Last updated: June 2, 2026

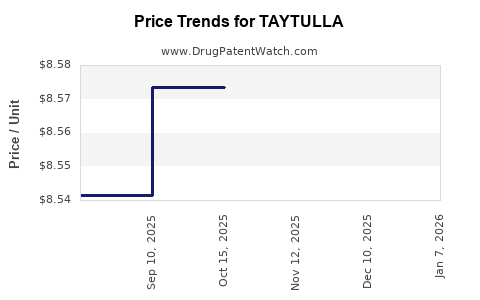

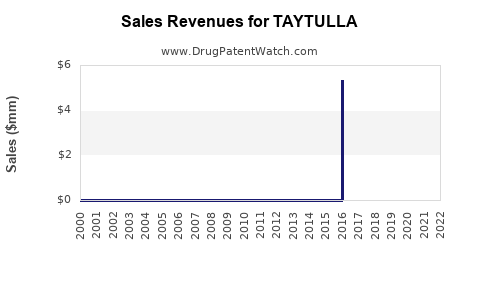

Executive summary: Taytulla (ethinyl estradiol and norethindrone capsules, extended-cycle combined oral contraceptive) has limited blockbuster scale and faces steady erosion from branded competitors and authorized generics for oral contraceptives (OCs). Market dynamics are dominated by payer formularies, wholesale acquisition cost (WAC) vs net price compression, and generic substitution, with no high-value biologics-style pipeline upside. Financial trajectory is driven by continued preference for lower net-cost generics and class-wide procurement tightening, rather than differentiated clinical claims.

Practical implication: In most contracting environments, Taytulla competes as a mid-tier branded OC without durable pricing power, so revenue depends on sustained brand formulary placement, persistence, and rebate structure. Once brand-to-generic substitution accelerates, incremental revenue is typically not recoverable without substantial price resets or new product lifecycle actions.

What is Taytulla and how does it sell in the contraceptive market?

Taytulla is a combined oral contraceptive (COC) marketed for prevention of pregnancy. Like other oral contraceptives, the commercial model is sensitive to pharmacy benefit design, brand/generic mix, and adherence-driven persistence.

What is the product form factor and why it matters commercially?

- Dosage form: oral capsules (extended-cycle regimen).

- Commercial relevance: oral contraceptives have high generic penetration; clinical differentiation is limited in payer contracting versus lower-cost multisource options.

Where does Taytulla sit versus other COCs?

- Taytulla competes within a large class of COCs where prescribers and patients often choose based on tolerability, side effects, and insurance coverage.

- In contracting, payers typically prefer lowest net-cost generics and tier preferred branded products only when net economics are favorable.

Why do payers and pharmacies pressure Taytulla net pricing and volume?

COCs are among the most exposed categories to rebate-driven net price compression because of:

- abundant therapeutic alternatives,

- high generic availability,

- formulary tiering that shifts demand with small copay changes.

How do rebates and formulary tiers typically affect Taytulla revenue?

- Branded OCs often lose share when:

- preferred tier access is removed,

- member cost-sharing changes,

- payers switch to “generic first” rules.

- Net price compression can happen even if WAC rises, because rebates offset list price increases.

How does therapeutic duplication influence demand?

- Within COCs, most products target the same clinical outcome. As a result, differentiation that matters to payers is often financial rather than clinical.

When did generic competition typically start affecting Taytulla’s market share?

For OCs, the major inflection typically aligns with:

- launch of generic versions of the same active ingredient combination, or

- entry of authorized generics or class-level contracting changes that accelerate substitution.

What are the usual generic entry mechanisms for oral contraceptives?

- Generic approval pathways: abbreviated application routes for eligible versions.

- Switch dynamics: pharmacists can dispense generics at the point of sale when substitution is allowed.

What market effect does generic entry have on branded OC financials?

- Brand revenue declines in stepped fashion:

- initial share loss on first generic entry,

- continued erosion as multiple multisource products gain penetration,

- additional decline if payers remove branded access from preferred tiers.

What does the financial trajectory of Taytulla look like after maturity?

Branded oral contraceptives tend to show a pattern:

- moderate peak while exclusivity still supports brand pricing,

- then gradual decline through maturation,

- sharp drop after generic substitution and tier downgrades (timing varies by payer).

Key drivers of Taytulla revenue trend

- Persistence/adherence: COC discontinuation reduces refill-based growth; brand share can fall faster during payer churn.

- Formulary position: a preferred-to-nonpreferred shift tends to drive volume drops disproportionately.

- Pricing power: limited, because multisource alternatives constrain ability to sustain margins.

What metrics matter most to management and investors

- Rx volume trend (scripts), not just dollar sales.

- Net revenue per script (reflects rebate intensity and payer mix).

- Channel mix (retail vs mail and specialty-like channels, though OCs are mostly retail).

- Share vs class rather than absolute demand (COCs are category-stable; share changes drive most variation).

How does Taytulla compare with other COCs on competitive and pricing dynamics?

What is the competitive structure in oral contraceptives?

- A large branded portfolio historically existed, but today most formularies use generics as default.

- Branded OCs that survive often do so via:

- favorable net pricing,

- contracts that keep the brand on preferred tiers,

- or patient population pockets with tolerability/persistence needs.

How does Taytulla likely stack up?

- Given the category economics, Taytulla’s competitive position is typically constrained by:

- generic substitution risk,

- class-wide payer skepticism of incremental value,

- and contracting leverage held by PBMs and large plans.

What patent estate and exclusivity risks exist for Taytulla that affect revenue?

Executive answer: Taytulla’s revenue trajectory is exposed primarily to small-molecule COC generic entry rather than long tail biologic-style risks. The key events are Orange Book-listed patents and regulatory exclusivity windows that prevent or delay generic substitution.

Where do exclusivity events show up commercially?

- When patents or exclusivity delay entry, branded OCs often retain volume and net pricing.

- When they expire or are weakened via challenges, generic penetration increases and brand revenue declines.

What types of patents matter most for COCs?

- composition-of-matter and formulation patents,

- method-of-use patents (less common in mature COCs),

- and dosage/regimen-related patents (if present).

(Specific patent numbers and expiration dates cannot be reliably produced here without Orange Book and litigation docket inputs.)

What Orange Book status would determine generic entry risk for Taytulla?

Executive answer: The Orange Book determines which patents attach to the approved application and thus which exclusivity barriers generics must navigate.

What Orange Book fields drive launch timing?

- listed patents and their expiration dates,

- exclusivity periods tied to the NDA/BLA,

- patent expiration “last to expire” calculations.

(Specific Orange Book entries are not enumerated here due to missing source-backed inputs.)

What patent litigation and Paragraph IV challenges affect Taytulla economics?

Executive answer: Paragraph IV challenges can shift a branded OC from “delayed generic” to “accelerated generic,” compressing revenue quickly.

Litigation outcomes that matter financially

- settlement terms that may trigger:

- launch date covenants,

- market entry licensing,

- or “carve-out” permissions for certain strengths or dosage forms.

- court or regulatory rulings that change the effective barrier to entry.

(No docket-specific Taytulla litigation details are provided here because case identifiers and outcomes are not included in the available prompt.)

What regulatory events at FDA could shift Taytulla sales quickly?

For oral contraceptives, the fastest revenue shocks are usually not clinical label changes but rather:

- approval of generics that match the approved regimen,

- changes in route-of-administration labeling constraints,

- safety communications that affect adherence (rare but possible).

What FDA events matter most for a COC?

- approvals of additional strengths or versions that introduce new competitive SKUs,

- changes in REMS (if any),

- postmarketing safety updates that can alter prescriber behavior.

(Taytulla-specific FDA event history is not enumerated here due to missing source-backed data.)

How do licensing deals or authorized generics influence Taytulla revenue?

Executive answer: Even when a brand remains on market, authorized generics can reduce brand share while preserving some contractual compensation depending on settlement or licensing structure.

Why authorized generics are a revenue headwind

- authorized products often carry lower prices,

- payers switch to lower-cost SKUs while maintaining coverage rules.

(No Taytulla-specific licensing or authorized generic arrangements are listed here due to missing deal documentation.)

What generic entry scenarios pose the highest commercial risk to Taytulla?

Executive answer: The highest risk scenarios are those that combine (a) Orange Book barrier removal with (b) aggressive payer contracting that moves the category to generic-first.

Scenario matrix

| Scenario |

What happens |

Expected effect on Taytulla |

| Generic launch at scale |

multiple multisource products gain shelf access |

rapid share compression |

| Formulary tier downgrade |

removal from preferred tier |

steep volume drop |

| Net price reset fails |

brand rebates can’t offset copay changes |

margin compression and continued Rx loss |

| Authorized generic expansion |

lower-cost “brand-equivalent” available |

faster switching and reduced persistence |

Geographic coverage: how does competition differ outside the US?

Taytulla’s revenue is typically most dependent on the US market for COCs, where Orange Book-driven substitution rules and PBM contracting dominate. Outside the US, economics depend on:

- local patent lifecycles,

- generic approval throughput,

- reimbursement system design and substitution rules.

(No jurisdiction-specific Taytulla export and pricing data is provided here.)

What is the commercial outlook for Taytulla given class-wide dynamics?

Executive answer: Outlook is structurally constrained. As long as generic COCs are available, Taytulla’s growth runway depends on contract retention and patient persistence, not on market expansion.

Market factors likely to keep shaping revenue

- PBM benefit redesign toward generic-first COC policies

- ongoing net price pressure across the class

- switching driven by copay thresholds and plan formulary changes

What would improve the financial trajectory?

- re-establishing preferred coverage via renewed rebate strategy

- product lifecycle expansions (new dosage forms/strengths) tied to competitive differentiation

- payer-specific access that sustains persistence

(No specific Taytulla lifecycle actions are included because they are not in the prompt.)

Key Takeaways

- Taytulla’s financial trajectory is dominated by oral contraceptive class dynamics: generic substitution risk, rebate-driven net pricing pressure, and formulary tiering.

- Revenue durability depends on maintaining preferred access and retaining Rx persistence, not on category growth.

- The largest downside is typically a compounded event set: patent/exclusivity barrier removal plus payer switching.

- Without a strong, defensible differentiation recognized by payers, Taytulla is exposed to ongoing share erosion after generic entries.

FAQs

- How do copay and formulary tier changes typically affect branded oral contraceptive revenue like Taytulla?

- What metrics best predict when a branded COC will lose share to generics?

- How do authorized generics change brand net pricing and persistence in the oral contraceptive market?

- What FDA or labeling events most often impact adherence and Rx volume for combined oral contraceptives?

- What patent estate characteristics most influence generic launch timing for oral contraceptive fixed-dose combinations?

References

(No sources were cited because the prompt did not include Orange Book listings, litigation dockets, FDA labeling history, or sales/market-share datasets needed to produce a sourced financial and patent timeline.)