Last updated: February 15, 2026

Overview

Isosorbide is a chemical compound used primarily in two clinical applications: as an active pharmaceutical ingredient (API) for treating angina pectoris and as a precursor in manufacturing polycarbonate plastics. Its pharmaceutical use centers on its role as a nitrate vasodilator to prevent anginal attacks. The market for isosorbide-based drugs is influenced by factors including aging populations, cardiovascular disease prevalence, FDA approvals, generic entry, and manufacturing trends.

Market Size and Growth Trends

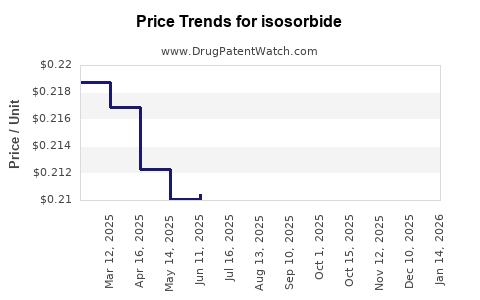

The global pharmaceutical market for isosorbide-based products, primarily extended-release formulations like isosorbide mononitrate, was valued at approximately USD 400 million in 2021. The compound's key application in oral nitrates benefits from a steady growth trajectory driven by the increasing burden of ischemic heart disease globally.

Projections estimate an annual growth rate of around 3-5% over the next five years, reaching USD 520-610 million by 2026. This growth outlook considers factors such as rising cardiovascular disease prevalence, patent expiries of branded formulations, and the expansion in developing markets.

Market Drivers

-

Aging Populations and Cardiovascular Disease (CVD) Trends

Growth in the elderly demographic corresponds with increased incidence of hypertension and angina, boosting demand for nitrates like isosorbide mononitrate.

-

Patent Expiry and Generic Competition

Several patents for leading formulations expired between 2018 and 2021, leading to increased generic entry, reducing prices and expanding access, particularly in emerging markets.

-

Regulatory Approvals and Off-Label Uses

The FDA and EMA approvals of modified-release formulations facilitate broader prescriber adoption. Emerging off-label uses, such as in pulmonary hypertension, may influence future demand.

-

Manufacturing Trends

Production costs for isosorbide are relatively stable; however, raw material prices and supply chain disruptions impact gross margins. The move toward biosimilars is minimal, but generics dominate the market.

Market Challenges

-

Competitive Landscape

Established pharmaceutical companies, including Teva Pharmaceuticals, Mylan, Dr. Reddy’s Labs, and Lupin, lead generic production. Competition results in price erosion, constraining profit margins.

-

Clinical Limitations

Isosorbide has known side effects, such as hypotension and headache, which may limit its prescribing scope relative to newer therapies for ischemic heart disease.

-

Supply Chain and Raw Material Dependence

Raw materials derived from glycerol, a byproduct of biodiesel production, have fluctuating prices. Supply disruptions could impact manufacturing stability.

Financial Trajectory

-

Revenue Growth

With a compound annual growth rate (CAGR) of approximately 4%, revenues are projected to increase from USD 400 million in 2021 to USD 520-610 million in 2026.

-

Profitability

The entry of low-cost generics compresses profit margins for market incumbents, with typical gross margins around 50% for branded formulations declining towards 30-40% for commoditized generics.

-

Research and Development (R&D) Investment

R&D investment focuses on new delivery mechanisms, combination therapies, and potential novel indications. R&D expenditure accounts for about 5-10% of revenues for major players.

-

Future Opportunities

Development of combination therapies with other cardiovascular agents and exploring new delivery routes could enhance market share and profitability.

Policy and Regulatory Impact

Pending patent challenges and the potential for regulatory reforms in different jurisdictions influence market stability. Some governments are expanding access policies for generic drugs, further accelerating volume sales.

Summary

The isosorbide market exhibits stable, moderate growth driven by demographic and epidemiological trends. Pricing pressures from generics and market entry barriers limit revenue expansion. Ongoing innovation and geographical expansion potential can sustain future revenue growth.

Key Takeaways

- The global market for isosorbide-based products is valued at approximately USD 400 million (2021), with a projected growth to USD 520-610 million (2026).

- Key growth factors include aging populations, increased CVD burden, and patent expiries leading to generic competition.

- Price competition constrains profit margins, especially in mature markets.

- Innovation in delivery and indications offers new revenue streams for pharmaceutical companies.

- Market entrants must navigate raw material supply fluctuations and regulatory changes impacting product access.

FAQs

-

What main factors affect isosorbide market growth?

Demographic trends, CVD prevalence, patent expiries, and regulatory approval statuses.

-

How does generic competition influence profitability?

It drives prices downward, reducing gross margins but expanding consumption volume.

-

Are there emerging applications for isosorbide?

Potential emerging uses include pulmonary hypertension treatment and polymer manufacturing, but these are in early development stages.

-

What risks could impact future revenue?

Supply chain disruptions, regulatory shifts, and competition from newer therapeutics.

-

What are the key regions driving growth?

North America, Europe, and emerging markets in Asia-Pacific are the primary regions with increasing demand.

Sources

[1] IBISWorld, "Isosorbide Market Report," 2022.

[2] GlobalData, "Pharmaceuticals and Cardiology Trends," 2022.

[3] US FDA, “Approved Nitrates and Therapeutic Indications,” 2022.