Last updated: April 24, 2026

Nitrofurantoin is an established urinary-tract antibiotic with stable demand driven by recurrent uncomplicated cystitis, broad prescriber familiarity, and low-to-moderate pricing. The market’s near-term dynamics are constrained by safety-driven prescribing limits (pulmonary and hepatic risks, renal function thresholds) and periodic supply and formulation shifts in key geographies. Financial trajectory is shaped less by patent exclusivity (the core active is long out of patent in most markets) and more by payer coverage, formulation mix (macrocrystals vs. macrocrystals/monohydrate combinations and branded vs. generic), and guideline adherence.

What is the current market structure for nitrofurantoin?

Nitrofurantoin’s market is predominantly generic in most major jurisdictions. Brand presence remains in certain regions and for specific formulations, but competitive pricing is dominated by multiple ANDA- and locally authorized generic products. Demand tends to be resilient because the product class is guideline-relevant for uncomplicated cystitis and is used in first-line or second-line settings depending on local resistance patterns and antimicrobial stewardship rules.

Market segmentation by use case

Common consumption drivers include:

- Uncomplicated acute cystitis in women (short course oral therapy).

- Recurrent uncomplicated cystitis prophylaxis in selected patients (longer-term regimens under monitoring).

- Institutional UTI pathways (step-down or alternative therapy when preferred agents are restricted).

Market segmentation by formulation

The practical market distinction is formulation and dosing schedule rather than drug substance alone:

- Macrocrystals/monohydrate combinations for common regimens.

- Macrocrystals alone.

- Other nitrofurantoin salts depending on region.

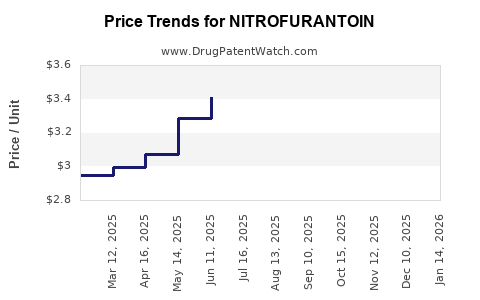

Formulation mix impacts pricing and revenue volatility because payer formularies often lock to specific presentations, and substitution can require prescriber acceptance.

Which forces drive demand for nitrofurantoin?

1) Guideline adherence and prescribing pathways

Nitrofurantoin remains a commonly recommended option for uncomplicated cystitis in many guideline ecosystems due to its narrow urinary spectrum and low systemic selective pressure compared with broader agents. That guideline fit supports steady prescription volumes even as resistance patterns shift.

2) Safety monitoring requirements and renal function thresholds

Nitrofurantoin prescribing is constrained by label- and guideline-aligned renal function criteria and risk monitoring (lung, liver, neuropathy). These constraints typically do not eliminate demand, but they can shift share away from older patients or populations with borderline kidney function.

Key commercial implication: demand is stable but not linear. After safety communications, health systems often tighten criteria, reducing utilization intensity until practice normalizes.

3) Antimicrobial stewardship and payer restrictions

Stewardship programs can either support nitrofurantoin (as a narrow option) or restrict it (if local pathways prefer alternatives). Payer utilization management also affects how readily claims move through outpatient formularies.

4) Resistance patterns and competitive class dynamics

Nitrofurantoin resistance has historically remained relatively limited compared with some alternatives, supporting its continued role. If local resistance rises or if preferred alternatives gain formulary share, nitrofurantoin volume can soften.

What constraints affect nitrofurantoin supply and continuity of treatment?

Manufacturing concentration and API sourcing risk

Like many older small-molecule antibiotics, nitrofurantoin’s supply can face periodic manufacturing disruptions or quality events. The market response typically appears quickly in pricing and availability, then normalizes when supply returns.

Commercial implication: revenue can swing around supply interruptions, with disproportionate impact on smaller formulary SKUs.

Formulation and label lifecycle effects

Switches between formulations (for example, macrocrystal schedules versus combination products) can affect:

- net price via payer preference

- adherence via dosing convenience

- substitution rates for generic equivalents

How does the financial trajectory typically look for nitrofurantoin?

Revenue mechanics in a generic-dominated market

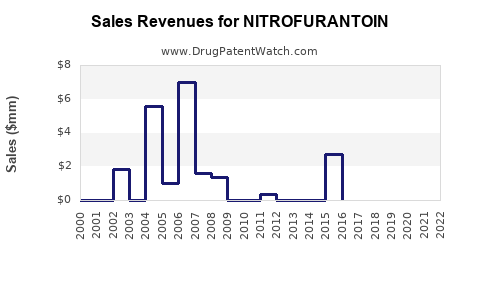

For an off-patent antibiotic, financial performance is primarily determined by:

- Unit volume (prescriptions and duration)

- Net price after rebates and payer terms

- Product mix (formulation and strength)

- Claim stability (availability and coverage)

- Competition intensity (number of stocked generics)

With broad generic competition, price declines generally drive long-run revenue flattening unless volume grows. Volume is usually steadier than price because nitrofurantoin remains clinically entrenched for uncomplicated cystitis.

What investors usually infer from nitrofurantoin economics

- Upside is usually incremental, tied to guideline reinforcement, increased recognition for recurrent cystitis prophylaxis, or expanded formulary coverage.

- Downside typically comes from utilization tightening (renal safety criteria, stewardship changes) or supply events.

- Margins can improve when consolidation reduces effective competition or when payers standardize to a limited set of presentations.

Which market signals matter most for 12 to 24-month outlook?

Coverage and guideline updates in major markets

Short-cycle policy shifts can reallocate share across urinary-tract agents. The most important market signal is whether nitrofurantoin remains a preferred agent in local acute cystitis pathways and whether it retains positioning for recurrent cystitis prophylaxis.

Safety communications and clinical practice response

Clinician practice changes after safety updates can persist for months or longer. Even when the label does not ban use, conservative thresholds reduce eligible patient pools and can dampen prescribing.

Supply chain and quality events

Availability shocks show up in:

- wholesale pricing spikes

- temporary substitution delays

- claim denials or pharmacy stockouts

These events can temporarily lift net prices while also suppressing realized prescriptions when supply is constrained.

How do regulatory and labeling realities shape commercial performance?

Nitrofurantoin’s commercial trajectory is anchored by mature regulatory history and long-standing safety labeling. Key regulatory reality is that eligibility depends on kidney function and risk profile. That translates into:

- lower utilization intensity among older patients

- greater monitoring burden

- slower uptake in settings with strict adherence protocols

These factors do not usually collapse demand, but they do cap maximum utilization and reduce growth optionality compared with on-patent products.

What is the core competitive landscape?

Generic competition as the dominant force

The competitive field is:

- multi-source generics

- regionally branded generics for certain formulations

- periodic entry of additional generic manufacturers into stocked presentations

Competitive set in uncomplicated cystitis

Nitrofurantoin’s competitive alternatives vary by geography and include other urinary antibiotics and broader agents depending on resistance and stewardship. The presence of these alternatives influences nitrofurantoin share more through pathway design and payer preferences than through differentiation in clinical outcomes.

Commercial implication: nitrofurantoin is usually not priced as a premium product. Share gains generally require payer alignment and consistent availability rather than clinical superiority.

What does historical stability imply for financial trajectory?

Nitrofurantoin behaves like a mature, commoditized antibiotic with:

- stable baseline utilization for uncomplicated cystitis

- moderate variability from guideline and safety practice enforcement

- limited upside from new-to-market innovation because the core active ingredient is established and generics dominate

The financial trajectory typically follows a mature commodity pattern:

- price erosion over long horizons

- volume stability driven by persistent clinical need

- episodic swings driven by availability and payer contract renegotiations

Key Takeaways

- Nitrofurantoin’s market is generic-dominated, so financial trajectory is primarily driven by unit volume, formulation mix, payer coverage, and net pricing rather than exclusivity.

- Demand is structurally supported by guideline relevance for uncomplicated cystitis, with additional steady demand from recurrent cystitis prophylaxis where monitored and prescribed.

- Safety constraints and renal function thresholds cap utilization intensity, especially in older and comorbid populations, which limits upside.

- Revenue volatility is most likely to come from supply continuity and formulation/payer standardization shifts rather than from step-change differentiation.

- Over 12 to 24 months, watch payer pathway decisions, safety practice enforcement, and supply chain stability as the principal determinants of realized net revenue.

FAQs

1) Is nitrofurantoin growth driven by new patentable differentiation?

No. The financial trajectory is determined mainly by generic competition, payer contracting, and utilization patterns tied to clinical guidelines and safety labeling.

2) What most strongly limits nitrofurantoin use in practice?

Renal function eligibility and risk monitoring requirements related to pulmonary, hepatic, and neurologic adverse events.

3) What formulation factors matter commercially?

Macrocrystal and macrocrystal/monohydrate product selection, dosing schedule, and payer preference drive net price and substitution rates.

4) Where does the biggest variability in revenue typically come from?

Supply continuity and wholesale availability shocks, which affect filled prescriptions and temporary pricing.

5) How does antimicrobial stewardship influence nitrofurantoin?

Stewardship can reinforce nitrofurantoin if treated as a narrow first-line option, or reduce utilization if pathways shift to alternative agents or impose stricter criteria.

References (APA)

[1] FDA. (n.d.). Nitrofurantoin products: drug safety communications and labeling information (archived label sections and safety-related updates). U.S. Food and Drug Administration. https://www.fda.gov/

[2] European Medicines Agency. (n.d.). Nitrofurantoin: product information and safety-related information in EPAR/SmPC materials. European Medicines Agency. https://www.ema.europa.eu/

[3] National Institute for Health and Care Excellence. (n.d.). Urinary tract infection (lower): guideline recommendations relevant to antimicrobial selection. NICE. https://www.nice.org.uk/

[4] American Urological Association. (n.d.). Guideline recommendations for recurrent uncomplicated bladder symptoms/UTIs where relevant to antimicrobial selection. AUA. https://www.auanet.org/