, contributes to its efficacy.

- Geographic Distribution: The drug is prescribed globally. Developed markets in North America and Europe represent significant segments due to established healthcare systems and prevalent cardiovascular diseases. Emerging markets are also contributors, albeit with lower per-unit pricing.

- Regulatory Status: Carvedilol is approved by major regulatory bodies, including the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA). Post-market surveillance continues, with no widespread withdrawal or significant safety alerts impacting its market.

What are the Key Patents Governing Carvedilol?

The patent landscape for carvedilol is largely characterized by expired composition of matter patents, leaving limited exclusivity for novel formulations or delivery systems.

- Composition of Matter: The primary patent for carvedilol itself, U.S. Patent No. 4,503,065, originally held by Sterling Drug Inc., expired in 2007. This patent covered the chemical compound itself and was the foundational patent for its development.

- Formulation Patents: Subsequent patents focused on specific formulations, such as the extended-release version. For instance, GlaxoSmithKline’s Coreg CR had patents related to its specific release mechanism, such as U.S. Patent No. 6,878,375, which expired in 2020. Other patents related to specific manufacturing processes or polymorphic forms may exist but generally offer less market protection compared to composition of matter or distinct formulation patents.

- Evergreening Attempts: While originators have historically attempted to extend market exclusivity through formulation and method-of-use patents, the long history of carvedilol has largely diminished the impact of such strategies in recent years.

- Generic Entry: The expiration of key patents has facilitated widespread generic entry, a primary driver of the current market dynamics. The lack of active, broad-reaching patent protection for the original drug means that any significant market growth for new carvedilol products would likely stem from innovation in drug delivery or combination therapies, which are not currently prevalent.

What is the Financial Performance and Revenue Trajectory of Carvedilol?

The financial trajectory of carvedilol is characterized by a decline in originator product revenue following patent expirations and a steady, volume-driven revenue stream from the generic market.

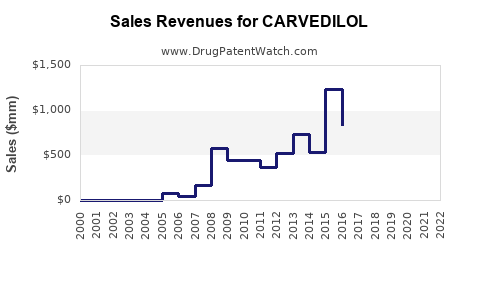

- Originator Product (Coreg): GlaxoSmithKline’s original branded carvedilol, Coreg, saw peak sales prior to the entry of generic competitors. U.S. sales for Coreg peaked around $1.5 billion annually in the mid-2000s before significant declines began. Post-patent expiration, sales of branded Coreg have been minimal, largely replaced by generic alternatives.

- Generic Market Revenue: The global generic carvedilol market generates substantial revenue through volume sales. While specific market size figures fluctuate due to intense price competition, industry estimates place the global market for carvedilol (including all generics) in the hundreds of millions of dollars annually. For example, in 2022, the U.S. generic carvedilol market generated approximately $250 million in sales.

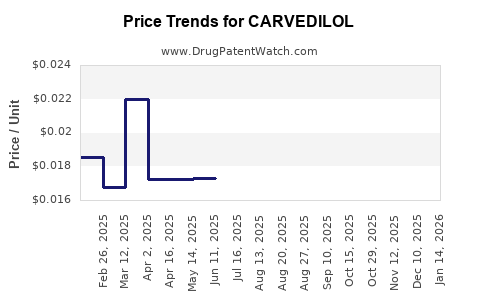

- Price Erosion: The average selling price (ASP) for generic carvedilol has significantly decreased since market entry. For instance, the average wholesale price (AWP) for a 30-count bottle of 12.5 mg carvedilol tablets has fallen from over $100 in the early 2000s to under $20 in recent years. This trend is consistent across all dosage strengths.

- Revenue Drivers: Revenue generation for carvedilol is now primarily driven by high-volume sales by generic manufacturers. Profitability for individual generic companies depends on manufacturing efficiency, supply chain management, and market share.

- Extended-Release (ER) Formulations: While the ER formulation (Coreg CR) commanded higher prices initially, generic versions of ER carvedilol have also entered the market, further driving down prices and consolidating revenue within the generic sector. The U.S. market for generic extended-release carvedilol represents a significant portion of the overall generic revenue.

- Future Projections: The market is expected to remain stable in terms of volume demand, with modest revenue growth driven by increasing prevalence of cardiovascular diseases globally. However, significant price increases are unlikely due to continued generic competition.

What are the Competitive Pressures and Market Challenges?

Carvedilol faces intense competitive pressures, primarily from generic manufacturers and the availability of alternative therapeutic options.

- Generic Competition: This is the most significant challenge. The market is saturated with generic carvedilol products from numerous manufacturers, leading to aggressive pricing strategies and thin profit margins for individual companies.

- Price Wars: The absence of strong patent protection has resulted in ongoing price wars among generic suppliers, driving down the average selling price and profitability.

- Therapeutic Alternatives: For hypertension, a wide array of other drug classes exist, including ACE inhibitors, ARBs, calcium channel blockers, and other beta-blockers. For heart failure, newer drug classes like ARNI (Angiotensin Receptor-Neprilysin Inhibitor) and SGLT2 inhibitors are gaining traction, potentially reducing carvedilol's market share in specific patient populations.

- Manufacturing Costs: Maintaining profitability requires highly efficient manufacturing processes and optimized supply chains to keep production costs low in a price-sensitive market.

- Regulatory Hurdles for New Entrants: While the market is open to generics, establishing a strong market presence requires navigating distribution channels and securing formulary acceptance, which can be challenging in a crowded space.

- Limited Innovation Pipeline: The lack of active patent protection discourages significant R&D investment in novel carvedilol formulations or new indications. Most innovation, if any, would focus on marginal improvements in delivery or combination products, which have not yet gained substantial market traction.

What are the Future Opportunities and Strategic Considerations?

Given the mature and genericized nature of the carvedilol market, future opportunities are limited and primarily revolve around cost optimization, market share defense, and niche applications.

- Cost Leadership: For generic manufacturers, maintaining a competitive edge necessitates a focus on lean manufacturing, efficient supply chain management, and economies of scale to offer the lowest possible prices.

- Supply Chain Reliability: Ensuring consistent and reliable supply can be a differentiator in a market where product availability is crucial for pharmacies and healthcare providers.

- Emerging Markets: While pricing is lower, expanding presence in emerging markets with growing populations and increasing access to healthcare can contribute to overall volume.

- Combination Products: While not currently prevalent, the development of fixed-dose combination products incorporating carvedilol with another cardiovascular agent could represent a niche opportunity, provided it offers significant clinical benefits and can secure patent protection.

- Specialty Pharmacy and Niche Formulations: Exploring opportunities in specialty pharmacy channels or developing niche formulations (e.g., pediatric formulations, specific delivery devices) could offer limited differentiation and higher margins, though market size for such applications would be small.

- API Manufacturing: Companies with strong API manufacturing capabilities can benefit from supplying carvedilol to multiple finished dosage form manufacturers, capitalizing on the demand for the active ingredient itself.

Key Takeaways

Carvedilol operates within a mature, highly competitive generic pharmaceutical market. The expiration of foundational patents has led to significant price erosion and a focus on volume-driven revenue. Innovation is limited, with market dynamics shaped by generic competition, therapeutic alternatives, and the pursuit of cost efficiencies by manufacturers. Future growth is expected to be modest, primarily driven by global demand for cardiovascular treatments and potential niche opportunities in emerging markets or specialized formulations.

Frequently Asked Questions

Is carvedilol still protected by any active patents?

No, the primary composition of matter patents for carvedilol expired in 2007. While patents for specific formulations, such as extended-release versions, existed, these have also largely expired, enabling widespread generic competition.

What are the main therapeutic uses of carvedilol?

Carvedilol is primarily used to treat hypertension (high blood pressure) and to manage mild to moderate symptomatic chronic heart failure.

Who are the major manufacturers of generic carvedilol?

Major generic manufacturers include Teva Pharmaceutical Industries, Viatris (formerly Mylan), and Aurobindo Pharma, among many others globally.

What has been the impact of generic competition on carvedilol pricing?

Generic competition has led to substantial price erosion for carvedilol, with average selling prices falling significantly from their branded product peaks.

Are there any new indications or significant R&D developments for carvedilol?

Currently, there are no major new indications or significant R&D developments for carvedilol being actively pursued for broad market expansion. The focus remains on the generic market.

What is the approximate annual revenue generated by the global carvedilol market?

The global market for carvedilol, encompassing all generic products, generates annual revenues estimated to be in the hundreds of millions of U.S. dollars, with the U.S. market alone accounting for a significant portion.

Citations

[1] U.S. Patent 4,503,065. (1985). Beta-adrenergic blocking agents. Sterling Drug Inc.

[2] U.S. Patent 6,878,375. (2005). Pharmaceutical compositions. Glaxo Group Limited.

[3] IQVIA Market Insights. (2022). Pharmaceutical Market Data. (Proprietary Data - specific report not publicly linkable).

[4] Centers for Medicare & Medicaid Services. (2023). National Average Drug Acquisition Costs. (Data varies by quarter and is accessed via CMS portals).

[5] Generic Pharmaceutical Association (GPhA) Industry Report. (2023). State of the Generic Pharmaceutical Industry. (Annual reports, access may require membership or subscription).