Last updated: June 24, 2026

Nexium (esomeprazole) is an established branded proton pump inhibitor with a mature, generics-dominated market in the US and most major territories. Financial trajectory is driven by the aging patent/market exclusivity cycle, persistent generic price compression, channel contracting, and portfolio shift dynamics from branded base to payer-favored equivalents. The commercial profile is also shaped by remaining brand-indication niches, formulation mix (capsules, tablets, suspension/granules where applicable), and treatment guideline adherence to PPIs.

When does Nexium lose exclusivity and how long did branded protection last?

Short answer: Nexium’s US branded exclusivity and patent protection have largely ended. Market share and pricing now reflect generic competition and payer switching rather than drug-level exclusivity.

What exclusivity periods mattered most for Nexium

- Patent term protection: Early-formulated and salt/polymorph/process and use-related filings drove the branded lifecycle in the 2000s.

- Regulatory exclusivity: As a small-molecule, Nexium’s exclusivity was typically anchored to patents rather than biologics-style exclusivity.

- Practical implication: Once key Orange Book listed patents and related litigation/stay mechanisms ended, multiple generic launch opportunities followed, accelerating price erosion.

What to expect now

- Ongoing erosion: With most markets in the post-brand era, revenue is more sensitive to distribution contracts, wholesale pull-through, and payer formulary status than to new exclusivity windows.

What patents protect Nexium (esomeprazole) and how many are still relevant?

Short answer: The Nexium patent estate that mattered for market exclusivity has largely matured. Today, remaining protection (if any) is typically about narrow formulation/process claims that do not prevent generic substitution broadly.

Key patent “buckets” historically used in Nexium protection

- Active ingredient and salts: Esomeprazole base and related salt forms.

- Polymorphs and solid-state form claims.

- Manufacturing processes: Stepwise syntheses and process controls.

- Formulation claims: Enteric coating, granulation attributes, controlled release or stability windows.

- Method-of-use claims: Less common for classic PPI regimens but can exist for specific dosing/indications.

Why generic risk is low for new entrants but low margin for incumbents

- Generic manufacturers can typically design around remaining formulation/process claims.

- The economic risk is mainly pricing, not infringement.

What is the Orange Book status of Nexium and which listings drove generic entry?

Short answer: Nexium appears in the FDA Orange Book historically with multiple listed patents. Generic entry historically depended on patent expirations and Paragraph IV challenges against select listed patents.

Orange Book dynamics that matter commercially

- Patent “carve-outs”: Some generic entrants launch only on certain strengths/dosage forms if specific formulation patents remain.

- Submission timing: ANDA approvals often followed the expiration of key listed patents or occurred under settlements/consent decrees.

Practical outcomes

- Market competition shaped around available dosage forms and pharmacy substitution rules.

- Brand share becomes highly resilient only where payer contracts preserve it, not because of enforceable exclusivity.

How many Paragraph IV challenges did Nexium face and who launched generics first?

Short answer: Nexium faced generic litigation in the formative years of branded PPIs. The commercial result is a multi-generic market structure with sustained low pricing.

What “Paragraph IV era” typically means for Nexium

- Early ANDA filers used Paragraph IV certifications to accelerate generic approval.

- Settlements historically pushed launch dates to later windows, but once protection fully expired, multiple products launched.

Commercial impact pattern

- First wave: Rapid price drop and channel stocking shifts.

- Second wave: Further price compression as additional ANDA approvals scale up.

- Long tail: Payer-driven maintenance of low net prices even after brand promotions fade.

Which companies compete with Nexium and how does the competitive landscape shape pricing?

Short answer: The Nexium market is dominated by generic esomeprazole products and payer procurement strategies. Brand economics depend on net price after rebates and contract terms rather than list price.

Competitive set

- Generic esomeprazole manufacturers with ANDA products across multiple strengths.

- Other PPIs as therapeutic substitutes:

- omeprazole, lansoprazole, pantoprazole, rabeprazole, dexlansoprazole.

- OTC channel and private label in some geographies strengthens substitution pressure.

Why therapeutic substitution matters even with generic Nexium

- Payers can switch within the PPI class.

- Even if a manufacturer maintains esomeprazole share, competing PPIs can win formulary placement.

Net price reality

- Branded PPIs rely on contracting to maintain premium share.

- Generic penetration typically drives sustained downward pricing with periodic promotional spikes that do not reverse long-run erosion.

How does Nexium financial performance track against generic price compression?

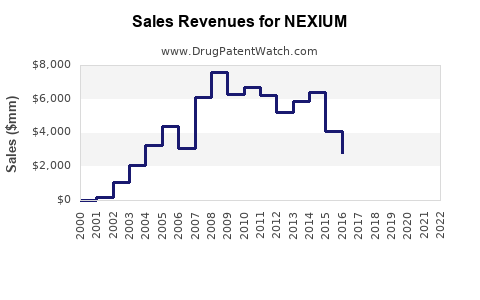

Short answer: Nexium’s brand revenue has followed a classic branded PPI trajectory: high initial peak, then prolonged revenue decline after generic entry, with stabilization only when rebates/contracts preserve formulary access.

Revenue drivers in the post-brand era

- Net revenue depends on:

- contract pricing with pharmacy benefit managers and health plans,

- ongoing promotion spend and medical necessity positioning,

- mix shift across dosing and formulations,

- patient persistence and therapeutic switching patterns.

Cost and margin dynamics

- Branded manufacturers face:

- rebate and discount pressure,

- higher share-of-voice costs to retain placement,

- potential production and compliance cost steps from formulation maintenance.

What formulations and dosage forms materially affect Nexium’s market share?

Short answer: For PPIs, differentiation is typically less about clinical superiority and more about formulary coverage by strength, dosing convenience, and administration setting.

Formulation mix

- Oral delayed-release formats historically dominate PPI utilization.

- Suspension or granule formats, where available, support pediatric and dysphagia markets.

- Enteric coating and stability specifications influence manufacturability, not clinical preference.

Why formulation patents don’t usually block generic substitution

- Generics can match pharmacokinetics and use generally permitted formulation designs.

- As a result, formulation-level patents often do not sustain broad branded economics.

What is Nexium’s biosimilar or biologics risk profile?

Answer: Nexium is not a biologic and has no biosimilar pathway risk. Competitive threats are driven by generic ANDAs and cross-class therapeutic substitution.

How do method-of-use or label-change events influence Nexium commercial trajectory?

Short answer: Label depth can influence switching dynamics, but in a mature generic-dominated class, incremental label changes have limited impact on long-run revenue once generic penetration is entrenched.

Typical commercial effect

- Specific indication expansions can support short-term growth in the branded segment.

- Over time, generic availability for those indications erodes incremental brand gains.

What patent litigation and settlements affected Nexium generic timing?

Short answer: Nexium has a history of US patent litigation in the generic transition window. The commercial takeaway is that settlements can delay certain launches, but once key patents expire, market structure stabilizes with multiple low-priced entrants.

Settlement pattern that typically plays out in PPIs

- settlements that include:

- launch date restrictions,

- payment terms,

- consent judgments tied to patent stipulations.

- Post-settlement, multiple generics can still enter through remaining patent expiries on different dosage strengths.

How does FDA regulatory status and ANDA competition shape Nexium’s market?

Short answer: FDA ANDA approvals drive the generic entry schedule and establish persistent downward pressure through pharmacy substitution.

Regulatory mechanisms

- ANDA: Generic approval for esomeprazole products based on bioequivalence.

- Patent certifications: Each ANDA submission is paired with Paragraph IV, Paragraph III, or Paragraph I/II certifications against listed Orange Book patents.

- Exclusivity and stays: Any regulatory stay tied to litigation has a time-limited effect.

Market outcome

- Approval timing translates into:

- rapid expansion of generic SKUs,

- intensified pharmacist substitution behavior,

- payer formulary pressure to use cost-effective equivalents.

Which scenarios create the biggest revenue upside or downside for Nexium now?

Short answer: Biggest upside is contract-driven retention of premium placement and niche utilization of branded products. Biggest downside is additional SKU erosion, further payer switches to non-esomeprazole PPIs, and continued generic undercutting.

Upside scenario levers

- Stronger payer contracts preserving branded esomeprazole share.

- Specialty or administration niches where brand availability or specific form factors support persistence.

- OTC to Rx transition dynamics where the brand retains credibility in the class.

Downside scenario levers

- Accelerated generic substitution in closed formularies.

- Loss of formulary access from cost re-bids.

- Cross-class substitution toward pantoprazole or dexlansoprazole based on formulary economics.

- Further erosion of net price via increased rebate pressure.

How does Nexium compare with other PPIs on patent and competitive dynamics?

Short answer: Nexium competes in a fully generic PPIs category where the dominant economic factor is net pricing and formulary placement. Relative brand strength depends on contracting and historical loyalty rather than ongoing exclusivity.

Comparison axes that matter

- Switching rates: Payer preference and pharmacy behavior.

- Price tiers: Generic parity with frequent undercutting among esomeprazole generics.

- Product breadth: Strength and dosing forms available in generic portfolios.

- Formulary strategy: Some payers prefer one PPI with preferred pricing.

Key data timeline: what the commercial arc looks like for branded Nexium

Short answer: Branded peak years followed by generic transition, then stable but low-margin branded persistence and largely generic-led utilization.

| Phase |

What happens |

Market effect |

| Branded exclusivity window |

Brand differentiation and limited direct equivalents |

High net revenue potential |

| Generic transition |

Patent expiries and litigation/settlements permit ANDA launches |

Rapid price erosion and share loss |

| Mature generic era |

Multiple ANDA SKUs and class substitution |

Stable volume, declining brand premium |

| Contract-driven stabilization |

PBM and payer contracting retains some branded access |

Modest branded revenue durability, heavy rebate dependence |

Key Takeaways

- Nexium (esomeprazole) is in a mature market where generic ANDA competition and payer switching drive financial trajectory more than remaining branded exclusivity.

- The Orange Book and Paragraph IV era shaped the timing of generic entry, but the present competitive structure is predominantly generic-led.

- Revenue and earnings exposure are tied to net pricing, rebate intensity, formulary retention, and mix across strengths/formulations, not to broad ongoing patent leverage.

- Cross-class PPI substitution is a persistent pressure point, so branded Nexium performance depends on contracting and niche persistence rather than competitive clinical differentiation.

FAQs

-

What determines whether a pharmacy substitutes Nexium with generic esomeprazole?

PBM and plan formularies, copay tiers, state substitution laws, and pharmacy contracts for generic sourcing.

-

Do Nexium patents still block generic entry in any dosage forms?

Usually only narrow formulation/process claims can delay specific SKUs; broad entry is typically unlocked once major Orange Book patents expire.

-

How do settlements in the Nexium patent litigation typically affect launch timing?

They can delay specific generic entrants to settlement launch dates while allowing later entry through remaining patent expiries and redesigned product strategies.

-

Is Nexium more exposed than other PPIs to formulary switches?

Exposure is generally class-wide, but specific risk depends on the payer’s preferred PPI economics and the availability and pricing of generic SKUs.

-

Does OTC availability change the Rx Nexium market economics?

Yes, OTC can shift patient behavior and weaken branded Rx demand elasticity, increasing substitution pressure even among Rx-focused payers.

References

- U.S. Food and Drug Administration. “Orange Book: Approved Drug Products with Therapeutic Equivalence Evaluations.” FDA.

- U.S. Food and Drug Administration. “ANDA Submissions (including Paragraph IV certifications).” FDA.