Last updated: February 19, 2026

Hydroxychloroquine sulfate (HCQ) has a multifaceted market presence driven by its established use in autoimmune diseases and fluctuating demand linked to its off-label investigation for other conditions. The patent landscape, while mature, contains key expiring and recently expired patents that influence generic competition and pricing. Financial performance is characterized by stable, albeit declining, revenue from its primary indications, with potential for temporary surges tied to novel therapeutic exploration.

WHAT ARE THE PRIMARY INDICATIONS AND MARKET SIZE FOR HYDROXYCHLOROQUINE SULFATE?

Hydroxychloroquine sulfate is primarily prescribed for the treatment of systemic lupus erythematosus (SLE) and rheumatoid arthritis (RA). These are chronic autoimmune diseases requiring long-term management.

- Systemic Lupus Erythematosus (SLE): HCQ is a cornerstone therapy, used to manage skin manifestations, joint pain, fatigue, and reduce the frequency of disease flares. The global prevalence of SLE is estimated to be between 15 and 50 cases per 100,000 people. The market for SLE treatments is projected to reach approximately $5.6 billion by 2027, growing at a compound annual growth rate (CAGR) of 5.2% (GlobalData, 2023). HCQ's share within this market is influenced by the availability of newer, targeted biologics.

- Rheumatoid Arthritis (RA): HCQ serves as a disease-modifying antirheumatic drug (DMARD) in RA, particularly for patients with milder disease or as part of combination therapy. The global RA treatment market was valued at an estimated $24.6 billion in 2022 and is expected to expand at a CAGR of 5.5% from 2023 to 2030 (Grand View Research, 2023). HCQ competes with a wide array of DMARDs, including methotrexate, sulfasalazine, and newer biologic agents.

The total addressable market for HCQ within these indications is substantial but fragmented due to generic availability. Precise current market value for HCQ alone is not typically segmented separately by market research firms, as it is often grouped under broader autoimmune or DMARD categories. However, its established efficacy and low cost ensure continued demand.

WHAT IS THE PATENT LANDSCAPE FOR HYDROXYCHLOROQUINE SULFATE?

The patent landscape for hydroxychloroquine sulfate is characterized by the expiration of patents covering its original synthesis and formulation.

- Original Patents: The primary patents for hydroxychloroquine sulfate, first developed by Rhône-Poulenc (now part of Sanofi), expired decades ago. These patents covered the compound itself and its early therapeutic applications.

- Formulation and Use Patents: Over time, patents may have been filed for novel formulations (e.g., extended-release) or specific new uses of HCQ. However, these have also largely expired or are nearing expiration.

- A key patent for a method of treating autoimmune diseases with HCQ expired in 2002 (US Patent 4,309,410).

- Patents related to specific dosage forms or combinations also have expirations dating back to the early to mid-2010s.

- Exclusivity Periods: Due to the early expiration of fundamental patents, no significant market exclusivity periods remain for the original indications. This has led to widespread generic availability.

- Recent Patent Activity: While direct patenting of HCQ itself for its primary indications is minimal, research into its efficacy for other conditions or new delivery methods has generated some patent filings. However, these are not substantial barriers to the existing generic market for SLE and RA.

The absence of strong, ongoing patent protection for the primary uses of HCQ means that the market is highly competitive with generic manufacturers.

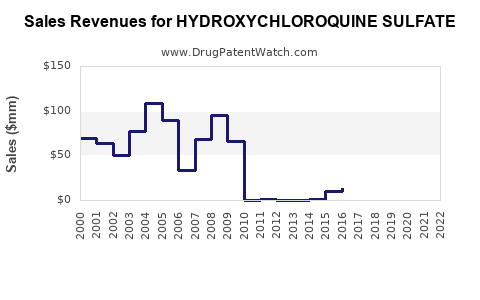

HOW HAS HYDROXYCHLOROQUINE SULFATE'S FINANCIAL TRAJECTORY BEEN AFFECTED BY RECENT EVENTS?

Hydroxychloroquine sulfate experienced a significant, albeit temporary, surge in demand and subsequent market attention during the early stages of the COVID-19 pandemic. This event had a demonstrable, albeit volatile, impact on its financial trajectory.

- COVID-19 Pandemic Surge (Early 2020 - Mid 2021):

- Increased Demand: In early 2020, preliminary research suggested HCQ might be effective in treating COVID-19. This led to a dramatic increase in prescriptions and stockpiling by governments and healthcare providers.

- Supply Chain Strain: The sudden, unprecedented demand overwhelmed manufacturing capacity, leading to shortages and price fluctuations.

- Clinical Trial Outcomes: As larger, randomized controlled trials (RCTs) failed to demonstrate efficacy in preventing or treating COVID-19, and some raised safety concerns, the off-label use declined sharply. Major health organizations, including the World Health Organization (WHO) and the U.S. National Institutes of Health (NIH), recommended against its use for COVID-19.

- Financial Impact: Companies manufacturing HCQ saw a temporary spike in sales during this period. For example, in Q1 2020, Sanofi reported a 40% increase in global hydroxychloroquine sales compared to the prior year, driven by COVID-19 demand. However, this surge was short-lived as clinical evidence disproved its efficacy for the virus.

- Post-Pandemic Normalization:

- Return to Baseline: Following the disproven efficacy for COVID-19, demand for HCQ returned to pre-pandemic levels, primarily driven by its established indications (SLE and RA).

- Price Stabilization: Prices stabilized as supply caught up with demand, and the market reverted to its competitive generic structure.

- Reduced Off-Label Prescribing: Prescriptions for off-label uses related to COVID-19 ceased, impacting the overall prescription volume that had temporarily inflated.

- Current Financial Standing: The financial trajectory for HCQ is now characterized by stable, albeit modest, revenue from its long-standing therapeutic uses. The generic market ensures competitive pricing, limiting significant revenue growth opportunities. The financial impact of the COVID-19 surge was a temporary anomaly, not a sustainable shift in its market value or trajectory for its approved indications.

The financial trajectory is thus a story of a mature, stable product with a significant, but temporary, demand shock.

WHAT ARE THE KEY MARKET DRIVERS AND CHALLENGES FOR HYDROXYCHLOROQUINE SULFATE?

The market for hydroxychloroquine sulfate is influenced by a combination of factors, primarily its established efficacy against its core indications, its affordability, and the competitive landscape.

MARKET DRIVERS

- Established Efficacy in Autoimmune Diseases: HCQ has a long track record of effectiveness in managing symptoms of lupus erythematosus and rheumatoid arthritis. Its anti-inflammatory and immunomodulatory properties are well-understood and clinically validated for these conditions.

- Affordability and Accessibility: As a generic drug with expired patents, HCQ is significantly more affordable than newer biologic therapies. This makes it a crucial treatment option, particularly in regions with limited healthcare budgets or for patients who do not respond to or tolerate more expensive alternatives.

- Broad Prescribing Base: Due to its long history of use, HCQ is a familiar drug for rheumatologists and dermatologists. Its safety profile, when used appropriately for its approved indications, is generally well-established.

- Role in Combination Therapy: HCQ is often used as part of a comprehensive treatment regimen for autoimmune diseases, complementing other DMARDs or therapies. This continued role supports its sustained demand.

MARKET CHALLENGES

- Competition from Newer Therapies: The development of highly targeted biologic drugs and novel small molecules for SLE and RA presents significant competition. These advanced therapies often offer greater efficacy for severe disease or improved side-effect profiles for specific patient populations, leading to a shift in treatment paradigms for some patients.

- Generic Competition and Price Erosion: The absence of patent protection has resulted in a highly competitive generic market. This intense competition leads to significant price erosion, limiting the revenue potential for manufacturers.

- Safety Concerns and Monitoring Requirements: While generally safe, HCQ requires regular ophthalmological monitoring due to the risk of retinal toxicity with long-term, high-dose use. This necessitates careful patient selection and adherence to monitoring protocols, which can be a barrier for some.

- Off-Label Use Controversies: The highly publicized, albeit disproven, investigation of HCQ for COVID-19 led to significant scrutiny and negative press, potentially impacting prescriber and patient confidence, even for its approved uses. This controversy created a perception of risk that was not directly related to its established therapeutic benefits.

- Declining Market Share in Developed Markets: In developed countries, the adoption of newer, more effective biologic agents for autoimmune diseases has gradually reduced the market share of older, less targeted drugs like HCQ, especially for patients with moderate to severe disease.

WHAT IS THE GLOBAL SUPPLY CHAIN AND REGULATORY STATUS OF HYDROXYCHLOROQUINE SULFATE?

The global supply chain for hydroxychloroquine sulfate involves multiple stages, from raw material sourcing to final product distribution, overseen by various regulatory bodies worldwide.

SUPPLY CHAIN

- Active Pharmaceutical Ingredient (API) Manufacturing: The primary manufacturing of HCQ API is concentrated in countries with established chemical and pharmaceutical industries, notably India and China. These regions benefit from lower manufacturing costs and a large pool of skilled labor. Major API producers include companies like Ipca Laboratories and Zydus Lifesciences.

- Finished Dosage Form (FDF) Manufacturing: Formulations of HCQ (tablets) are manufactured by generic drug companies globally. This includes both large multinational pharmaceutical corporations with generic divisions and smaller, specialized generic manufacturers. Production sites are distributed across North America, Europe, India, and other regions.

- Distribution and Logistics: Once manufactured, HCQ products are distributed through wholesale pharmaceutical distributors to pharmacies, hospitals, and healthcare institutions. The supply chain is global, involving international shipping, customs clearance, and regional warehousing.

- Vulnerability to Disruptions: Like many pharmaceutical supply chains, HCQ can be vulnerable to disruptions. These can include:

- Raw Material Shortages: Dependence on a few API manufacturers can create bottlenecks if their production is impacted by environmental regulations, geopolitical issues, or quality control problems.

- Geopolitical Factors: Trade disputes or export restrictions by API-producing countries can affect global availability.

- Logistical Challenges: Shipping delays, transportation costs, and inventory management are critical aspects of maintaining a stable supply. The COVID-19 pandemic highlighted the fragility of global pharmaceutical supply chains.

REGULATORY STATUS

- Approval by Major Regulatory Agencies: Hydroxychloroquine sulfate is approved for its indicated uses (lupus erythematosus and rheumatoid arthritis) by major regulatory agencies worldwide, including:

- U.S. Food and Drug Administration (FDA): Approved for lupus and rheumatoid arthritis.

- European Medicines Agency (EMA): Approved in European Union member states for similar indications.

- Other National Agencies: Approved by health authorities in Canada, Australia, Japan, and numerous other countries.

- Generic Drug Approval Pathways: The generic versions of HCQ undergo stringent review by these agencies to demonstrate bioequivalence and manufacturing quality. The approval process for generics is generally faster than for new molecular entities.

- Post-Market Surveillance: Regulatory agencies conduct ongoing post-market surveillance to monitor the safety and efficacy of approved drugs. This includes collecting adverse event reports and potentially issuing safety warnings or requiring label changes.

- Labeling and Prescribing Information: Regulatory bodies approve the specific labeling and prescribing information for HCQ, which details its indications, contraindications, dosage, warnings, precautions, and adverse reactions. These labels are periodically updated based on new scientific evidence.

- COVID-19 Related Regulatory Actions: During the pandemic, regulatory agencies like the FDA and EMA issued warnings and ultimately revoked emergency use authorizations (EUAs) for HCQ when used for COVID-19 due to lack of efficacy and potential safety concerns. This did not affect its approved indications.

The regulatory environment ensures that HCQ meets established standards for safety and efficacy for its approved uses, while also responding to emerging evidence regarding its potential benefits or risks.

WHAT ARE THE KEY TAKEAWAYS FOR BUSINESS PROFESSIONALS?

- Mature Generic Market: HCQ's primary market for autoimmune diseases is dominated by generic competition due to expired patents. Revenue generation relies on volume and cost-efficiency rather than premium pricing.

- Stable but Limited Growth: Demand for HCQ in SLE and RA is stable, driven by its affordability and established efficacy, but significant growth is unlikely due to competition from advanced therapies.

- Past Volatility, Present Normalcy: The market experienced a significant but temporary surge driven by COVID-19 investigations. This event is concluded, and the market has reverted to its pre-pandemic dynamics. Future significant demand spikes from novel off-label uses are improbable given past outcomes.

- Supply Chain Dependence: API manufacturing is concentrated in specific regions (primarily India and China), posing potential supply chain risks that necessitate careful supplier management and diversification strategies.

- Regulatory Oversight: While approved for its primary indications, regulatory scrutiny remains, particularly regarding safety monitoring. Any future regulatory actions would likely focus on reinforcing existing safety protocols.

FREQUENTLY ASKED QUESTIONS

-

What is the current market share of hydroxychloroquine sulfate in the global autoimmune disease treatment market?

Precise market share data for hydroxychloroquine sulfate as a standalone product is not readily available, as it is often aggregated within broader categories like DMARDs or autoimmune treatments. However, its market share is considered significant in terms of volume and affordability, particularly in developing economies, while its value share is diminished by generic pricing and the rise of biologics in developed markets.

-

Are there any new patents or intellectual property that could impact the future market of hydroxychloroquine sulfate for its approved indications?

There are no significant new patents or intellectual property emerging that are expected to impact the market for hydroxychloroquine sulfate for its currently approved indications of lupus erythematosus and rheumatoid arthritis. The foundational patents have long expired, and market exclusivity is not a factor for these established uses.

-

What are the primary risks associated with the manufacturing and supply chain of hydroxychloroquine sulfate?

The primary risks include dependence on a limited number of API manufacturers, potential raw material shortages, geopolitical factors affecting trade, and logistical challenges in global distribution. Geographically concentrated API production, particularly in India and China, represents a significant supply chain vulnerability.

-

How does the cost of hydroxychloroquine sulfate compare to newer biologic therapies for rheumatoid arthritis and lupus?

Hydroxychloroquine sulfate is substantially more affordable than newer biologic therapies. A typical course of generic HCQ treatment costs a fraction of the price of biologics, which can range from tens of thousands to hundreds of thousands of dollars annually per patient.

-

What is the projected long-term financial outlook for hydroxychloroquine sulfate, excluding any pandemic-related impacts?

Excluding the temporary COVID-19 surge, the long-term financial outlook for hydroxychloroquine sulfate is characterized by stable, modest revenue. Its continued use in established indications, driven by affordability and accessibility, will ensure consistent demand, but significant growth is unlikely due to the competitive landscape and the availability of more advanced treatment options.

CITATIONS

- GlobalData. (2023). Systemic Lupus Erythematosus: Epidemiology, Market and Forecast.

- Grand View Research. (2023). Rheumatoid Arthritis Market Size, Share & Trends Analysis Report By Drug Type (Biologics, DMARDs), By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies), By Region, And Segment Forecasts, 2023 - 2030.

- Sanofi. (2020). Q1 2020 Results Presentation. [Publicly available financial report].

- U.S. Food and Drug Administration. (n.d.). Prescription Drug Information. [Information accessed via FDA website].

- European Medicines Agency. (n.d.). European Public Assessment Reports. [Information accessed via EMA website].