OLANZAPINE Drug Patent Profile

✉ Email this page to a colleague

When do Olanzapine patents expire, and when can generic versions of Olanzapine launch?

Olanzapine is a drug marketed by Am Regent, Anthea Pharma, Aspiro, Eugia Pharma, Omnivium Pharms, Qilu, Sandoz Inc, UBI, Ajanta Pharma Ltd, Apotex Inc, Aurobindo Pharma Ltd, Barr Labs Inc, Chartwell Molecular, Dr Reddys Labs Ltd, Hec Pharm, Hisun Pharm Hangzhou, Jubilant Generics, Macleods Pharms Ltd, Orbion Pharms, Pharmobedient, Strides Pharma Intl, Sun Pharm Inds, Torrent, Zydus Pharms, Alkem Labs Ltd, Cadila Pharms Ltd, Hikma, Indoco, Ivax Pharms Inc, Jiangsu Hansoh Pharm, Natco Pharma, Sunshine, Teva Pharms, Torrent Pharms Ltd, Epic Pharma Llc, and Ph Health. and is included in fifty NDAs.

The generic ingredient in OLANZAPINE is fluoxetine hydrochloride; olanzapine. There are twenty-seven drug master file entries for this compound. Three suppliers are listed for this compound. Additional details are available on the fluoxetine hydrochloride; olanzapine profile page.

AI Deep Research

Questions you can ask:

- What is the 5 year forecast for OLANZAPINE?

- What are the global sales for OLANZAPINE?

- What is Average Wholesale Price for OLANZAPINE?

Summary for OLANZAPINE

| US Patents: | 0 |

| Applicants: | 36 |

| NDAs: | 50 |

| Finished Product Suppliers / Packagers: | 44 |

| Raw Ingredient (Bulk) Api Vendors: | 121 |

| Clinical Trials: | 538 |

| Patent Applications: | 4,908 |

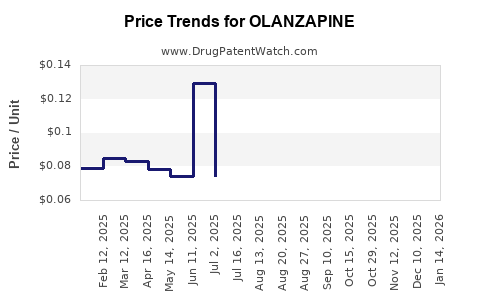

| Drug Prices: | Drug price information for OLANZAPINE |

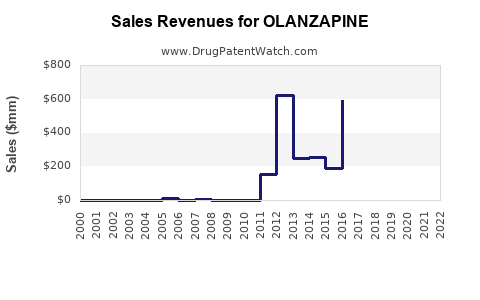

| Drug Sales Revenues: | Drug sales revenues for OLANZAPINE |

| DailyMed Link: | OLANZAPINE at DailyMed |

Recent Clinical Trials for OLANZAPINE

Identify potential brand extensions & 505(b)(2) entrants

| Sponsor | Phase |

|---|---|

| Montefiore Medical Center | PHASE4 |

| University Hospital, Strasbourg, France | PHASE2 |

| Roswell Park Cancer Institute | PHASE2 |

Pharmacology for OLANZAPINE

| Drug Class | Atypical Antipsychotic |

Anatomical Therapeutic Chemical (ATC) Classes for OLANZAPINE

US Patents and Regulatory Information for OLANZAPINE

| Applicant | Tradename | Generic Name | Dosage | NDA | Approval Date | TE | Type | RLD | RS | Patent No. | Patent Expiration | Product | Substance | Delist Req. | Exclusivity Expiration |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Zydus Pharms | OLANZAPINE | olanzapine | TABLET, ORALLY DISINTEGRATING;ORAL | 202889-004 | Mar 9, 2023 | DISCN | No | No | ⤷ Start Trial | ⤷ Start Trial | ⤷ Start Trial | ||||

| Cadila Pharms Ltd | OLANZAPINE | olanzapine | TABLET;ORAL | 210022-005 | Feb 24, 2023 | AB | RX | No | No | ⤷ Start Trial | ⤷ Start Trial | ⤷ Start Trial | |||

| Jubilant Generics | OLANZAPINE | olanzapine | TABLET, ORALLY DISINTEGRATING;ORAL | 200221-001 | Sep 12, 2012 | AB | RX | No | No | ⤷ Start Trial | ⤷ Start Trial | ⤷ Start Trial | |||

| Dr Reddys Labs Ltd | OLANZAPINE | olanzapine | TABLET, ORALLY DISINTEGRATING;ORAL | 076534-004 | Oct 24, 2011 | AB | RX | No | No | ⤷ Start Trial | ⤷ Start Trial | ⤷ Start Trial | |||

| Sunshine | OLANZAPINE | olanzapine | TABLET;ORAL | 206238-002 | Nov 19, 2018 | AB | RX | No | No | ⤷ Start Trial | ⤷ Start Trial | ⤷ Start Trial | |||

| Qilu | OLANZAPINE | olanzapine | TABLET;ORAL | 204319-004 | Jan 27, 2016 | AB | RX | No | No | ⤷ Start Trial | ⤷ Start Trial | ⤷ Start Trial | |||

| >Applicant | >Tradename | >Generic Name | >Dosage | >NDA | >Approval Date | >TE | >Type | >RLD | >RS | >Patent No. | >Patent Expiration | >Product | >Substance | >Delist Req. | >Exclusivity Expiration |

EU/EMA Drug Approvals for OLANZAPINE

| Company | Drugname | Inn | Product Number / Indication | Status | Generic | Biosimilar | Orphan | Marketing Authorisation | Marketing Refusal |

|---|---|---|---|---|---|---|---|---|---|

| Eli Lilly Nederland B.V. | Zyprexa Velotab | olanzapine | EMEA/H/C/000287AdultsOlanzapine is indicated for the treatment of schizophrenia.Olanzapine is effective in maintaining the clinical improvement during continuation therapy in patients who have shown an initial treatment response.Olanzapine is indicated for the treatment of moderate to severe manic episode.In patients whose manic episode has responded to olanzapine treatment, olanzapine is indicated for the prevention of recurrence in patients with bipolar disorder. | Authorised | no | no | no | 2000-02-03 | |

| Eli Lilly Nederland B.V. | Zypadhera | olanzapine | EMEA/H/C/000890Maintenance treatment of adult patients with schizophrenia sufficiently stabilised during acute treatment with oral olanzapine. | Authorised | no | no | no | 2008-11-19 | |

| Eli Lilly Nederland B.V. | Zyprexa | olanzapine | EMEA/H/C/000115Coated tabletsAdultsOlanzapine is indicated for the treatment of schizophrenia.Olanzapine is effective in maintaining the clinical improvement during continuation therapy in patients who have shown an initial treatment response.Olanzapine is indicated for the treatment of moderate to severe manic episode.In patients whose manic episode has responded to olanzapine treatment, olanzapine is indicated for the prevention of recurrence in patients with bipolar disorder.InjectionAdultsZyprexa powder for solution for injection is indicated for the rapid control of agitation and disturbed behaviours in patients with schizophrenia or manic episode, when oral therapy is not appropriate. Treatment with Zyprexa powder for solution for injection should be discontinued and the use of oral olanzapine should be initiated as soon as clinically appropriate. | Authorised | no | no | no | 1996-09-27 | |

| Krka | Zalasta | olanzapine | EMEA/H/C/000792Olanzapine is indicated for the treatment of schizophrenia.Olanzapine is effective in maintaining the clinical improvement during continuation therapy in patients who have shown an initial treatment response.Olanzapine is indicated for the treatment of moderate to severe manic episode.In patients whose manic episode has responded to olanzapine treatment, olanzapine is indicated for the prevention of recurrence in patients with bipolar disorder. | Authorised | yes | no | no | 2007-09-27 | |

| Mylan Pharmaceuticals Limited | Olanzapine Mylan | olanzapine | EMEA/H/C/000961AdultsOlanzapine is indicated for the treatment of schizophrenia.Olanzapine is effective in maintaining the clinical improvement during continuation therapy in patients who have shown an initial treatment response.Olanzapine is indicated for the treatment of moderate to severe manic episode.In patients whose manic episode has responded to olanzapine treatment, olanzapine is indicated for the prevention of recurrence in patients with bipolar disorder. | Authorised | yes | no | no | 2008-10-06 | |

| Teva B.V. | Olanzapine Teva | olanzapine | EMEA/H/C/000810AdultsOlanzapine is indicated for the treatment of schizophrenia.Olanzapine is effective in maintaining the clinical improvement during continuation therapy in patients who have shown an initial treatment response.Olanzapine is indicated for the treatment of moderate to severe manic episode.In patients whose manic episode has responded to olanzapine treatment, olanzapine is indicated for the prevention of recurrence in patients with bipolar disorder. | Authorised | yes | no | no | 2007-12-12 | |

| >Company | >Drugname | >Inn | >Product Number / Indication | >Status | >Generic | >Biosimilar | >Orphan | >Marketing Authorisation | >Marketing Refusal |