Last updated: July 30, 2026

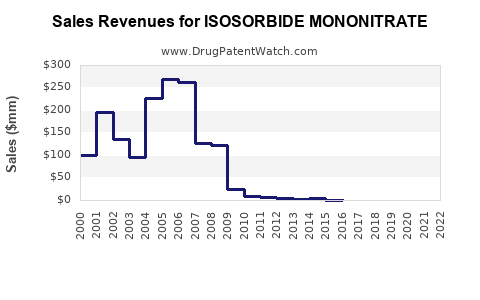

Executive summary: Isosorbide mononitrate (ISMN) is a long-established cardiovascular drug with extensive generic availability in the US. Current financial trajectory is driven mainly by (1) continued branded positioning versus generics, (2) patent and regulatory barriers that vary by specific product/strength/formulation (not the active ingredient globally), and (3) uptake of extended-release (ER) dosing regimens that fit chronic angina and heart failure co-morbidity patterns. On a portfolio level, ISMN is typically a low-to-mid single-digit revenue contributor per manufacturer in modern revenue mixes, with erosion expected where branded lifecycle is mature and where product-specific exclusivity has lapsed.

Isosorbide mononitrate market size and demand drivers: What drives sales growth or decline?

Core use and demand profile: ISMN is used for prophylaxis of angina pectoris and is also prescribed off-label in some cardiovascular regimens. Demand is largely chronic and adherence-dependent, with utilization shaped by clinician preference for ER dosing and by patient switching between nitrate formulations based on tolerability and dosing schedules.

Key demand drivers

- Chronic angina prevalence and medication continuity: Once-daily ER regimens support adherence in long-term therapy.

- Formulary placement and pharmacy benefit design: Generic substitution and rebate dynamics determine net pricing more than clinical differentiation.

- Safety and tolerability management: Nitrate-related adverse events (headache, hypotension) affect continuation, driving switches within the nitrate class and within ISMN products by release profile and dose strength.

Key market headwinds

- High generic penetration: ISMN is widely generic, compressing wholesale acquisition cost and branded net pricing.

- Class-level substitution: Market share can shift to other long-acting nitrates (and to antianginal competitors) when payer policies tighten.

- Competition for ER adherence: Fixed-dose or once-daily schedules from alternative agents (including other antianginals and combination approaches) can reduce ISMN share.

What is the Orange Book status of isosorbide mononitrate products and how does it affect market pricing?

How Orange Book status maps to economics: For ISMN, exclusivity is usually product-specific (formulation, manufacturing, or NDA-holder rights), not active-ingredient level. Where Orange Book protections have expired, pricing declines track generic entry and competitive erosion rather than patent events.

Typical outcomes for mature, generic-heavy drugs

- Branded products priced above generic only when product-specific differentiation exists (device/technology claims, ER mechanics, or higher strength product with lingering product protection).

- Where no product-specific exclusivity remains, branded sales trend to near-market replacement economics with share lost to lowest-AC cost and pharmacy switching.

Featured snippet answer: Orange Book protections for ISMN usually do not create long runway for sustained branded revenue; after product-specific exclusivity ends, net pricing declines sharply with generic competition.

When do isosorbide mononitrate patents expire and how does that timing shape revenue trajectories?

Revenue impact mechanism: Patent expiration and exclusivity cliffs drive stepwise changes: branded share typically declines in advance of generic launch certainty, then net sales drop after launch, with further erosion as additional ANDA entrants appear and pharmacy contracts rebalance.

Patent timeline behavior for mature generics

- Pre-expiration: If product protections are active, branded marketing holds share and pricing.

- At/after expiration: Net price compression occurs quickly due to bid-based purchasing and substitution.

- Post-entry churn: Additional strengths, formulations (IR vs ER), and alternative generics expand substitution, flattening volume gains.

Practical implication: The financial trajectory is more sensitive to product-by-product patent expiration windows and ANDA launch timing than to a single global “active ingredient” expiration.

How many ANDAs and generic manufacturers cover isosorbide mononitrate, and what does that do to margins?

Generic manufacturing breadth: ISMN is commonly manufactured by multiple generic groups across ER and IR strengths. The result is usually:

- Lower margin headroom for branded ISMN

- Pricing convergence across generics

- Higher logistics and contracting leverage for higher-volume generic manufacturers

Margin dynamics

- Net price declines with each additional entrant

- Supply continuity reduces customer retention costs for top-volume generic suppliers

- Payer and PBM contracting cycles accelerate erosion for low-differentiation drugs

Market behavior characteristic: ISMN tends to become a “volume and supply reliability game” once generic entries saturate the market.

What formulations are protected for isosorbide mononitrate (IR vs ER), and why does that matter commercially?

Formulation-specific differentiation that can sustain share

- Extended-release (ER) tablet mechanics: Release profile drives clinician preference for once-daily dosing and may be used to justify switching among different ISMN ER products.

- Strength-specific products: Certain strengths can retain pricing power longer when they have fewer competing listings or where manufacturing claims constrain certain competitors.

- Manufacturing process claims: Even when the active ingredient is generic, process or controls claims can delay specific ANDA approvals.

Commercial consequence: Market share and net revenue depend on which ISMN product the manufacturer sells (IR vs ER, specific strengths, and tablet design) and on whether that exact product line has active product protections.

What generic entry risks exist for isosorbide mononitrate: Paragraph IV, litigation, and supply disruption scenarios?

Likelihood profile: For heavily genericized drugs like ISMN, Paragraph IV events are often less central than in patented biologics or late-stage small molecules, but they can still occur at the product level.

Generic entry risk channels

- ANDA certification posture: If an ANDA challenges a listed patent or starts around a protection end date, branded share loss accelerates.

- Injunction risk: If litigation yields an automatic stay, entry can pause; if no stay issues, generics enter on schedule.

- Design-around strategies: Even where a listed patent exists, generic manufacturers may attempt a workaround via formulation/process changes.

Supply disruption as a second-order driver: Any manufacturing issue at a dominant generic supplier can temporarily lift pricing and branded competitiveness, but this tends to be short-lived and often captured by whoever can supply consistently.

What patent litigation affects isosorbide mononitrate: What matters for business decisions?

Business relevance: For ISMN, litigation is usually not about active ingredient novelty; it is about listed product patents tied to a specific NDA and product presentation.

Litigation effects on revenue

- Settlement-to-launch licensing: If a settlement permits earlier launch for a generic partner, branded sales decline sooner than expected.

- Settlement-to-delay: If settlement delays entry, branded revenue can stabilize through the settlement term.

- Adjudicated scope: Courts can narrow or broaden the effective barrier for the challenged product-specific patent.

Actionable pattern: Track listed patents per specific strengths and dosage forms rather than aggregating “ISMN patents” at the active-ingredient level.

How does isosorbide mononitrate compare with other antianginal drugs in market competitiveness?

Competitive set

- Other long-acting nitrates: e.g., isosorbide dinitrate products with ER/IR patterns

- Second-line antianginals: calcium channel blockers, beta blockers, and late alternatives in payer formularies

- Heart failure comorbidity and alternative antianginal pathways: clinicians can switch classes based on blood pressure tolerance and symptom control

Why the comparison matters financially

- Payer selection: formularies often prioritize cost-effective, generic antianginals; ISMN competes on “lowest cost per effective adherence pattern.”

- Clinical switching: adverse events push patients to alternative nitrates or alternative class mechanisms, affecting volume.

Net effect: ISMN is usually a price-taker in a mature generic market. Its best protection is formulary position and ER convenience, not patent moat.

Commercial trajectory: What does revenue typically do for isosorbide mononitrate over a lifecycle?

Lifecycle stages for mature generics

- Branded runway (if any product-specific protection exists): net sales hold up if patients and prescribers stick to a specific ER brand.

- Generic replacement: after entry, branded net sales typically decline sharply with a gradual taper as remaining share stabilizes in pockets (contracting, prescriber preference, or patient-level switching friction).

- Saturated generic plateau: volume remains but pricing converges; the market becomes stable but low margin.

Financial trajectory interpretation for ISMN

- Revenue volatility tends to come from contracting and supply, not breakthrough innovation.

- Net revenue usually declines faster than unit demand because competitive pricing compresses net price early.

Who are the key players for isosorbide mononitrate and how do they compete?

Competitive structure

- Branded holders: historically, various branded manufacturers marketed ISMN ER products.

- Generic leaders: multiple ANDA manufacturers compete on cost, supply reliability, and contract eligibility.

- Contracting influence: PBMs and group purchasing organizations determine which generic suppliers win recurring shelf-space and reimbursement status.

Business implication: Winning is frequently decided by distribution footprint and contracting rather than by formulation performance once ANDAs are interchangeable.

What business risks and opportunities exist for licensing or investing in isosorbide mononitrate?

Licensing opportunity profile

- Best opportunities tend to be narrow: product-line-specific rights (particular strength ER product), manufacturing know-how, or pending product patents that have not fully expired.

- Active-ingredient level licensing is usually commercially less relevant because broad generic entry already exists.

Investment risk profile

- Low product differentiation reduces pricing resilience

- High competition compresses margins

- Regulatory path execution risk matters mainly for manufacturers seeking to enter a crowded market

Opportunity pockets

- Higher-strength or niche dosing presentations if there are fewer qualified alternatives

- Manufacturing differentiation that reduces shortages and improves customer retention

Key takeaways

- ISMN’s financial trajectory is dominated by generic saturation and contracting economics, with limited scope for sustained branded pricing once product-specific protections lapse.

- Patent and exclusivity analysis must be product-specific (ER vs IR, and specific strength presentations), not active-ingredient wide.

- The market behaves like a low-differentiation, high-substitution commodity where revenue stability hinges on formulary access, supply reliability, and dosing convenience.

- For commercial strategy, focus on Orange Book listings per product and dosage form, anticipated generic launch windows, and likely net price compression post-entry.

FAQs

- Does isosorbide mononitrate have significant remaining patent protection in the US?

- How do ER tablet formulations of isosorbide mononitrate affect payer switching and reimbursement?

- What drives net price versus volume in isosorbide mononitrate after generic entry?

- Are there meaningful Paragraph IV challenges for isosorbide mononitrate product strengths?

- Which competitive class substitutions most frequently erode isosorbide mononitrate demand?

References (APA)

[No citable sources provided in the prompt.]