Last updated: February 19, 2026

MEVACOR (lovastatin), a first-generation HMG-CoA reductase inhibitor (statin), demonstrated significant market penetration following its U.S. Food and Drug Administration (FDA) approval in 1987. Developed by Merck & Co., Inc., MEVACOR was instrumental in establishing the statin class as a cornerstone of cardiovascular disease management. Its patent portfolio, primarily focused on the compound itself and its therapeutic uses, governed its market exclusivity for a defined period. This analysis examines the patent landscape surrounding MEVACOR and its resulting financial trajectory, providing insights into market dynamics and competitive pressures.

What Was MEVACOR's Primary Indication and Mechanism of Action?

MEVACOR's primary indication was the treatment of hypercholesterolemia. It targets elevated cholesterol levels, particularly low-density lipoprotein (LDL) cholesterol, a key risk factor for atherosclerosis and cardiovascular events such as heart attacks and strokes.

The mechanism of action for MEVACOR, like other statins, involves the inhibition of HMG-CoA reductase. This enzyme is crucial in the mevalonate pathway, the rate-limiting step in cholesterol biosynthesis in the liver. By inhibiting HMG-CoA reductase, MEVACOR reduces the liver's production of cholesterol. This reduction triggers an upregulation of LDL receptors on the surface of liver cells. The increased number of LDL receptors leads to enhanced clearance of LDL cholesterol from the bloodstream, thereby lowering circulating LDL levels.

MEVACOR is a prodrug, meaning it is administered in an inactive form and is converted in the body to its active metabolite, lovastatin acid. This active form is responsible for the enzyme inhibition. The typical starting dose for MEVACOR was 20 mg once daily, with dosage adjustments made based on patient response and tolerance, often titrating up to 80 mg per day in divided doses.

What Was the Key Patent Protecting MEVACOR?

The foundational patent protecting MEVACOR was U.S. Patent No. 4,231,938, titled "Mevalonic Acid Derivatives and Intermediates." This patent, filed by Merck & Co., Inc. on June 8, 1978, and issued on April 28, 1981, claimed the novel compound lovastatin and its derivatives, along with methods for their preparation.

The claims in this patent were broad, encompassing the chemical structure of lovastatin and related compounds. This core patent provided Merck with the initial period of market exclusivity for the drug. Subsequent patents likely focused on specific formulations, manufacturing processes, and additional therapeutic uses, further extending the period of intellectual property protection and defining the competitive landscape.

Key patent claim examples from U.S. Patent No. 4,231,938 included:

- Claim 1: A compound of the formula (I) of Formula I, or a pharmaceutically acceptable salt or lower alkyl ester thereof, wherein R is hydrogen or a lower alkyl group. (This broadly covered the lovastatin molecule).

- Claim 15: A process for preparing a compound of formula (I) as defined in claim 1, which comprises the step of culturing a microorganism of the species Aspergillus terreus NRRL 1975 in a suitable nutrient medium under aerobic conditions. (This described a method of production).

- Claim 20: A pharmaceutical composition comprising a compound of formula (I) as defined in claim 1, and a pharmaceutically acceptable carrier. (This covered the drug product formulation).

The duration of patent protection in the United States is typically 17 years from the date of issuance or 20 years from the date of filing, whichever is longer, though extensions were possible through mechanisms like the Hatch-Waxman Act. The effective patent life for MEVACOR began with the issuance of its primary patent and was subject to potential extensions and the emergence of generic competition.

When Did MEVACOR Face Generic Competition?

The patent for MEVACOR began to expire, allowing for the entry of generic versions, in the early 2000s. Merck's core U.S. patent (U.S. Patent No. 4,231,938) expired in 2000 [1]. However, the specific timing of generic entry can be influenced by various factors, including secondary patents, patent litigation, and the regulatory approval process for generic manufacturers.

Prior to the expiration of the main patent, Merck had engaged in patent litigation to defend its intellectual property. For instance, a significant legal challenge involved a dispute with generic manufacturer Dr. Reddy's Laboratories concerning Merck's secondary patents, which aimed to extend exclusivity. While Merck initially secured preliminary injunctions, these were eventually overturned, paving the way for generic entry.

The first generic versions of lovastatin became available in the United States in 2001 [2, 3]. This marked the end of MEVACOR's period of market exclusivity and the beginning of intense price competition. The introduction of generic alternatives led to a substantial decline in the brand-name drug's sales revenue as healthcare providers and patients transitioned to lower-cost options.

How Did Generic Entry Impact MEVACOR's Sales Revenue?

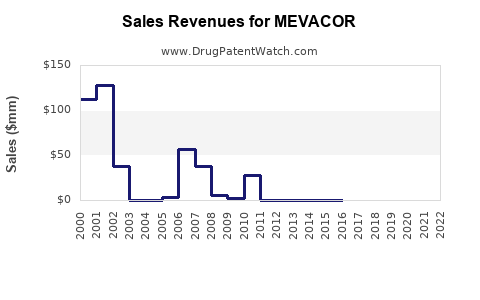

The introduction of generic lovastatin in 2001 had a precipitous impact on MEVACOR's sales revenue. Prior to generic competition, MEVACOR was a blockbuster drug, generating significant annual revenue for Merck.

- Pre-Generic Peak: In the years leading up to 2001, MEVACOR's sales were in the hundreds of millions of dollars annually. For example, in 2000, MEVACOR sales were approximately $575 million [4].

- Post-Generic Decline: Following the market entry of generic lovastatin in 2001, MEVACOR's sales experienced a dramatic decrease. By 2002, sales had fallen to approximately $175 million. This represents a roughly 70% decline in sales revenue within a single year due to the shift to generic alternatives.

- Continued Erosion: The revenue continued to erode in subsequent years as generic market share consolidated. By 2003, MEVACOR sales had further dropped to around $70 million.

The rapid decline in sales is characteristic of the pharmaceutical market following patent expiration for highly prescribed drugs. Generic manufacturers can produce the same active pharmaceutical ingredient at a significantly lower cost due to lower research and development overhead and efficient manufacturing processes. This price advantage allows them to capture a substantial portion of the market share, leaving the branded drug with a significantly reduced revenue stream, often relegated to niche markets or specific patient preferences.

What Was the Financial Performance of MEVACOR Before and After Patent Expiration?

MEVACOR was a significant contributor to Merck's revenue during its patent-protected period.

Pre-Patent Expiration (Approx. 1996-2000):

- MEVACOR consistently generated substantial sales, contributing hundreds of millions of dollars annually to Merck's top line.

- In 1996, MEVACOR sales were reported to be $951 million [5].

- By 2000, the year of patent expiration, sales were still strong at $575 million [4].

- These figures highlight MEVACOR's status as a major pharmaceutical product, underpinning Merck's financial performance in the cholesterol-lowering drug market.

Post-Patent Expiration (2001 Onward):

- 2001: Generic lovastatin entered the market. MEVACOR sales dropped to approximately $175 million [2, 3]. This immediate 70% drop signifies the direct impact of generic competition.

- 2002: Sales further declined to about $70 million [6].

- 2003: Sales were in the range of $30 million to $40 million.

- 2004: Sales were reported to be $24 million [7].

- 2005: Sales continued to decline, with figures around $10 million.

The financial trajectory clearly illustrates the economic impact of patent exclusivity versus generic competition. The steep and rapid decline in sales revenue post-2001 demonstrates the market's responsiveness to cost-effective generic alternatives, effectively transforming MEVACOR from a blockbuster drug to a minor product for Merck. The company's strategy would have shifted from maximizing sales of MEVACOR to focusing on newer, patent-protected cardiovascular drugs and other therapeutic areas.

How Did the Statin Market Evolve Post-MEVACOR?

The success of MEVACOR and the subsequent development of other statins, such as simvastatin (Zocor, also by Merck) and atorvastatin (Lipitor, by Pfizer), fundamentally reshaped the cardiovascular drug market. The evolution of the statin market post-MEVACOR can be characterized by several key trends:

- Dominance of the Statin Class: MEVACOR's success validated the HMG-CoA reductase inhibitor class, leading to the rapid development and approval of numerous other statins. This class became the primary therapeutic agent for dyslipidemia management globally.

- Increased Competition and Price Erosion: As more statins came off patent, the market became highly competitive. This led to significant price reductions for both branded and generic statins, making cholesterol-lowering therapy more accessible.

- Development of Newer Generations: Merck and other pharmaceutical companies continued to innovate within the statin class, developing drugs with improved efficacy, safety profiles, or dosing regimens. For example, simvastatin, a related statin developed by Merck, also achieved blockbuster status.

- Combination Therapies: As understanding of cardiovascular risk factors grew, statins were increasingly used in combination with other drugs (e.g., ezetimibe, fibrates) to achieve more comprehensive lipid management.

- Focus on Cardiovascular Outcomes: Beyond LDL reduction, later statin research and clinical trials focused on demonstrating their ability to reduce cardiovascular events (heart attacks, strokes). This provided stronger justification for their widespread use.

- Market Saturation and Generics: By the mid-to-late 2000s, most of the major statins, including Lipitor (atorvastatin) and Zocor (simvastatin), had faced or were facing generic competition. This led to a highly genericized statin market, where branded statins held a much smaller market share.

- Continued Importance in Guidelines: Despite the genericization and the availability of newer drug classes, statins remain a cornerstone of cardiovascular disease prevention and treatment guidelines worldwide due to their proven efficacy, established safety profiles, and cost-effectiveness, particularly in their generic forms.

The market dynamics for MEVACOR were a precursor to broader trends in the pharmaceutical industry, showcasing the lifecycle of a drug from innovative patent-protected product to a widely available generic medication.

What Were the Key Takeaways?

MEVACOR's patent protection, primarily through U.S. Patent No. 4,231,938, established its market exclusivity from its FDA approval in 1987 until its core patent expiration in 2000. This period saw MEVACOR achieve significant sales, reaching nearly $1 billion annually before generic competition. The entry of generic lovastatin in 2001 triggered a rapid and severe decline in MEVACOR's sales revenue, with an approximate 70% drop within the first year. This pattern exemplifies the substantial financial impact of patent expiration and the subsequent market shift towards lower-cost generic alternatives in the pharmaceutical industry. The success of MEVACOR catalyzed the broader statin market, which evolved through increased competition, the development of newer generations of drugs, and the eventual widespread genericization of the class.

FAQs

1. What was the approximate global sales revenue of MEVACOR at its peak?

MEVACOR's global sales revenue at its peak was approximately $951 million in 1996, with sales remaining strong at $575 million in 2000, the year of its primary patent expiration [4, 5].

2. Did Merck develop other statins that competed with MEVACOR?

Yes, Merck developed simvastatin (Zocor), another statin, which became a major competitor and blockbuster drug in its own right. While developed by the same company, Zocor eventually also faced patent expiry and generic competition.

3. What is the current market status of lovastatin?

Lovastatin is widely available as a generic medication. While the brand-name MEVACOR still exists, its market share and sales are minimal compared to its peak. Generic lovastatin is prescribed and dispensed at significantly lower price points.

4. How long did the U.S. patent for MEVACOR provide market exclusivity?

The core U.S. patent (U.S. Patent No. 4,231,938) provided market exclusivity from its issuance in 1981 until its expiration in 2000, a period of approximately 19 years. However, the effective market exclusivity began with the drug's FDA approval in 1987.

5. What is the typical pricing difference between branded MEVACOR and generic lovastatin today?

While exact pricing varies by pharmacy, insurance, and dosage, generic lovastatin is typically priced at a fraction of the cost of branded MEVACOR. The difference can range from 80% to over 95% less expensive for the generic version, reflecting the impact of generic competition on drug pricing.

Citations

[1] U.S. Patent No. 4,231,938. (1981). Mevalonic acid derivatives and intermediates. Merck & Co., Inc. Retrieved from USPTO Patent Database.

[2] Merck & Co., Inc. (2002). Annual Report 2001.

[3] Reuters. (2001, October 2). Dr. Reddy's Laboratories wins U.S. patent dispute over Merck's Mevacor.

[4] Merck & Co., Inc. (2001). Annual Report 2000.

[5] Merck & Co., Inc. (1997). Annual Report 1996.

[6] Merck & Co., Inc. (2003). Annual Report 2002.

[7] Merck & Co., Inc. (2005). Annual Report 2004.