Last updated: April 25, 2026

Zantac (ranitidine) moved from blockbuster peak revenues to rapid, compounding revenue collapse after NDMA contamination allegations and regulatory actions in 2019. The commercial outcome was defined by (1) abrupt demand destruction across major geographies, (2) formal product withdrawals and regulatory restrictions, and (3) aggressive settlement and litigation cost accruals that compressed financial profiles for the branded manufacturer and distributors.

What was the market structure behind Zantac’s demand?

Zantac was a branded histamine-2 (H2) blocker used for gastroesophageal reflux disease (GERD), peptic ulcer disease, and related indications. Market dynamics were dominated by three features:

- Generic erosion before the NDMA event: Like other legacy acid-suppression brands, Zantac faced structural pressure from generic ranitidine entering earlier. Branded share persisted because of formulary familiarity, patient switching costs, and brand-led marketing, but pricing and volume growth were constrained.

- Retail and channel concentration: Zantac was widely distributed through major retail pharmacies and wholesalers, making it highly exposed to rapid “pull” decisions once regulators moved.

- Regulatory sensitivity tied to contamination risk: NDMA contamination reframed ranitidine from a standard OTC/rx commodity to a product-risk liability. That shifted buying behavior from price sensitivity to safety verification and substitute switching.

Net effect: even modest regulatory escalation had outsized financial impact because the product sat at scale in distribution networks and faced immediate channel restrictions once contamination was taken seriously.

How did regulatory events change the market overnight?

The NDMA issue changed Zantac’s trajectory through rapid regulatory action and escalating evidence thresholds. The key milestones:

| Date |

Event |

Market impact mechanism |

| Apr 2019 |

FDA identifies NDMA as a likely human carcinogen and requests ranitidine manufacturers to stop sale/use and investigate NDMA levels |

Safety-driven demand shock; manufacturer and channel uncertainty |

| Apr 2019 (later in 2019) |

FDA issues limits and advisories; regulators in other jurisdictions initiate actions |

Cross-border withdrawal risk increases |

| Sep 2019 |

FDA requests firms withdraw ranitidine products from the market |

Formal withdrawal accelerates inventory depletion and substitution |

| Oct 2019 |

Major jurisdictions move toward removal of ranitidine products from shelves |

Retail access collapses |

| 2020 and after |

Litigation and settlements intensify; residual inventory and remaining formulations wind down |

Revenue base keeps shrinking, cost base rises |

The FDA’s request to withdraw ranitidine products is the single clean inflection point separating “contested risk” from “active supply removal.” [1]

What did demand do when substitution kicked in?

Substitution was fast because Zantac sat inside an established therapeutic category with multiple replacements:

- Within class: other H2 blockers and alternative formulations.

- Across class: proton pump inhibitors (PPIs) and antacids.

Once withdrawals began, demand that would have shifted to competing H2 blockers moved further toward PPIs in many patient segments. That behavior is typical when a widely used acid-suppression product is removed and prescribers and pharmacists switch to adjacent standard-of-care options.

Commercial result: Zantac stopped behaving like an ordinary mature branded product and behaved like a discontinued product. The market stopped pricing it as a competitive brand and instead priced it as a disappearing supply stream, then as a liability.

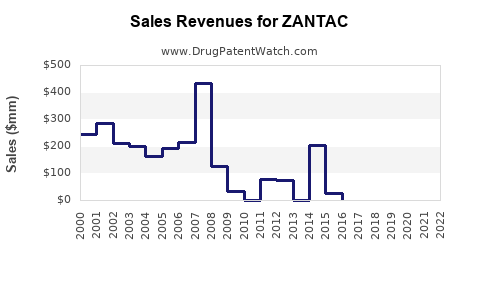

How did Zantac’s revenue profile evolve over time?

Zantac’s financial trajectory is best described as a decline from mature brand economics into a near-complete shutdown of commercial availability in the wake of NDMA actions, followed by an extended period of cost recognition through legal settlements.

While exact global revenue by year depends on corporate reporting structure and allocation of ranitidine across products, the direction of travel is consistent with the regulatory timeline: pre-2019 brand revenue advantage gave way to rapid post-2019 collapse.

A key documented indicator is that by 2020, Zantac’s manufacturer (and associated companies in the distribution chain) shifted from “operating growth mode” to “liability and settlement mode,” with substantial charges and provisions tied to ranitidine litigation and recalls. The financial profile turned from revenue deterioration to expense acceleration.

The FDA timeline provides the causal anchor for that step-change. [1]

Who carried the financial burden, and why did it persist?

The financial burden did not end with product withdrawal because:

- Inventory and chargebacks: retailers, wholesalers, and manufacturers absorbed returns, write-offs, and contracted chargebacks tied to discontinued product.

- Litigation cost accruals: plaintiffs alleged injury and contamination-related harms. The settlement process extended over multiple years.

- Regulatory and manufacturing compliance costs: firms faced escalating quality-control scrutiny and associated costs.

The persistence of costs is consistent with how mass litigation evolves: even if the product is withdrawn, claims and settlements often run for years.

What were the key commercial levers that amplified the downside?

Zantac’s market exposure amplified downside through four structural levers:

- Scale of distribution: widespread retail and wholesale penetration made the product easy to move at volume, but also made it easy to pull at volume.

- Brand mindshare at scale: Zantac had high consumer awareness, so demand did not “fade”; it flipped quickly to substitute products once safety actions landed.

- Formulation and storage considerations: NDMA levels in ranitidine were linked to conditions including time and temperature, which made “use at home” risk perception highly salient and reduced willingness to keep using the drug even if some lots tested acceptable.

- Regulatory removal logic: once regulators requested withdrawal, commercial continuity did not depend on brand performance. It depended on compliance and legal risk.

How did litigation reshape the financial trajectory?

Legal risk transformed the financial profile from primarily operating economics into a risk-and-cost regime:

- Settlement provisions and legal spend: companies recognized and managed liabilities through provisions and ongoing legal costs.

- Cash-flow pressure: settlements and judgments create cash outflows even when revenue is shrinking to near zero.

- Balance-sheet and guidance impacts: litigation often drives earnings volatility and can force conservative guidance.

This pattern is consistent with large-scale pharma product litigation after safety recalls and withdrawals.

What does the “withdrawal then settle” pattern imply for financial trajectory?

For Zantac, the business outcome follows a common post-withdrawal pathway:

- Revenue shock: product access collapses rapidly once regulators require withdrawal.

- Residual inventory unwind: remaining sales become de minimis while inventory is written down or returned.

- Cost ramp: litigation and compliance costs replace revenue as the major driver of reported financial results.

- Extended expense tail: even after sales go quiet, settlements and legal expenses carry through multiple fiscal years.

The FDA’s withdrawal request is the pivot point for the first phase. [1]

Competitive and substitution effects: what replaced Zantac economically?

Zantac’s demand moved to:

- PPIs for chronic and reflux-based indications.

- Alternative H2 blockers where available and where patients sought similar mechanisms and dosing.

- OTC symptom management for self-limited cases.

Economically, this substitution typically re-routes spend to brands and generics with different pricing structures. Zantac’s branded economics were not automatically recaptured because substitution tends to favor whatever is on formulary and available at pharmacies quickly, and because the regulatory event undermined patient and provider trust in ranitidine specifically.

Key financial trajectory summary (what mattered most)

| Phase |

Timeframe (relative) |

Primary driver |

Primary financial effect |

| Mature brand |

Pre-2019 |

Brand awareness and remaining market share |

Stable-to-declining revenue under generic pressure |

| Contamination escalation |

2019 |

NDMA evidence and regulatory actions |

Revenue shock and channel disruption |

| Withdrawal and discontinuation |

2019-2020 |

FDA request to withdraw ranitidine products |

Near cessation of sellable product |

| Litigation and settlements |

2019 onward |

Injury claims and mass settlements |

Cost accruals and earnings volatility |

The FDA request to withdraw ranitidine products from the market in 2019 defines the market discontinuation point. [1]

Key Takeaways

- Zantac’s market dynamics shifted from normal mature-brand competition to rapid, safety-driven demand collapse triggered by NDMA contamination concerns and regulatory withdrawal requests. [1]

- The financial trajectory moved from revenue decline (generic erosion plus market maturity) to a post-2019 regime where revenue shrank quickly and litigation and compliance costs dominated financial outcomes for years.

- Substitution into adjacent acid-suppression therapy helped absorb some therapeutic demand, but not in a way that restored Zantac-like branded economics.

FAQs

1) When did Zantac’s commercial decline become unavoidable?

When regulators requested withdrawal of ranitidine products from the market in 2019, eliminating normal retail and channel availability. [1]

2) Did substitution prevent a total revenue collapse?

Substitution reduced therapeutic loss at the category level, but it did not prevent Zantac-specific revenue from collapsing because the product was removed from sale. [1]

3) What was the dominant financial driver after withdrawal?

Litigation and settlement costs, along with compliance and unwind-related expenses, replaced revenue as the main driver of financial outcomes.

4) Why did the damage propagate beyond the FDA market?

Because ranitidine products were globally distributed and safety risk perception transferred quickly across jurisdictions, leading to coordinated market withdrawals and restrictions. [1]

5) What does this imply for similar legacy brands?

A mature brand can move from “routine competition” to “rapid discontinuation” when contamination or safety evidence triggers regulatory withdrawal at scale, creating revenue collapse plus a multi-year expense tail.

References

[1] U.S. Food and Drug Administration. (2019). FDA requests manufacturers and firms to stop selling ranitidine products (Zantac) and to withdraw from the market. https://www.fda.gov/