Share This Page

AMINOCAPROIC Drug Patent Profile

✉ Email this page to a colleague

When do Aminocaproic patents expire, and what generic alternatives are available?

Aminocaproic is a drug marketed by Hikma, Abraxis Pharm, Baxter Hlthcare, Hospira, Luitpold, Zenara, Ajenat Pharms, Amneal, Annora Pharma, Aurobindo Pharma, Carnegie, Epic Pharma Llc, MSN, Regcon Holdings, Sciegen Pharms, Sunny, Taro, Tp Anda Holdings, Vistapharm Llc, Adaptis, Ani Pharms, and Rising. and is included in twenty-seven NDAs.

The generic ingredient in AMINOCAPROIC is aminocaproic acid. There are six drug master file entries for this compound. Twenty-two suppliers are listed for this compound. Additional details are available on the aminocaproic acid profile page.

DrugPatentWatch® Litigation and Generic Entry Outlook for Aminocaproic

A generic version of AMINOCAPROIC was approved as aminocaproic acid by LUITPOLD on December 1st, 1987.

AI Deep Research

Questions you can ask:

- What is the 5 year forecast for AMINOCAPROIC?

- What are the global sales for AMINOCAPROIC?

- What is Average Wholesale Price for AMINOCAPROIC?

Summary for AMINOCAPROIC

| US Patents: | 0 |

| Applicants: | 22 |

| NDAs: | 27 |

| Raw Ingredient (Bulk) Api Vendors: | 1 |

| Clinical Trials: | 39 |

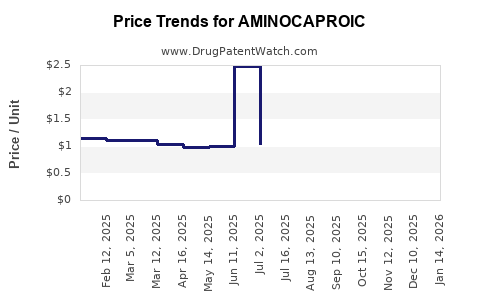

| Drug Prices: | Drug price information for AMINOCAPROIC |

| DailyMed Link: | AMINOCAPROIC at DailyMed |

Recent Clinical Trials for AMINOCAPROIC

Identify potential brand extensions & 505(b)(2) entrants

| Sponsor | Phase |

|---|---|

| Zagazig University | NA |

| Minia University | Phase 3 |

| NYU Langone Health | N/A |

US Patents and Regulatory Information for AMINOCAPROIC

| Applicant | Tradename | Generic Name | Dosage | NDA | Approval Date | TE | Type | RLD | RS | Patent No. | Patent Expiration | Product | Substance | Delist Req. | Exclusivity Expiration |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Rising | AMINOCAPROIC ACID | aminocaproic acid | TABLET;ORAL | 213944-001 | Sep 14, 2022 | AB | RX | No | No | ⤷ Start Trial | ⤷ Start Trial | ⤷ Start Trial | |||

| Sunny | AMINOCAPROIC ACID | aminocaproic acid | TABLET;ORAL | 209060-002 | Nov 27, 2018 | AB | RX | No | Yes | ⤷ Start Trial | ⤷ Start Trial | ⤷ Start Trial | |||

| Hikma | AMINOCAPROIC | aminocaproic acid | TABLET;ORAL | 075602-001 | May 24, 2001 | DISCN | No | No | ⤷ Start Trial | ⤷ Start Trial | ⤷ Start Trial | ||||

| Tp Anda Holdings | AMINOCAPROIC ACID | aminocaproic acid | SOLUTION;ORAL | 212494-001 | Aug 11, 2020 | AA | RX | No | Yes | ⤷ Start Trial | ⤷ Start Trial | ⤷ Start Trial | |||

| Carnegie | AMINOCAPROIC ACID | aminocaproic acid | TABLET;ORAL | 213928-001 | Feb 12, 2021 | AB | RX | No | No | ⤷ Start Trial | ⤷ Start Trial | ⤷ Start Trial | |||

| >Applicant | >Tradename | >Generic Name | >Dosage | >NDA | >Approval Date | >TE | >Type | >RLD | >RS | >Patent No. | >Patent Expiration | >Product | >Substance | >Delist Req. | >Exclusivity Expiration |

Aminocaproic Acid Market Dynamics, Financial Trajectory, Competition, and Exclusivity

Aminocaproic acid is a mature, off-patent antifibrinolytic used mainly in hospital and specialty-care settings. Its commercial value is driven by procurement volume, shortages, manufacturing continuity, and clinical substitution rather than patent protection. Public company filings do not separately disclose aminocaproic acid revenue, so the product’s financial trajectory is best assessed through regulatory status, hospital demand, generic competition, and exposure to tranexamic acid.

What is aminocaproic acid used for?

Aminocaproic acid, also known as epsilon-aminocaproic acid or EACA, inhibits fibrinolysis by competitively blocking lysine-binding sites on plasminogen and plasmin. It is available in oral and injectable forms and is used when excessive fibrinolysis contributes to bleeding.

The principal clinical applications are:

- Bleeding associated with elevated fibrinolytic activity

- Hematologic disorders, including selected bleeding episodes in hemophilia

- Perioperative bleeding in cardiac, hepatic, urologic, and other procedures

- Mucosal bleeding, including dental and gynecologic applications

- Selected off-label uses in traumatic, surgical, or localized bleeding

The FDA labeling limits the drug’s use to situations in which laboratory evidence or clinical assessment indicates that hyperfibrinolysis contributes to bleeding. It is not a general replacement for blood-product support or surgical hemostasis.[1]

Which dosage forms are commercially important?

| Dosage form | Typical commercial role | Primary channel |

|---|---|---|

| Injection, commonly 250 mg/mL | Acute inpatient and perioperative use | Hospitals, wholesalers |

| Tablets, commonly 500 mg | Outpatient or maintenance treatment | Retail, specialty, hospital pharmacies |

| Oral solution, commonly 0.25 g/mL | Pediatric, swallowing-limited, or dose-flexible use | Hospital and specialty pharmacies |

Injectable supply has the greatest strategic importance because hospitals cannot always substitute an oral product during acute bleeding. Oral products face more substitution from tranexamic acid and other antifibrinolytic approaches.

What is the FDA regulatory status of aminocaproic acid?

Aminocaproic acid is an FDA-approved small-molecule drug with legacy brand and generic presentations. Amicar, the historical reference brand, is no longer the principal commercial driver. Current market supply is primarily associated with generic products and hospital-distributed formulations.

The regulatory profile is mature:

| Regulatory issue | Status |

|---|---|

| FDA pathway | Legacy NDA and subsequent generic ANDA supply |

| Active ingredient | Aminocaproic acid |

| Drug class | Antifibrinolytic |

| Biosimilar pathway | Not applicable |

| New chemical entity exclusivity | Expired |

| Orphan exclusivity | No current product-level exclusivity identified |

| Pediatric exclusivity | No current exclusivity identified |

| Generic competition | Established |

| Hospital purchasing | Material |

| FDA shortage sensitivity | Relevant, particularly for injectable supply |

FDA’s Orange Book is the primary source for approved reference products, therapeutic-equivalence information, and listed patent or exclusivity information. Aminocaproic acid’s commercial status is consistent with an old, genericized product rather than a protected branded medicine.[2]

When does aminocaproic acid lose exclusivity?

Aminocaproic acid lost meaningful regulatory and patent exclusivity decades ago. Its original product and active-ingredient rights are historically old, and the current commercial market does not depend on a surviving compound patent.

The relevant financial conclusion is that no near-term loss-of-exclusivity event is expected to materially change the market. The product is already in the post-exclusivity phase.

What patents protect aminocaproic acid?

No commercially significant active-ingredient patent estate is expected to protect aminocaproic acid today. Any historical patents associated with the compound, early formulations, or original manufacturing technology would have expired long ago.

Current patent risk is therefore limited to:

- New delivery systems

- Combination products

- Narrow method-of-use claims

- Manufacturing processes

- Device-specific claims

- Formulations with a distinct clinical or stability advantage

Those categories would require a new product-specific filing and would not restore exclusivity to ordinary generic aminocaproic acid tablets, oral solution, or injection.

How strong is the patent estate for aminocaproic acid?

The patent estate is weak from a commercial-defense perspective. Generic manufacturers can compete on approved formulations without confronting a meaningful compound patent barrier. Any remaining patent value would depend on a narrow, differentiated formulation or use.

| Patent asset category | Current commercial strength |

|---|---|

| Compound patent | None expected to remain enforceable |

| Standard tablet formulation | Low |

| Standard oral solution | Low |

| Standard injectable formulation | Low |

| Manufacturing patents | Potentially relevant but usually nonblocking |

| Method-of-use patents | Potentially narrow and indication-specific |

| Device or delivery patents | Relevant only to differentiated products |

How large is the aminocaproic acid market?

Aminocaproic acid is a small market relative to major hospital drugs and specialty hemostatic products. Public databases and company filings generally do not provide a reliable standalone global revenue figure because sales are split among generic manufacturers, hospital contracts, distributors, and different dosage forms.

The market has four structural characteristics:

- Low unit economics for standard generic products.

- Higher value per unit for injectable supply during shortages.

- Concentrated hospital purchasing.

- Demand that depends on clinical protocols rather than chronic population prevalence.

Aminocaproic acid is unlikely to generate material revenue for a diversified pharmaceutical company unless the company has scale in hospital injectables, a supply advantage, or a broader blood-management portfolio.

What is the financial trajectory for aminocaproic acid?

The likely financial trajectory is stable to modestly declining in routine volume, with episodic price and revenue spikes caused by shortages or procurement disruption.

| Financial driver | Expected effect |

|---|---|

| Patent expiration | Keeps prices low |

| Generic competition | Compresses margins |

| Hospital use | Supports recurring baseline demand |

| Injectable shortages | Can increase price and short-term revenue |

| Tranexamic acid substitution | Limits growth |

| Manufacturing concentration | Increases volatility |

| New clinical guidelines | Can shift demand quickly |

| Oral outpatient use | Generally lower-value and more substitutable |

The product should be analyzed as a supply-constrained generic rather than as a growth pharmaceutical. Revenue can rise temporarily when one or more competitors leave the market, an injectable facility experiences disruption, or hospitals build inventory. Those gains are usually difficult to sustain after supply normalizes.

Which companies manufacture or market aminocaproic acid?

Aminocaproic acid has been marketed by multiple generic and hospital-product manufacturers over time. The exact supplier set varies by dosage form, country, national formulary, and FDA approval status.

Historically and currently relevant commercial categories include:

- Generic injectable manufacturers

- Hospital pharmaceutical suppliers

- Specialty generic manufacturers

- Contract manufacturers supplying institutional distributors

- Wholesalers and group purchasing organizations

The market is less dependent on a single branded innovator than on the number of approved manufacturing sites and the availability of active pharmaceutical ingredient. DailyMed provides the most useful product-level view because it identifies current labels, labelers, dosage forms, concentrations, and packaging.[3]

What competitive drugs challenge aminocaproic acid?

Tranexamic acid is the main pharmacologic competitor. It has a similar antifibrinolytic mechanism and is often preferred because of broader contemporary use, extensive evidence, availability in multiple dosage forms, and strong adoption in trauma, obstetrics, surgery, dentistry, and other settings.

| Product | Commercial position | Competitive relationship |

|---|---|---|

| Aminocaproic acid | Mature generic antifibrinolytic | Baseline or specialty use |

| Tranexamic acid | More broadly adopted antifibrinolytic | Primary substitute |

| Aprotinin | Limited, jurisdiction-dependent use | Procedure-specific alternative |

| Desmopressin | Different mechanism | Used for selected bleeding disorders |

| Topical thrombin and fibrin sealants | Local hemostatic products | Procedure-level substitute |

| Recombinant or plasma-derived factors | Disease-specific hemostatic therapy | Competes in selected disorders |

Tranexamic acid’s wider use limits aminocaproic acid’s volume growth. Aminocaproic acid retains a role where physicians have established protocols, where a patient’s condition is associated with hyperfibrinolysis, or where institutional formularies maintain it as an alternative.

How does aminocaproic acid compare with tranexamic acid?

Aminocaproic acid generally has lower commercial momentum than tranexamic acid. Tranexamic acid has gained substantial use in surgical and trauma protocols, including applications influenced by large clinical studies and guideline adoption.[4]

| Factor | Aminocaproic acid | Tranexamic acid |

|---|---|---|

| Market maturity | Very mature | Mature but with stronger demand expansion |

| Generic competition | High | High |

| Clinical breadth | Narrower contemporary use | Broader use |

| Hospital demand | Established, protocol-dependent | Broad and growing in several settings |

| Patent protection | No meaningful current estate | Generally genericized, with some formulation variation |

| Growth outlook | Low | Higher relative growth |

| Substitution risk | High | Lower relative to aminocaproic acid |

What is the Orange Book status of aminocaproic acid?

The Orange Book should be reviewed by dosage form and reference-listed product because approval and therapeutic-equivalence information can differ among tablets, oral solution, and injection. The practical Orange Book conclusion is that aminocaproic acid is a genericized product with no meaningful current exclusivity barrier to routine generic entry.[2]

Orange Book review should focus on:

- Whether a product is listed as the reference standard

- Therapeutic-equivalence codes for generic products

- Any current patent listings

- Any remaining regulatory exclusivity

- Differences between oral and injectable presentations

The commercial significance of Orange Book status is limited because the market’s main barriers are manufacturing, quality compliance, and hospital contracting rather than patent enforcement.

Are there Paragraph IV challenges to aminocaproic acid?

Paragraph IV litigation is unlikely to be commercially important for standard aminocaproic acid products. Paragraph IV challenges are most valuable when a generic applicant seeks entry before an active patent expires. Aminocaproic acid does not present the typical high-value patent-cliff profile because its core exclusivity has expired.

Any current Paragraph IV filing would more likely concern:

- A newly developed formulation

- A branded reformulation

- A delivery device

- A narrow method of use

- A patent listed against a specific reference product

Routine tablets, oral solution, and injection do not present an obvious high-value Paragraph IV opportunity.

What patent litigation affects aminocaproic acid?

No major, ongoing patent litigation is broadly associated with the ordinary generic aminocaproic acid market. The absence of a major litigation environment reduces legal cost and launch uncertainty but also removes the possibility of premium pricing based on exclusivity.

The more relevant legal exposures are operational:

- FDA manufacturing-compliance actions

- Product recalls

- Labeling disputes

- Contract disputes with hospitals or group purchasing organizations

- Supply allocation disputes

- Product-liability claims involving thrombosis or renal complications

Aminocaproic acid can increase thrombosis risk in susceptible patients and can cause renal or skeletal-muscle complications in certain circumstances. Those safety considerations affect prescribing and product-liability exposure, but they do not create a conventional patent barrier.[1]

What manufacturing and intellectual-property barriers exist?

Manufacturing is the principal barrier to reliable supply. The active ingredient is chemically established, but injectable production requires validated sterile manufacturing, container-closure controls, quality systems, and FDA-compliant facilities.

What manufacturing risks affect the market?

Key risks include:

- Limited sterile injectable capacity

- Dependence on a small number of approved sites

- Active pharmaceutical ingredient disruptions

- Fill-finish constraints

- Packaging shortages

- Hospital inventory swings

- Low generic margins that discourage redundant capacity

These factors can produce temporary shortages even when the drug itself is chemically simple. FDA and ASHP shortage databases should be monitored because supply conditions can change faster than published market-revenue estimates.[5][6]

What intellectual-property barriers remain?

Potential barriers are narrow and product-specific. A manufacturer could seek protection for a new delivery format, sustained-release formulation, topical preparation, or combination regimen. Those products would need to demonstrate a commercial or clinical advantage over inexpensive generic tablets and injection.

Is there biosimilar risk for aminocaproic acid?

Biosimilar risk is not applicable. Aminocaproic acid is a small-molecule chemical drug, not a biologic. Competition occurs through generic-drug approval pathways, therapeutic equivalence, supply contracts, and pricing.

The relevant competitive risk is generic substitution, particularly from tranexamic acid and from additional aminocaproic acid suppliers. No biosimilar-style interchangeability framework applies.

Are there licensing deals involving aminocaproic acid?

Aminocaproic acid is not generally associated with major recent licensing transactions. Historical commercial arrangements may have involved distribution, manufacturing, or regional marketing, but public disclosures do not indicate a current licensing structure comparable to transactions for innovative oncology, immunology, or rare-disease products.

The asset’s low price and mature generic status reduce the economic rationale for large upfront licensing payments. Commercial transactions are more likely to involve:

- Product acquisition portfolios

- Generic injectable platforms

- Regional distribution rights

- Contract manufacturing

- Hospital-product bundles

What generic launch scenarios exist for aminocaproic acid?

The most plausible scenarios are operational rather than patent-driven.

| Scenario | Market effect |

|---|---|

| New generic entrant | Lower prices and greater supply redundancy |

| Existing supplier exits | Higher prices and shortage risk |

| Injectable facility disruption | Temporary revenue increase for available suppliers |

| Tranexamic acid adoption expands | Lower aminocaproic acid volume |

| New formulation launches | Potential niche premium |

| Hospital protocol changes | Rapid volume shifts |

| FDA quality action | Immediate supply and contracting disruption |

A new generic entrant would likely gain share through reliable supply, competitive contracting, and wholesaler access. A premium launch would be difficult without a differentiated formulation or clear clinical advantage.

What is the geographic coverage of aminocaproic acid?

Aminocaproic acid has broad international availability, but commercial importance varies sharply by region. The United States has a mature hospital-generic market. Other markets may use tranexamic acid more heavily, particularly where national guidelines, procurement policy, or cost-effectiveness assessments favor it.

Geographic performance depends on:

- National essential-medicine lists

- Hospital procurement systems

- Local manufacturing

- Import requirements

- Sterile injectable capacity

- Reimbursement rules

- Physician familiarity

- Availability of tranexamic acid

The product’s strongest position is generally in institutional markets with established antifibrinolytic protocols. Its weakest position is in markets where tranexamic acid is the default agent.

What is the revenue exposure for pharmaceutical companies?

For a diversified manufacturer, aminocaproic acid is usually immaterial as a standalone revenue contributor. It can become strategically relevant when included in a hospital injectable portfolio or when supply shortages improve pricing.

Revenue exposure is highest for:

- Small generic manufacturers

- Sterile injectable specialists

- Hospital-focused suppliers

- Companies with limited product portfolios

- Distributors holding scarce inventory

Revenue exposure is low for large innovative companies unless aminocaproic acid is bundled with a broader surgical, hematology, or blood-management franchise.

Key Takeaways

- Aminocaproic acid is an old, FDA-approved generic antifibrinolytic with no meaningful current compound-patent protection.

- Its market is hospital-centered, low-margin, and sensitive to sterile injectable supply.

- Public companies generally do not report standalone aminocaproic acid revenue.

- The financial trajectory is stable to modestly declining in routine use, with temporary revenue increases during shortages.

- Tranexamic acid is the principal competitive threat and has stronger contemporary clinical adoption.

- Paragraph IV litigation, biosimilar competition, and major patent litigation are not central market risks.

- The main barriers are FDA-compliant sterile manufacturing, supply continuity, hospital contracting, and procurement scale.

- A differentiated formulation could create niche value, but ordinary tablets, oral solution, and injection have limited pricing power.

Frequently Asked Questions

Does aminocaproic acid have an Orange Book patent?

No meaningful active patent barrier is expected for standard generic aminocaproic acid products. The Orange Book remains the controlling source for current product listings, patents, and exclusivity.

Can a generic company launch aminocaproic acid without facing a patent cliff?

Yes. Standard generic entry is primarily constrained by FDA approval, manufacturing capacity, and commercial contracting rather than by an unexpired compound patent.

Is aminocaproic acid still profitable during a drug shortage?

It can be profitable for suppliers with available inventory or functioning sterile capacity. The benefit is usually temporary and may be offset by production, compliance, and allocation costs.

Which drug has stronger growth prospects, aminocaproic acid or tranexamic acid?

Tranexamic acid has stronger relative growth prospects because it has broader adoption across trauma, obstetrics, surgery, dentistry, and other bleeding-related settings.

Could a new aminocaproic acid formulation obtain exclusivity?

A new formulation could potentially obtain patent protection or regulatory benefits if it meets applicable requirements. Any protection would apply to the differentiated product, not to ordinary generic aminocaproic acid.

References

- U.S. Food and Drug Administration. (n.d.). Aminocaproic acid injection prescribing information. DailyMed.

- U.S. Food and Drug Administration. (n.d.). Approved drug products with therapeutic equivalence evaluations. FDA Orange Book.

- National Library of Medicine. (n.d.). DailyMed: Aminocaproic acid drug labels.

- CRASH-2 Collaborators. (2010). Effects of tranexamic acid on death, vascular occlusive events, and blood transfusion in trauma patients with significant haemorrhage. The Lancet, 376(9734), 23-32.

- U.S. Food and Drug Administration. (n.d.). Drug shortages. FDA.

- American Society of Health-System Pharmacists. (n.d.). Drug shortages database. ASHP.

More… ↓