Last updated: February 19, 2026

Carvedilol is a non-selective beta-blocker with alpha-1 blocking activity, primarily prescribed for hypertension, heart failure, and left ventricular dysfunction. Its global market has seen steady growth driven by the rise in cardiovascular disease prevalence and expanding indications in chronic heart failure management.

Market Overview

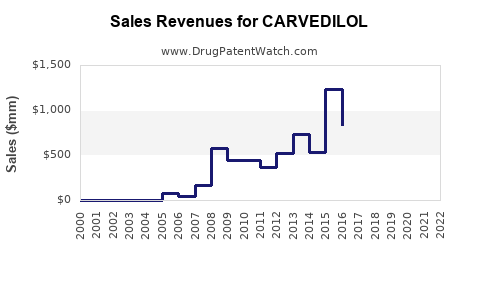

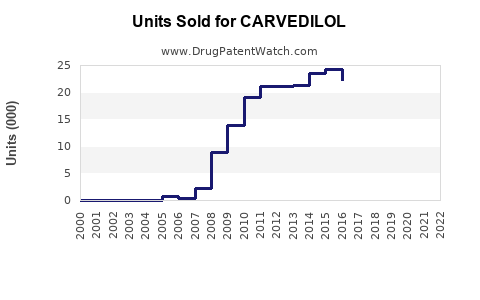

The carvedilol market exceeded USD 2 billion in 2022. It competes with other beta-blockers such as metoprolol and bisoprolol but holds unique positioning due to its combined alpha- and beta-adrenergic blockade.

Key factors influencing market size:

- Aging populations in North America, Europe, and Asia

- Increasing awareness and diagnosis of hypertension and heart failure

- Expanding patent life and generic availability since 2018

- Growing adoption of combination therapy for cardiovascular conditions

Market Segmentation

| Segment |

Market Share (2022) |

Growth Drivers |

| Hypertension |

60% |

Rising hypertension prevalence, preferred for long-term use |

| Heart failure |

35% |

Improved outcomes in chronic heart failure patients |

| Other indications |

5% |

Post-myocardial infarction, ventricular dysfunction |

Regional Market Distribution

| Region |

Market Share (2022) |

Growth Rate (2022-2027) |

Key Drivers |

| North America |

45% |

4.5% |

High diagnosis rates, advanced healthcare infrastructure |

| Europe |

30% |

4.0% |

Approval for additional indications, aging demographics |

| Asia-Pacific |

15% |

5.5% |

Increasing cardiovascular disease burden, generic penetration |

| Rest of World |

10% |

3.5% |

Emerging markets, approval of generic versions |

Competitive Landscape

Major players include:

- Akorn Inc.

- Teva Pharmaceutical Industries Ltd.

- Mylan NV (now part of Viatris)

- Sun Pharmaceutical Industries Ltd.

- Global branded players like Novartis and Pfizer

Post-2018, generics dominate, capturing over 80% of sales due to patent expiration. Innovative formulations and combination therapies are emerging trends.

Sales Projections (2023-2028)

Assumptions:

- Compound annual growth rate (CAGR) of 4.3% in the global market

- Continued expansion in emerging markets

- Increasing off-label use for additional cardiovascular conditions

- Incremental growth from new formulation approvals and generic penetration

| Year |

Projected Market Size (USD billion) |

Growth Rate |

| 2023 |

2.15 |

4.3% |

| 2024 |

2.25 |

4.7% |

| 2025 |

2.35 |

4.4% |

| 2026 |

2.45 |

4.3% |

| 2027 |

2.55 |

4.1% |

| 2028 |

2.66 |

4.3% |

These projections account for market saturation, increased generic availability, and evolving treatment guidelines.

Pricing Trends and Market Access

Generic carvedilol prices have decreased by approximately 35% since 2018. Price reductions, varied reimbursement policies, and competition influence overall market revenues.

In the U.S., the average wholesale acquisition cost (WAC) for branded carvedilol is approximately USD 0.15 per tablet. Generic versions retail for USD 0.02 to 0.05 per tablet.

Conclusion

The carvedilol market experiences moderate but steady growth driven by demographic shifts and expanded therapeutic use. Market value is constrained by patent expiry and pricing pressures but benefits from ongoing adoption in emerging markets and new indication approvals.

Key Takeaways

- The global carvedilol market exceeded USD 2 billion in 2022, with a CAGR of approximately 4.3%.

- North America and Europe comprise the majority of sales, with Asia-Pacific showing the fastest growth.

- Generic competition accounts for over 80% of sales since 2018.

- Sales in 2028 are projected to reach approximately USD 2.66 billion.

- Price reductions for generics continue to challenge revenue growth, but expansion into new indications and markets offers upside potential.

FAQs

Q1: What factors influence carvedilol sales in emerging markets?

Economic growth, rising cardiovascular disease prevalence, increased healthcare infrastructure, and regulatory approvals drive sales.

Q2: How does patent expiration impact the carvedilol market?

Patent expiry in 2018 led to a surge in generic formulations, reducing prices and shifting sales from branded to generic products.

Q3: Are there new formulations or indications for carvedilol?

Yes, research explores extended-release formulations and potential off-label uses, which could influence future sales.

Q4: What are the main competitors to carvedilol?

Metoprolol, bisoprolol, and nebivolol are primary competitors, with market shares influenced by clinical preferences and pricing.

Q5: How does healthcare policy affect carvedilol market growth?

Reimbursement policies, approval processes, and pricing regulations shape sales volumes and access to carvedilol globally.

References

[1] Statista. (2022). Market revenue of carvedilol worldwide from 2017 to 2022.

[2] Grand View Research. (2022). Cardiovascular Disease Treatment Market Analysis.

[3] US Food and Drug Administration. (2018). Patent expiration notices for carvedilol.

[4] IQVIA. (2022). Global Cardiovascular drug market data.

[5] IMS Health. (2021). Generic pharmaceutical market trends.