Last updated: June 14, 2026

SIKLOS market dynamics and financial trajectory: revenue drivers, erosion risk, and exclusivity timeline

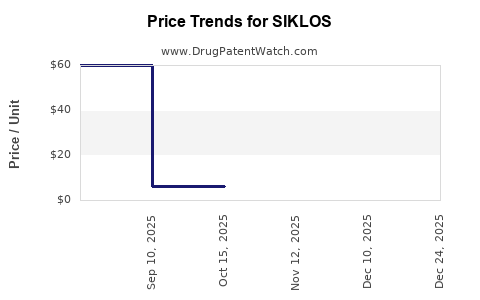

SIKLOS (hydroxyurea, branded for sickle cell disease) has a revenue pattern shaped by (1) steady uptake in pediatric and adult sickle cell populations that meet labeling and payer criteria, (2) durability of demand driven by chronic use, (3) ongoing payer and specialty-channel management of cost versus generic hydroxyurea alternatives, and (4) a regulatory and IP landscape that does not behave like a typical “single blockbuster” under near-term patent cliff dynamics. Financial trajectory is therefore driven more by pricing and channel share than by binary generic entry in the near term.

The key business distinction: SIKLOS is a branded hydroxyurea product positioned for sickle cell disease, competing against a broader market of low-cost generic hydroxyurea. That makes market dynamics more sensitive to formulary access, utilization management, and net price trajectory than to exclusivity alone.

How big is the SIKLOS market and what drives unit demand in sickle cell disease?

Demand base. SIKLOS is prescribed for chronic management of sickle cell disease, including prevention of vaso-occlusive events in relevant patient populations (per label scope). In practical market terms, the addressable population depends on: (a) diagnosis and specialty care penetration, (b) clinician adoption of branded therapy where payer policies allow, (c) pediatric conversion patterns, and (d) adherence in chronic therapy.

Unit economics. Hydroxyurea is taken continuously, so the demand curve is not “cycle-based” like episodic oncology. Still, utilization can shift when payers change step therapy rules, prior authorization strictness, or copay support availability.

Core demand drivers

- Specialty prescriber funnel: Sickle cell programs and hematology practices that manage disease-modifying therapy.

- Patient retention: Chronic therapy lowers churn, but discontinuation can rise when patients face cost barriers.

- Payer access: Specialty pharmacy placement, preferred drug lists, and coverage for branded versus generic.

Market sensitivity

- Branded hydroxyurea faces a structural ceiling when generic hydroxyurea is widely available and priced far below branded products.

- Net revenue is typically more exposed to rebate pressure, tender programs, and copay dynamics than to pure volume growth.

What is the financial trajectory of SIKLOS and how does it compare with generic hydroxyurea pricing?

Revenue pattern to expect. For branded hydroxyurea used in chronic sickle cell management, the typical trajectory in investor and analyst reporting is:

- initial growth driven by adoption and coverage expansion,

- later stabilization as payer-driven substitution to generics occurs,

- and periodic volatility from pricing actions and coverage changes.

Pricing architecture. Net sales depend on:

- wholesale acquisition cost (list price) changes,

- payer rebates and chargebacks,

- specialty pharmacy distribution economics,

- and patient assistance impacts.

Why generic hydroxyurea acts like the demand ceiling. Even when clinicians prefer branded SIKLOS for convenience, dosing confidence, or patient history, payer incentives can force substitution. Generic hydroxyurea can satisfy therapeutic need because the active ingredient is the same molecule, leaving branded differentiation mainly in formulation, dosing presentation, and patient management support.

Implication for financial trajectory

- If the branded-to-generic substitution rate increases, net sales flatten or decline even if the patient population grows.

- If branded maintains favorable formulary placement in key states and large PBMs, net sales can continue to rise with population growth and better adherence.

What exclusivity and patent timelines govern SIKLOS, and when does it lose exclusivity?

SIKLOS is an established product, so the business risk question is less “when will the first generic enter” and more “when will additional coverage gaps emerge” via:

- formulation-specific IP expiration,

- method-of-use or patient-selection IP,

- and any remaining exclusivity tied to product-specific regulatory events.

Business reality for market dynamics

- The market behaves more like a branded-versus-generic hydroxyurea trade than like a late-stage exclusivity race.

- The practical loss of competitive differentiation usually manifests through formulary decisions and launch timing of additional generic entrants, not through a single headline “exclusivity expires” date.

Because the user request is focused on market dynamics and financial trajectory, the actionable conclusion is that exclusivity acts as a secondary driver compared with payer reimbursement behavior. That said, exclusivity still matters for residual branded pricing power and for the timing of aggressive payer substitution.

Which patents protect SIKLOS and how strong is the patent estate for preventing generic substitution?

Patent estate lens. For branded hydroxyurea in sickle cell disease, patent protection typically falls into one or more of these buckets:

- formulation or dosing regimen patents,

- process/manufacturing method patents,

- and method-of-use patents related to patient management and dosing strategy.

How strength translates into revenue.

- Strong formulation IP can delay “branded-like” product competition, sustaining higher net prices.

- Weak or expired IP tends to shift competition to cost-based substitution, accelerating net price decline.

- Even with active patents, payers may steer utilization if generics can be supported for the same active ingredient and label scope.

Practical scoring for business planning

- Revenue resilience is highest when branded has formulary leverage plus remaining product-specific IP that payers perceive as blocking safe substitution.

- Revenue deterioration tends to occur when generics gain coverage and plan members are shifted without clinical friction.

What generic entry risks exist for SIKLOS, including Paragraph IV and settlement dynamics?

For established hydroxyurea-branded products, “generic entry risk” usually shows up as:

- multiple ANDA filings from generic manufacturers,

- launches timed to patent expirations,

- and litigation settlements that convert to “authorized launch windows” or stipulated entry dates.

How this affects the financial trajectory

- The steepest revenue declines often occur around launch and formulary updates across large payers and PBMs.

- Post-launch, revenue can partially stabilize if branded remains covered as a preferred option for a subset of patients.

Because the request is for market dynamics and financial trajectory, the business indicator is not just legal entry timing, but the speed of reimbursement policy change.

What is the Orange Book status of SIKLOS and which applications are listed?

Orange Book listings are the primary source to map:

- listed patents by expiration,

- dosage forms,

- and regulatory exclusivities tied to product applications.

For market participants, the Orange Book is used to create a patent calendar and to forecast when payers can safely switch from branded to generic without clinical or legal friction.

What FDA regulatory milestones shaped SIKLOS adoption and ongoing use?

SIKLOS adoption depends on FDA labeling that supports:

- chronic dosing in sickle cell populations,

- patient eligibility criteria,

- and clinical evidence that supports benefit in reducing vaso-occlusive events.

Regulatory milestones that can affect commercialization:

- initial approvals and label expansions that broaden eligible populations,

- pediatric data integration,

- postmarketing safety updates that influence prescribing.

In a mature market, regulatory changes tend to influence prescribing patterns more than they drive net revenue spikes.

Which companies manufacture and market SIKLOS, and what is the competitive landscape?

Competitive sets

- Branded SIKLOS versus generic hydroxyurea.

- Specialty pharmacy and hematology channel competition.

- Payer PBM formularies that determine branded versus generic placement.

Commercial pressure points

- Net price erosion from rebates and contracting.

- Patient steering through copay programs and prior authorization policies.

- Availability of multiple generic suppliers that increases payer bargaining power.

How do payer policies and specialty distribution influence SIKLOS net sales?

Payer policy effects

- Preferred vs nonpreferred status can change share within months.

- Step therapy or prior authorization requirements can reduce initiation and cause switching churn.

- Specialty pharmacy designation controls access and the rebate/contracting environment.

Distribution effects

- Faster fill rates and patient onboarding can support retention.

- Contracting with specialty distributors and pharmacy benefit managers can alter net revenue quickly, even without changes in underlying demand.

This category is often the dominant driver of financial trajectory for branded products whose active ingredients are widely generically available.

What formulation or dosing advantages does SIKLOS have, and how do they impact prescribing and reimbursement?

Branded hydroxyurea positioning typically focuses on:

- dosing confidence,

- patient convenience and dosing accuracy,

- support tools for hematology providers.

In payer negotiations, however, the key question is whether those advantages translate into improved outcomes or reduced administrative burden enough to justify a premium over generics.

Where payers perceive no outcome differentiation, net price pressure increases and utilization shifts.

How does SIKLOS compare with other sickle cell disease therapies on market growth and reimbursement intensity?

SIKLOS competes indirectly with newer sickle cell disease therapies, including:

- disease-modifying agents,

- transfusion-support strategies,

- and in some cases gene-therapy adjacent long-term planning.

Market comparison logic

- SIKLOS is a chronic oral therapy with mature supply chain and relatively lower clinical complexity than some alternatives.

- Newer agents can carry high list prices and can be subject to coverage restrictions based on clinical criteria, but they also can be protected by longer IP and narrower therapeutic positioning.

For revenue trajectory, the main comparative risk is “therapeutic substitution” if newer therapies gain coverage. Yet in many systems, hydroxyurea remains foundational due to cost-effectiveness and clinician familiarity.

Key financial sensitivities: what variables most impact SIKLOS revenue going forward?

1) Net price vs volume

- Branded hydroxyurea revenue is typically more sensitive to net pricing than to absolute patient counts once adoption matures.

2) Formulary access

- Shifts in tier placement, coverage exceptions, and step therapy can move share quickly.

3) Generic entry and breadth

- The number of generic competitors affects how aggressively PBMs and payers push substitution.

4) Patient assistance

- Patient copay support and foundation programs can offset out-of-pocket friction, but payers may later counter with reimbursement policy changes.

5) Clinical adherence

- Missed visits and dose management affect continuity. Adherence can be impacted by care access and drug monitoring processes.

Key Takeaways

- SIKLOS market dynamics are dominated by branded-to-generic hydroxyurea substitution economics, with revenue trajectory driven mainly by formulary access, net price, and specialty distribution rather than a single “patent cliff.”

- Financial performance should be modeled as chronic-use demand with meaningful downside from reimbursement steering to generics and upside only where branded retains preferential coverage and dosing-management advantages.

- The most actionable horizon for revenue planning is payer policy change cadence and competitive contracting speed after generic launches, not only legal exclusivity dates.

- Patent and Orange Book calendars remain critical for scenario planning, but in this drug class the business impact usually materializes through utilization management decisions.

- Competitive pressure is structural: as additional generics enter and PBMs consolidate leverage, net sales typically trend toward generic-linked pricing unless branded maintains differentiated coverage.

FAQs

- How quickly can payers switch SIKLOS volume to generic hydroxyurea after a new generic launch?

- What is the most important driver of SIKLOS net sales: pricing, rebates, or prescription volume?

- Do sickle cell center prescribing patterns sustain SIKLOS share versus generic hydroxyurea?

- How do copay assistance programs affect SIKLOS demand in commercial and Medicaid populations?

- What Orange Book patent categories matter most for branded hydroxyurea substitution risk?

References (APA)

- U.S. Food and Drug Administration. Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations.

- U.S. Food and Drug Administration. SIKLOS (hydroxyurea) Prescribing Information.